Paying taxes is an unavoidable part of adult life. Anyone earning beyond the prescribed income limit, whether through salaried employment, self-employment, or running a business, has a tax obligation.

To ease this burden and promote long-term financial planning, the government allows several exemptions and deductions under Section 80 of the Income Tax Act. One such provision is Section 80CCD, which offers tax relief on contributions made to select government-approved pension schemes. Apart from lowering the tax outgo, these schemes also nudge individuals to build a retirement corpus in a disciplined manner.

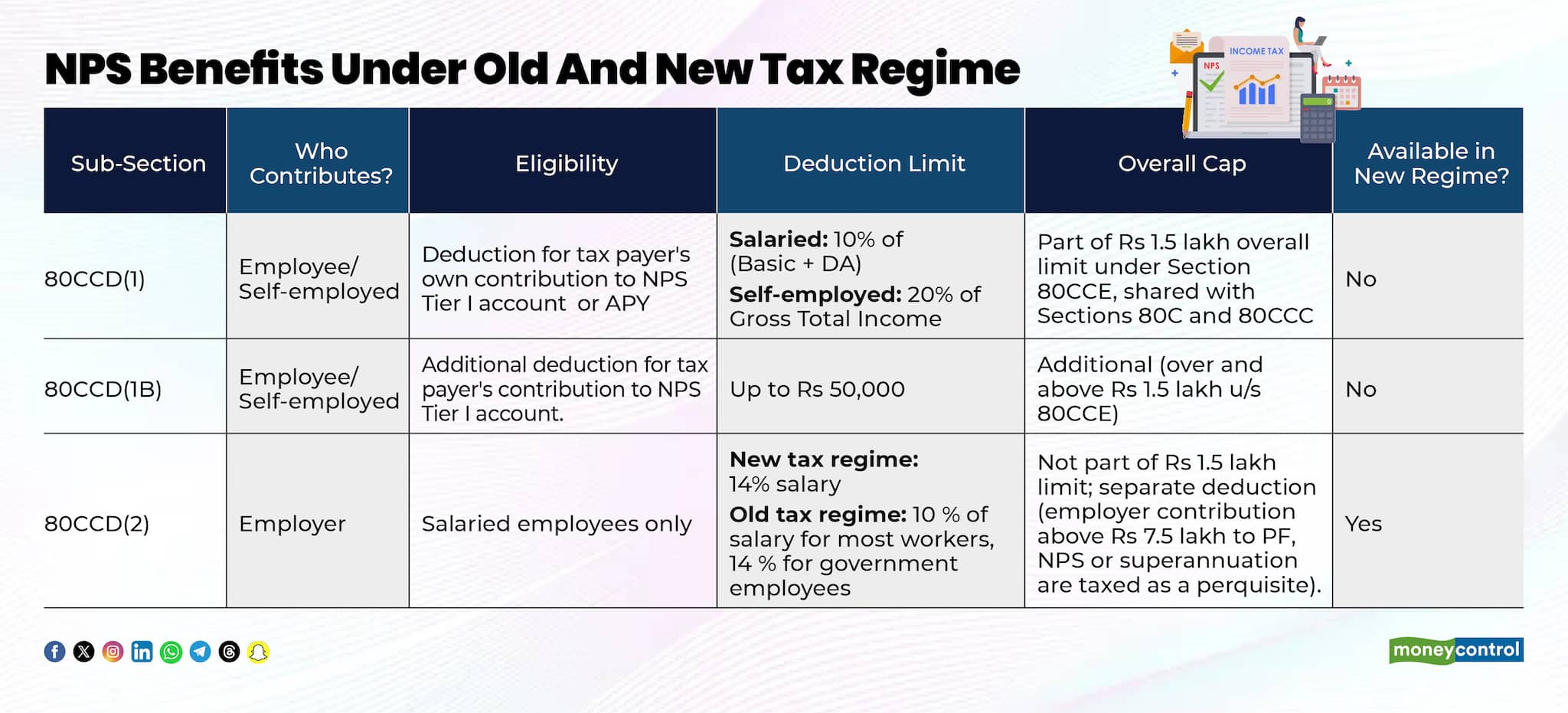

Understanding Section 80CCD

Section 80CCD provides tax deductions for amounts invested in pension schemes such as the National Pension System Tier-I account (NPS), the Unified Pension Scheme (UPS), and the Atal Pension Scheme. In the case of salaried individuals, both the employee’s own contribution and the employer’s contribution can be claimed as deductions, subject to the specified limits and income tax regime you opt for while filing your return.

Recently, the government clarified that all tax benefits currently available under NPS will also apply to the Unified Pension Scheme, bringing both schemes on an equal footing from a tax perspective.

Section 80CCD is divided into two subsections: Section 80CCD(1) and Section 80CCD(2). Section 80CCD (1) has a subsection called 80CCD(1B).

Benefits 80CCD under old tax regime

If an Individual opts to follow the old tax regime, then they can claim a benefit for contributions to an approved pension scheme as under:

Under 80CCD(1) - Salaried employee or self-employed can contribute to NPS up to 10 percent of their salary or 20 percent of their gross total income respectively, and claim deduction under section 80CCD(1).

Point to note is that the aggregate deduction under this section along-with deduction under section 80C (provides deductions up to Rs 1,50,000 on various investments and expenses) and 80CCC (offers tax deductions up to Rs 1,50,000 per year for contributions made by a person towards certain pension funds), shall be restricted to Rs 1,50,000.

Under 80CCD(1B) - Salaried employee or self-employed can claim extra deduction of up to Rs 50,000 under section 80CCD(1B) for NPS contribution for which deduction has not been claimed under section 80CCD(1). Further, the amount contributed by a taxpayer to NPS Vatsalya accounts for their minor children is also allowed within the overall limit of Rs 50,000.

Under the old tax regime, the maximum deduction for an employee’s own contribution works like this:

You can claim up to Rs 1,50,000 in total under Section 80C, 80CCC, and 80CCD(1) combined. Over and above this, Section 80CCD(1B) allows an additional Rs 50,000 deduction exclusively for NPS contributions.

Benefits of 80CCD under new tax regime

Employees who opt for new tax regime cannot claim deduction under section 80CCD(1) and 80CCD(1B) but can claim deduction under section 80CCD(2) with increased employer contribution limit from 10 percent to 14 percent in case of non-government employees.

Under 80CCD(2) - The tax benefit under Section 80CCD(2) varies depending on whether the taxpayer has opted for the old or the new tax regime. This provision allows a deduction only for the contribution made by the employer to the National Pension System. Under the new tax regime, the employer’s contribution is deductible up to 14 per cent of salary, calculated as basic pay plus dearness allowance.In the old regime, the limit for private-sector employees is restricted to 10 per cent of salary, while Central and State government employees are permitted to claim a deduction of up to 14 per cent under both regimes.

Since the deduction applies exclusively to employer-funded contributions, self-employed individuals are not eligible to claim any benefit under this section.

“Contribution made by employer to employee’s NPS (14 percent of salary where employer is central or state government, and 10 percent in case of other employer) is allowed deduction under section 80CCD(2). However, employees should be aware that aggregate contribution in excess of Rs 7,50,000 by an employer in a recognised provident fund, NPS Scheme and approved superannuation fund of an employee would be treated as a perquisite and would be liable to tax as salary income,” said Gopal Bohra, Partner -Tax, N.A.Shah Associates.

Contributions made to newer variants such as the Unified Pension Scheme and NPS Vatsalya are also recognised for deduction under Section 80CCD.

“From a long term savings and retirement planning perspective, the Pension Schemes certainly offer a good option to Individuals – those who get a tax break would get a slightly better rate of return as compared to those who would be denied tax breaks due to the new tax regime and its lower rates,” said Apurva Shah, CA & Managing Council Member of The Chamber of Tax Consultants.

“Investors are, however, advised not just go by the tax saved now but to ask a planner to visualise the returns that will be generated in the future and consider that with alternative investment options. Many organisations though, would insist on a Pension Contribution to be a part of the Salary package,” Shah said.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.