The National Pension System (NPS) offers two distinct structures — the traditional common schemes and the newer Multiple Scheme Framework (MSF).

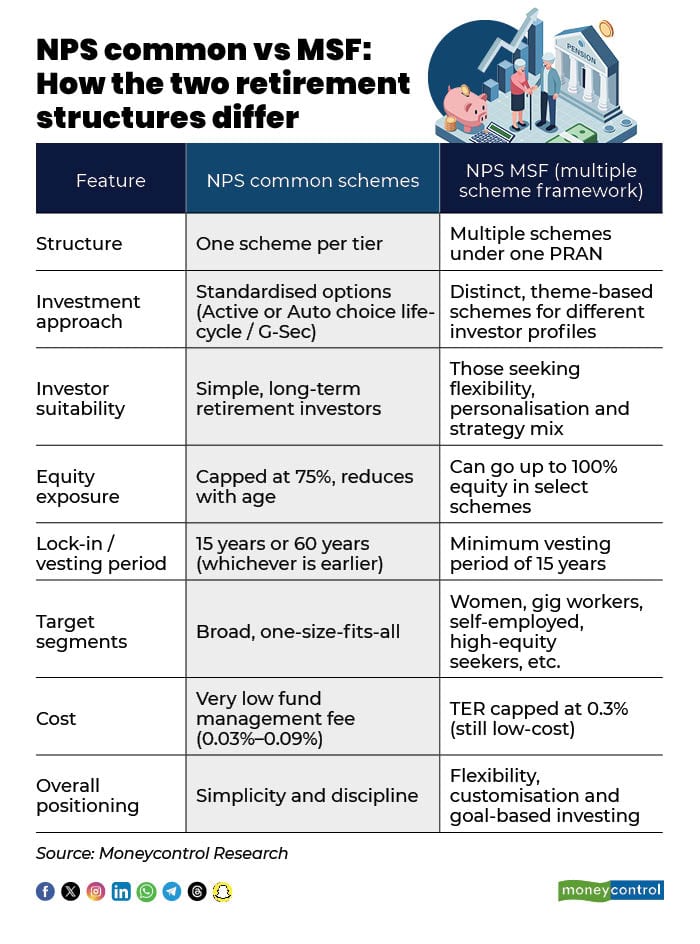

In common NPS schemes, the investment process is simple and uniform for everyone. A subscriber can select only one scheme per tier and then decide how to invest the funds. This can be done in two ways.

Under Active Choice, the investor decides the proportion of money to be put in equity, corporate bonds and government securities based on personal risk comfort. Under Auto Choice, the allocation is done through pre-set life-cycle options such as Life Cycle 25, 50 or 75, where equity exposure is higher when the investor is young and gradually reduces with age to lower risk.

There is also a balanced life-cycle fund and an option to invest entirely in government securities for maximum safety. "Because the structure is fixed and requires fewer decisions, it suits investors who want a straightforward, long-term retirement plan without frequent changes," SBI Pension Funds MD and CEO Pranay Ranjan Dwivedi said.

Under the common schemes, the cap on equity allocation is 75 percent and decreases with age to reduce exposure to equity volatility.

The MSF empowers pension funds to offer distinct schemes tailored to specific subscriber profile such as women, gig workers, platform-based earners, self-employed professionals or investors seeking 100 percent equity exposure. "Earlier, such segmentation was not possible under common schemes. MSF allows multiple schemes under one PRAN, enabling subscribers to diversify strategies, for example, combining a high-growth equity scheme with a conservative debt-focused one, based on personal goals and risk tolerance," said Dwivedi.

What is on offer?

There are around 16 schemes available under the MSF, giving subscribers a wider choice of investment styles within a single PRAN. These are offered by Aditya Birla Sun Life Pension (Secure Retirement Equity Fund and Secure Future), Axis Pension Fund (Golden Years Fund – Growth), DSP Pension Fund (Long Term Equity Fund), HDFC Pension Fund (Equity Advantage Fund and Surakshit Income Fund), ICICI Prudential Pension Fund (My Family My Future and NPS Dream), Kotak Pension Fund (Kuber Equity Fund), LIC Pension Fund (Growth Plus and Smart Balance), SBI Pension Fund (Akshay Dhara and Jeevan Swarna), Tata Pension Management (Smart Retirement Fund) and UTI Pension Fund (Dynamic Asset Allocator NPS Scheme and Wealth Builder NPS Equity Scheme)

A key advantage of MSF is its minimum vesting period of 15 years, compared with a lock-in period until age 60 in other schemes, such as corporate NPS. This offers welcome flexibility, particularly to younger subscribers or those unsure about committing for three decades.

Rajani Tandale, senior vice president, Mutual Fund at 1 Finance, said, "Under the MSF, exit timing becomes more flexible. For instance, a 35-year-old investing in an MSF option can choose to exit after 15 years. In such a case, at age 50, he can withdraw up to 80 percent of the accumulated corpus as a lump sum and using the remaining 20 percent to purchase an annuity. The withdrawal rules, however, remain the same."

There is a cost difference. However, options remain significantly cheaper than most other market-linked products. MSF typically comes with a slightly higher expense ratio than standard NPS schemes due to additional fund management and operational complexity.

Pensionbazaar.com head Vishwajeet Goel said, “Importantly, the total expense ratio is capped at just 0.30 percent of AUM, reinforcing NPS’s position as one of the most cost-efficient retirement products globally."

"In addition, a performance-linked incentive of up to 0.10 percent for schemes that attract a high proportion of new subscribers encourages innovation and healthy competition among pension fund managers, while maintaining a disciplined and investor-friendly cost structure.”

However, it’s also important to note that common schemes charge as little as 0.03 percent to 0.09 percent in fund management fees.

The MSF under the NPS marks a meaningful step forward in retirement investing. By allowing subscribers to hold multiple schemes under a single PRAN and offering tailored investment options, including high-risk variants with up to 100 percent equity allocation, the framework enhances flexibility and aligns portfolios with individual risk appetites and long-term goals.

In essence, both structures are designed to help investors build retirement wealth over time. "Common schemes suit those who value simplicity. MSF caters to those seeking flexibility, personalisation, or shorter commitment horizons," said Dwivedi. The Pension Fund Regulatory and Development Authority (PFRDA) offers both so that investors can choose what aligns with their financial journey .

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.