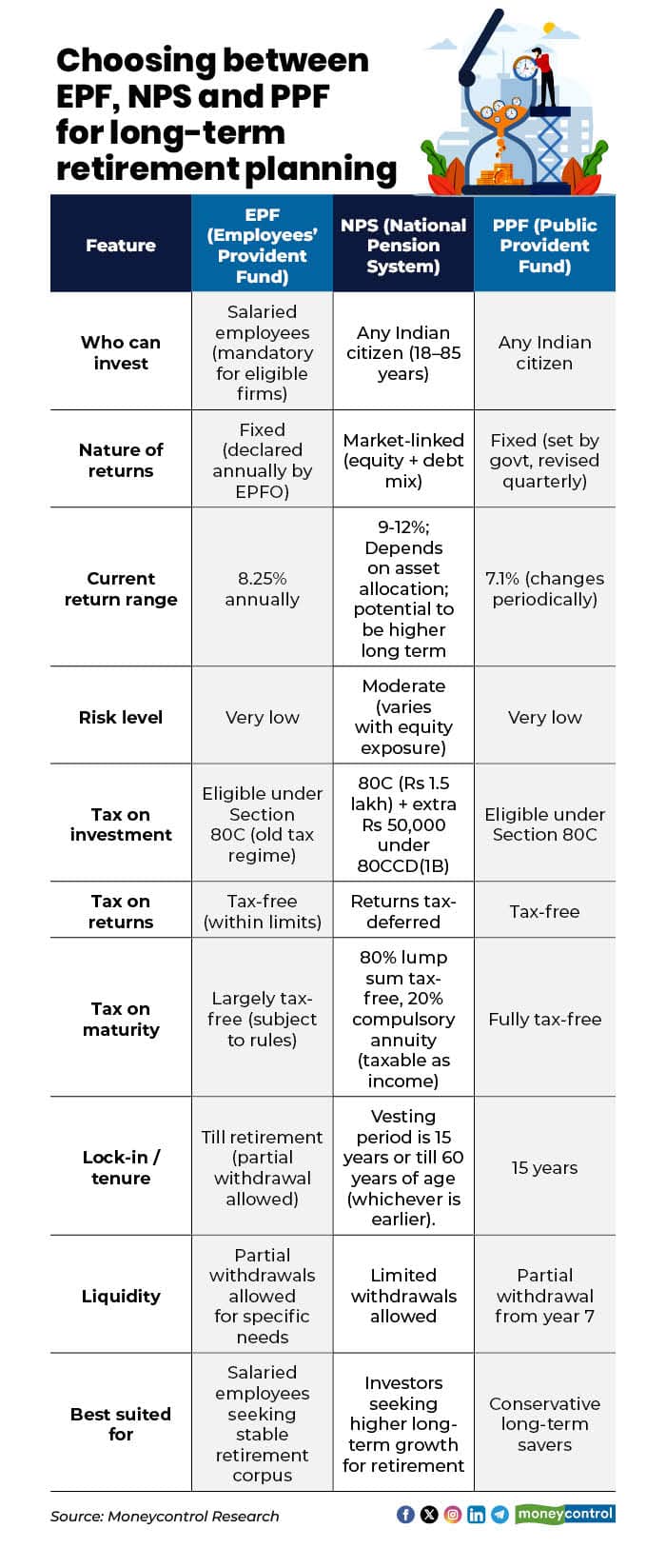

When it comes to retirement planning, investors often struggle to decide between the Employees' Provident Fund (EPF), Public Provident Fund (PPF) or National Pension System (NPS). The choice is not about picking a superior scheme but the one aligns best with your life stage, risk appetite and tax objectives. Each serves a different purpose in building a retirement corpus.

The Employees' Provident Fund builds disciplined, long-term wealth for salaried professionals through structured contributions. The Public Provident Fund (PPF) offers safety and predictability for those who value capital protection. The National Pension System (NPS), with its market-linked exposure, provides the potential for higher long-term growth for investors comfortable with moderate risk.

"Each product has its pros and cons; PPF has EEE (exempt, exempt, exempt), where contribution, interest, as well as maturity proceeds are tax exempt, a structural advantage, but with an annual limit of Rs 1.5 lakh. NPS has a dedicated tax-deduction section but liquidity and mandatory annuity are not universally liked. There is no single best-suited product; choice should be based on your circumstances, taxation, and liquidity needs," said Amol Joshi, founder, PlanRupee Investment Services.

Choice Connect CEO Atish Jain said, "EPF and PPF help build a stable and predictable base through government-backed returns and tax efficiency but relying only on fixed-return instruments over long periods can make it difficult to beat inflation."

EPF

Choose EPF if you're a salaried employee in the organised sector with EPF benefits. It allows you to build a low-risk, stable and automatic retirement corpus through monthly salary deductions. This option is ideal if you prefer a largely tax-free maturity and do not require high liquidity.

"EPF offers stability and mandatory employer contribution, which remains tax exempt within prescribed limits even under the new tax regime, though premature withdrawal is restricted," said Jignesh Shah, Partner Direct Tax at Bhuta Shah & Co LLP.

Best For

The scheme is best suited for risk-averse salaried individuals who want predictable retirement savings.

PPF

If you want safe, tax-free, long-term savings with a sovereign guarantee then PPF is one of the best options to remain invested for 15 years. Self-employed individuals can also have EPF. You get the flexibility to invest small amounts each year and create building the debt portion of your portfolio.

Best For

PPF is suitable for conservative investors and self-employed individuals, offering tax-free interest and maturity proceeds, with a 15-year lock-in period.

NPS

NPS addresses this gap by offering market-linked exposure at low cost, making it more suitable for long-term wealth creation.

It offers market-linked returns for potentially higher long-term growth.

It also offers an extra Rs 50,000 tax deduction beyond Section 80C. If retirement planning is your primary goal, and you can stay invested for 15 years or until age 60, whichever comes first, then this plan is worth a look. If you are okay with a partial annuity at retirement, NPS is the way forward.

Best for

NPS is suitable for investors seeking market-linked growth at a low cost structure with equity exposure and those with a long time horizon. "Under the new tax regime, deduction for employee contributions to EPF, PPF and NPS is not available; however, employer contribution to NPS up to 14 percent of salary continues to be deductible, a real edge, said Shah.

How to plan for retirement?

Retirement planning works best when it balances safety with growth. Start early, invest regularly and review your portfolio from time to time.

"In my view, retirement planning should be layered - a combination of stability and growth. The biggest mistake people make is delaying retirement planning, not selecting the wrong product. Start early, stay consistent, and review periodically - that matters far more," said Mahesh Shukla, Founder and CEO of PayMe.

Simple rule of thumb:

"In practice, the most effective retirement strategy is a combination approach, using EPF or PPF for stability and NPS for growth potential. We are also seeing through our partner network that investors increasingly prefer this blended allocation rather than a single product, as awareness around inflation and longer life expectancy continues to rise," said Jain.

(Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.