Exchange traded fund (ETFs) are generating interest, even as investors continue to shy away from equity schemes. In August, ETFs saw net inflows of Rs 1,721 crore, while equity schemes witnessed net outflows of nearly Rs 4,000 crore, as per figures released by the Association of Mutual Funds of India on Wednesday.

Industry experts say investors’ awareness of ETFs has improved due to the stagnant returns given by actively-managed equity schemes in the past.

“The ETF category has been consistently receiving net inflows. New ETFs are also being launched. With many actively-managed funds struggling to outperform benchmark indices, investors have seemingly turned their focus to ETFs,” says Himanshu Srivastava, Associate Director-Manager Research, Morningstar India.

To be sure, a large chunk of ETF flows is coming through the Employees’ Provident Fund Organisation. But the uncertainty in the markets has aroused retail investors’ interest in ETFs.

Over the past two years, mutual funds (MFs) have started offering a wider range of ETFs: smart-beta products, mid-cap, sectoral and those linked to the US markets. In August, HDFC MF floated a banking ETF. ICICI MF rolled out an ETF focusing on the information technology (IT) sector and also an Alpha Low Vol 30 ETF in August.

The latter is a multi-factor ETF, tracking the Nifty Alpha Low Volatility 30 Index. The index consists of 30 stocks that are selected through a rule-based system. Such rule-based ETFs are known as smart-beta products. Fund houses now work closely with index manufacturers too, to incorporate rules that decide inclusions and exclusions.

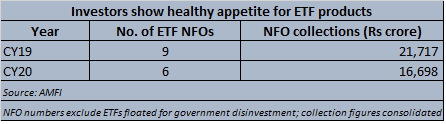

In the current calendar year, as many as six ETF NFOs have been rolled out. This excludes any ETF NFO launched as part of the government’s disinvestment programme. Collectively, ETF NFOs have garnered Rs 16,698 crore in CY20.

An actively-managed equity scheme involves a fund manager ‘actively’ buying and selling stocks. This is done with the aim of outperforming the scheme’s benchmark index.

In ETFs, the investments of the underlying portfolio are pre-determined, as they mimic an index of stocks. Further, the entry and exit of stocks in an ETF take place as and when the index is re-balanced. Therefore, ETFs are considered passive products.

What works for ETFs Experts say ETFs can come in handy for investors, especially when there is uncertainty over the economy and markets.

“Right now, there is lack of clarity on when the economy will start to recover and which stocks and sectors would be better-placed to ride the recovery. An easier way for investors to participate in the market would be to pick the most visible index in the market such as the Nifty,” says Vishal Jain, Head-ETF, Nippon Life India Asset Management.

Fund houses say that that Nifty-linked ETFs have gained traction in recent months. “The Nifty index has top-50 companies in India. If these companies cannot survive the economic uncertainty, then who will. We have seen lot of money coming into ETFs in last couple of months and new set of investors coming in,” Jain added.

The total expense ratios or TERs -- as known in MF industry parlance -- are much lower on ETFs than those on actively-managed equity schemes.

This is because the TER of an active fund, accounts for the fund management fee, which is not the case with an ETF.

For instance, TER of a Nifty ETF can be as low as 0.05 per cent, while that of large-cap active fund can be 0.5 per cent or higher, depending upon the asset size.

Watch for high impact cost and tracking error The lack of liquidity has remained an Achilles’ heel for the growth of ETFs. As a result, ETFs witness high impact costs. So, when an investor places an order for buying units of the ETF, she may not be able to buy her entire lot at the lowest available price. This could happen when the ETF is thinly traded, and a new buy order itself leads to higher prices. In a liquid market, the impact costs are minimal, as buying and selling happens at almost every price point.

Investors can also face challenges when ETFs start to show wide tracking errors. This is prone to happen when markets are highly volatile. For instance, when Nifty saw a sharp fall on March 16, ETFs couldn’t mimic the fall as they were supposed to. Some ETFs saw a limited dip or in some cases they closed in the positive terrain.

This can also happen when markets see a sharp upmove, and ETFs are unable to capture that fully.

Such divergences can make it difficult for investors to gain from market correction and deploy additional funds, as well as exit their ETF position in time to capitalise when markets recover.

For now though, investors appear to be taking refuge – partly if not fully – in ETFs. With more fund houses taking to ETFs, the menu can only get larger.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.