Earning Rs 1 lakh a month should, in theory, make saving and investing easier but in reality, that doesn’t always happen. Rent, EMIs and everyday expenses have a way of eating into income, leaving far less to save than expected.

More often than not, the issue isn’t the salary. It’s the lack of a clear structure, how much to save, what needs to be taken care of before investing and where the money should go. Without clarity, investing either gets pushed to the back seat or becomes a chase for high returns, without a real plan.

Let’s look at how someone earning Rs 1 lakh a month can approach saving and investing in a realistic way; starting with savings, taking care of their financial basics and finally focusing on sensible investment choices.

The idea is to move away from guesswork and build a system that is easy to follow and sustainable over the long term.

How much should you ideally save?

A simple and widely used budgeting framework is the 50-30-20 rule. It suggests dividing your income:

On a monthly income of Rs 1 lakh, this means a minimum saving of Rs 20,000. This is not an aggressive target, it is the baseline. The higher the better.

Consider Aman, a 25-year-old salaried professional earning Rs 1 lakh a month. After covering his expenses, he manages to save around Rs 15,000. While this is a decent start, going by the budgeting rule, it falls short of the 20 percent benchmark.

In such cases, the priority is not choosing better investments but gradually improving the savings rate by tightening expenses. Ideally, Aman should increase his monthly savings from Rs 15,000 to Rs 20,000.

Get the basics right

Before investment money, you need to set up a safety net. Think of it like wearing a seatbelt before driving.

For someone starting out like Aman, this includes: health insurance, life insurance (if needed) and an emergency fund.

Once these basics are in place, investing decisions become far more straightforward.

Start investing with clear goals

Before you start investing, it is important to define goals and timelines. Different goals require different approaches. And once you define the goal, the rest, how much to invest, where to invest, and for how long, gets easier.

So, define the goal first, then plan your investments around it.

Where should a first-time investor put money?

There is no single right answer, it depends on risk tolerance and time horizon. However, individual stocks can be risky for beginners. Mutual funds are often a better starting point, as they offer diversification and professional management.

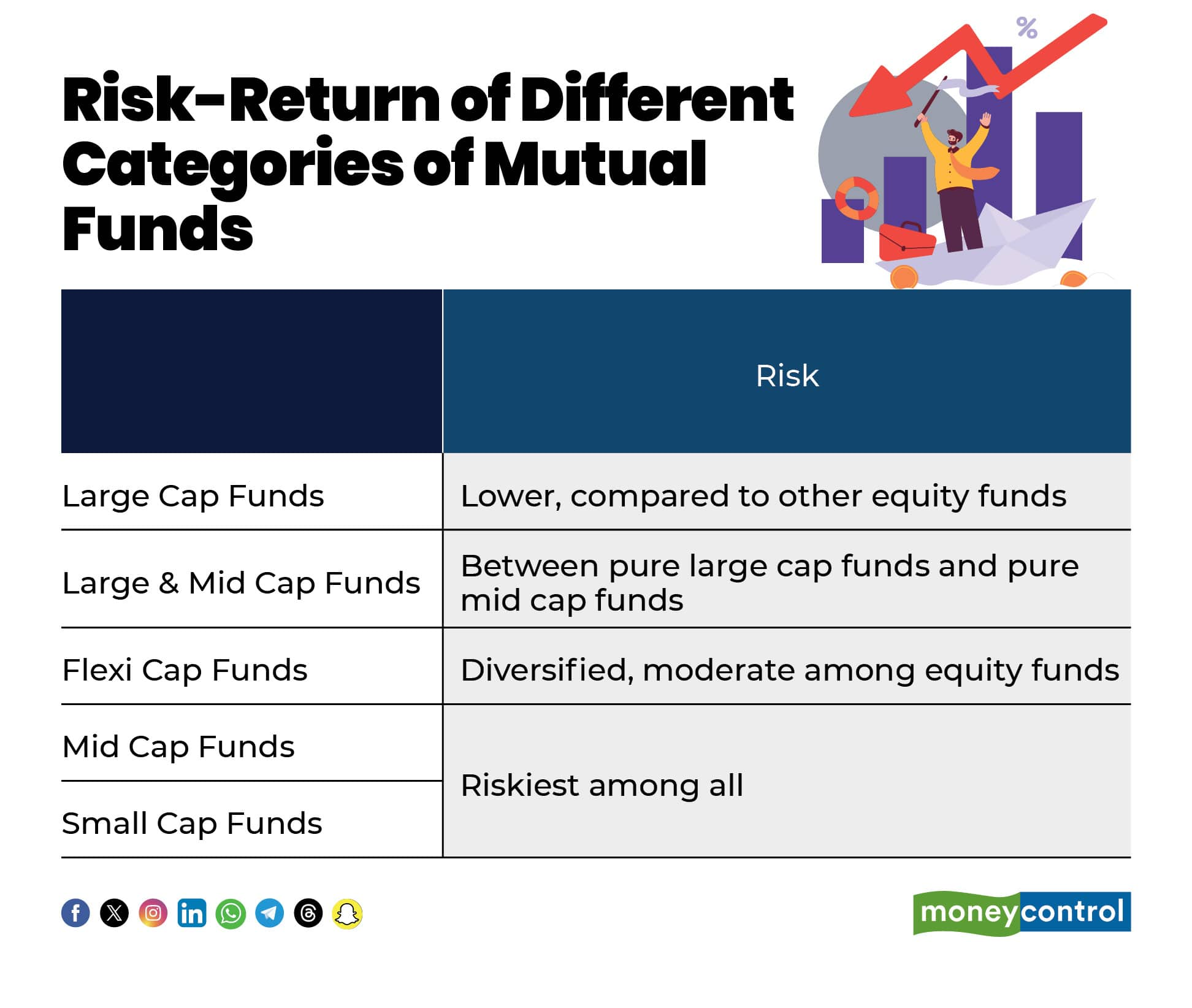

While you can choose from categories ranging from large and midcap funds to flexicap and smallcap funds, keep in mind that different mutual fund categories have delivered different returns over the years.

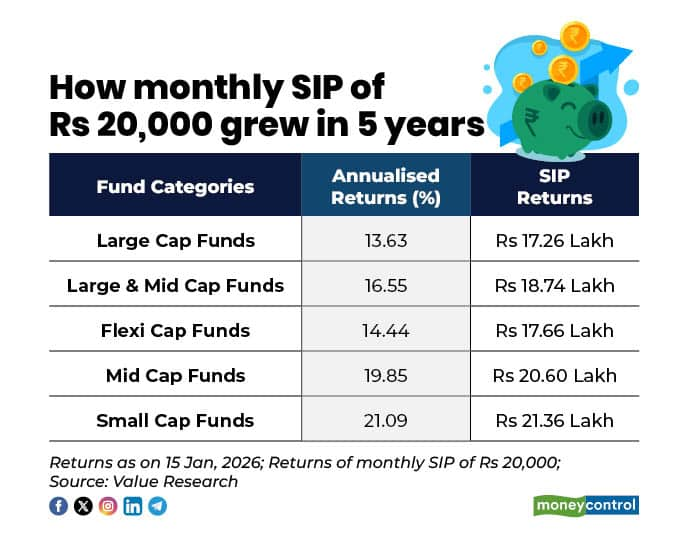

Over the past five years, returns across the most popular mutual fund categories show the clear difference. Smallcap funds delivered returns of over 21 percent, while largecap funds averaged around 13.70 percent. That’s a big gap.

Naturally, higher returns can translate into a larger corpus over time. For instance, at an average five-year return of 13.63 percent, a monthly SIP of Rs 20,000 in largecap funds would have grown to around Rs 17.26 lakh. In comparison, the same SIP in small-cap funds, with average returns of 21.09 percent, would have grown to over Rs 21 lakh.

But don’t get swayed just by high returns, there’s more to the story.

Higher returns come with higher volatility. While smallcap funds perform well in bull markets, they are also the most volatile. Mid and small-cap funds tend to fluctuate sharply during market downturns, which can be difficult for new investors to handle.

Beginner-friendly mutual fund options

For someone like Aman, who is just starting out, simpler fund categories are often more suitable.

1. Largecap index funds: These track India’s top 100 companies such as HDFC, Reliance and Infosys. They’re simple, low-cost and less volatile. These are ideal if you are ready to invest in equities with lower risk and some stability. In the past five years, they have delivered 13.63 percent SIP returns.

2. Dynamic asset allocation funds: These are a category of hybrid funds that switch between equity and debt depending on market conditions. They’re ideal for beginners who want to reduce volatility without missing out on returns. These funds have delivered 10.35 percent SIP return in the past 5 years.

3. Large and midcap funds: As the name suggests, these funds give the stability of largecaps and the growth potential of midcaps. They have delivered 16.55 percent SIP returns in the past five years. Suitable if you want to have some midcap exposure along with stability of largecaps. So, moderately risky equity funds.

4. Flexicap funds: If someone is willing to take a little risk, flexicap funds could work. They invest across large, mid, and small-cap companies as per the discretion of the fund manager, adding diversification and balancing both risk and return. In the past five years, these funds have delivered around 14.44 percent SIP return.

Keep it simple and start early

New investors often make the mistake of holding too many funds. Mutual funds are already diversified and a small number of well-chosen schemes is usually enough.

Starting early also matters. Even modest monthly investments, made consistently, can grow significantly over time due to compounding. Waiting for a higher salary often means missing out on those early years of growth.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.