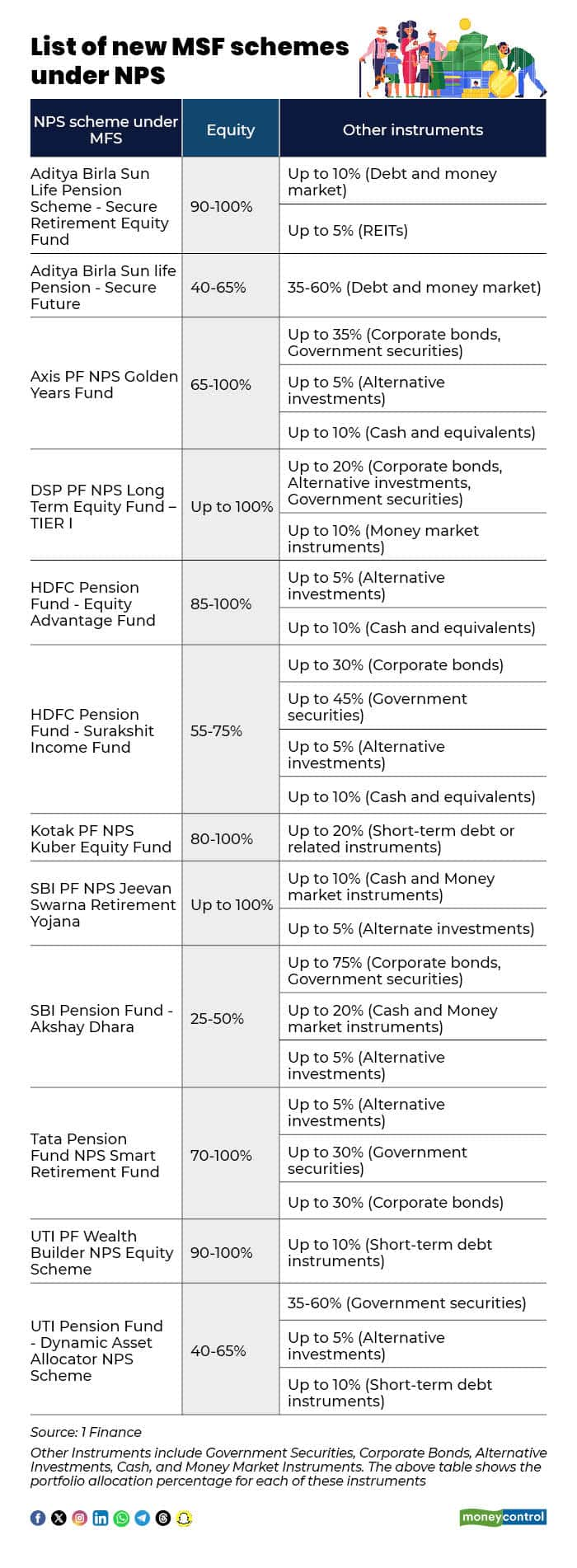

With the introduction of the Multiple Scheme Framework (MSFs) under the National Pension System (NPS), subscribers have greater flexibility in deciding how their money is invested. They can also invest up to 100 percent in equity. While this enhances return potential, it also makes tracking asset exposure more critical than ever.

Under NPS, investments are divided into three core asset classes: E (Equity), C (Corporate Debt) and G (Government Securities) -

The right mix of these three determines both growth and risk management in a retirement portfolio.

“Understanding asset exposure in NPS MSF schemes is essential for subscribers to clearly evaluate how their retirement corpus is allocated across equity (up to 100 percent), corporate debt, and government securities, all under a single PRAN. This visibility enables investors to assess risk levels, track performance through NAV and benchmark comparisons, and ensure their portfolio aligns with long-term retirement objectives,” said Siddhi Kamble, executive in Mutual Fund at 1 Finance.

Existing NPS subscriber cannot transfer their current scheme to the NPS MSF scheme. Currently, only new contributions are permitted to NPS MSF schemes. However, existing NPS subscribers can choose a new scheme launched under NPS MSF and begin investing there.

MSF offers a range of investment schemes, each with two options. One with moderate risk and another with high risk, potentially including up to 100 percent in equities.

However, allocating 100 percent of your funds to equity risks your entire NPS retirement savings to market swings, since it lacks a buffer from less volatile assets such as debt. A significant market decline before you start withdrawals results in selling more units at reduced prices, reducing your retirement income.

“Greater transparency helps in monitoring market volatility, maintaining proper diversification, identifying underperforming schemes for timely switches, and preventing unintended risks such as excessive equity exposure as retirement approaches,” said Kamble.

It is also important to note that switching between NPS MSF schemes is not allowed if your selected scheme hasn't performed well before completing 15 years.

In traditional NPS options, the Auto Choice (Lifecycle Fund) automatically adjusts allocations based on age. It keeps a higher equity stake when you are young and gradually shifts towards corporate debt and government securities as retirement nears. This predefined glide path helps lower risk over time without needing active management from the subscriber.

However, MSFs do not automatically rebalance based on age. The investor is responsible for regularly reviewing and adjusting their asset allocation based on their age and proximity to retirement. Without this discipline, a subscriber may unknowingly hold excess equity exposure into their final working years.

“While equity can generate superior long-term returns, it is inherently volatile. A market downturn close to retirement can significantly erode accumulated savings,” said Vishwajeet Goel, Head of Pensionbazaar.com.

“By consciously balancing exposure across E, C and G, especially in the years leading up to retirement, the investors can mitigate last-minute retirement shocks and protect their hard-earned corpus, ensuring a smoother and more financially secure transition into retirement,” added Goel.

Therefore, it is wiser to allocate your NPS investment towards retirement planning instead of solely choosing 100 percent equity. Experts also suggest that investing in NPS MSF at age 30-35, withdrawing between 45-50, and taking an annuity might deplete your NPS corpus before age 75. You should consider whether your annuity income can last from age 50 to 75.

In simple terms, flexibility offers empowerment, but it also requires responsibility. Consistently monitoring and adjusting asset allocation and savings until retirement is essential to facilitate a smoother and more secure financial transition into the golden years of your life.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.