Indian stock markets have seen a sharp pullback from record highs. Both the Nifty 50 and Sensex have fallen over 4 percent in a week, unsettling many retail investors.

The Nifty 50 is down over 4 percent from its peak of 26,373.2, which it had hit on January 5, while the Sensex has fallen 4 percent from its high of 86,159.02 on December 1 last year. On January 20, the Nifty closed at 25,232, and the Sensex at 82,180, reflecting another day of losses in the market.

As markets turn volatile, a familiar question resurfaces: should you continue your SIPs or pause them until things settle down?

Financial advisors warn that this is exactly when most investors make costly mistakes when they stop SIPs, just as long-term wealth creation is about to take shape. Here’s why staying invested matters, and how to navigate SIPs during market corrections.

Let’s explore the pitfalls, strategies, and mindset needed for SIP success.

Common reasons investors stop SIPs early

Market volatility tops the list, as short-term losses trigger fear and panic-selling during corrections, ignoring these are the very times when SIPs accumulate more units at lower prices.

Other factors include comparing returns to trending assets or high-performing funds, cash-flow issues from job changes or expenses, and a lack of initial conviction about market cycles.

Lt Col Rochak Bakshi (retired), founder of True North Finance, a financial and investment planning firm said, “Recency bias, where investors chase recent highs, and loss aversion further exacerbate this, treating SIPs like short-term trades rather than disciplined investments. As a result, many exit just before the wealth-building phase begins.”

The High Cost of Quitting: Eroding gains through missed compounding

Quitting early deprives investors of rupee-cost averaging in downturns and the compounding effect, which ramps up after 7-10 years. “SIPs thrive on time, not timing; early exits turn them into mediocre savings tools, locking in losses and forfeiting future growth,” said Vijay Maheshwari, founder of Stocktick Capital.

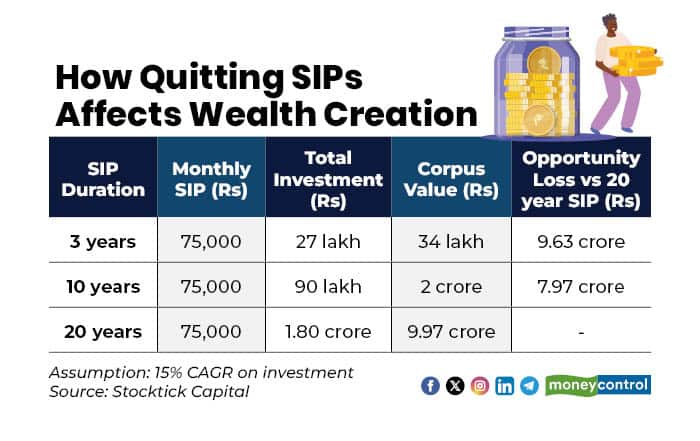

Consider a Rs 75,000 monthly SIP at 15 percent CAGR: After 3 years, the total investment of Rs 27 lakhs yields Rs 34 lakhs, but continuing to 20 years builds Rs 9.97 crore on Rs 1.8 crore invested. Stopping at 3 years means an opportunity loss of Rs 9.63 crore; even stopping at 10 years (Rs 2 crore corpus), it's Rs 7.97 crore forgone.

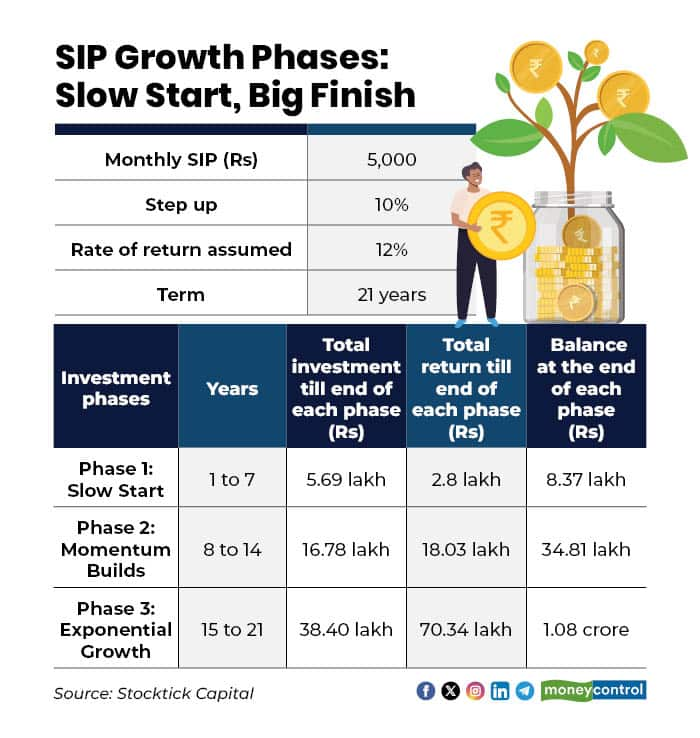

“Wealth creation is back-loaded—the first 7 years build a base, years 8-14 gain momentum, and the final phase explodes due to compounding on a larger sum. No timing or luck is needed; consistency alone drives this,” said Maheshwari.

For instance, a Rs 5,000 monthly SIP with 10 percent annual step-up and 12 percent returns grows to Rs 1.08 crore in 21 years. The investment phases show slow growth initially (Rs 8.37 lakh in 7 years), building momentum (Rs 34.81 lakh in 14 years), and exponential growth in the final phase (Rs 1.08 crore in 21 years).

Boosting outcomes with step-up SIPs

A step-up SIP increases contributions annually. For instance, for a Rs 5,000 starting SIP over 15 years at 12 percent returns, a conventional plan invests Rs 9 lakh for Rs 24 lakh maturity, while a 10 percent step-up invests Rs 15.3 lakh for Rs 36 lakh, a 50 percent boost.

Ideal for salaried professionals or young earners, it suits late starters (e.g., age 45 with Rs 10,000 starting and 15 percent annual increase, yielding Rs 90 lakhs in 15 years) or those with small initial amounts.

“However, it's unsuitable for self-employed individuals with inconsistent cash flows. Start in mid-30s when finances stabilize for maximum impact,” said Bakshi.

Also read | How NPS contributions cut your income tax under both old and new regimes

Psychological barriers and advisor strategies

Impatience for quick gains, especially in sideways markets, leads to exit within five years, as early modest returns erode confidence.

SIP is a long-term concept and starts showing results only after 7 to 10 years. Most investors don't have the patience to stick to the process. “Frequent comparison with peers, market indices, or recently outperforming funds further weakens conviction and encourages premature exits,” said Maheshwari.

“Successful SIP investing needs the investor to appreciate delayed gratification, which is a rare quality,” said Bakshi.

Advisors counter this by setting realistic expectations, explaining back-loaded returns, and communicating during dips to reframe them as opportunities.

Goal-based planning ties investments to milestones like education or retirement, reducing short-term focus. “Automated step-ups, periodic reviews, and a behavioral guidance-based approach with hand-holding build discipline and prevent errors,” said Maheshwari.

Elements for turning SIPs into extraordinary wealth

Beyond consistency, start early for exponential compounding, where later years generate most wealth. Gradually step up contributions, maintain asset allocation through rebalancing, and select quality funds with strong philosophies and risk management.

“Uphold behavioral discipline by ignoring market noise, ensure cost and tax efficiency, and review portfolios regularly to align with goals,” said Maheshwari. These amplify outcomes without chasing high-risk returns.

Also read | Here is how to invest smartly if you earn Rs 1 lakh a month

Building patience in volatile markets

For beginners, advisors recommend linking SIPs to goals (like buying a house) rather than focusing on returns, to handle market ups and downs. Automate investments, limit reviews to annually, and view volatility as a chance to buy low. Gradually increase amounts via step-ups, stay informed via credible sources without obsession, and remember compounding rewards endurance, not speed.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.