The Reserve Bank of India (RBI) Governor Shaktikanta Das said in his monetary policy statement on September 30 that India's consumer price index (CPI) remains "elevated" due to large adverse supply shocks.

The inflation rate in June as measured by the Consumer Price Index came in at 7.01 percent, the highest in around eight years. This means that prices have risen by around that much over the past one-year period.

Das also added that the CPI is "above the tolerance band" due to the firming up of domestic demand and spillovers from global markets. The monetary policy has largely maintained the inflation forecast for all the remaining quarters of FY23 and the first quarter of FY24.

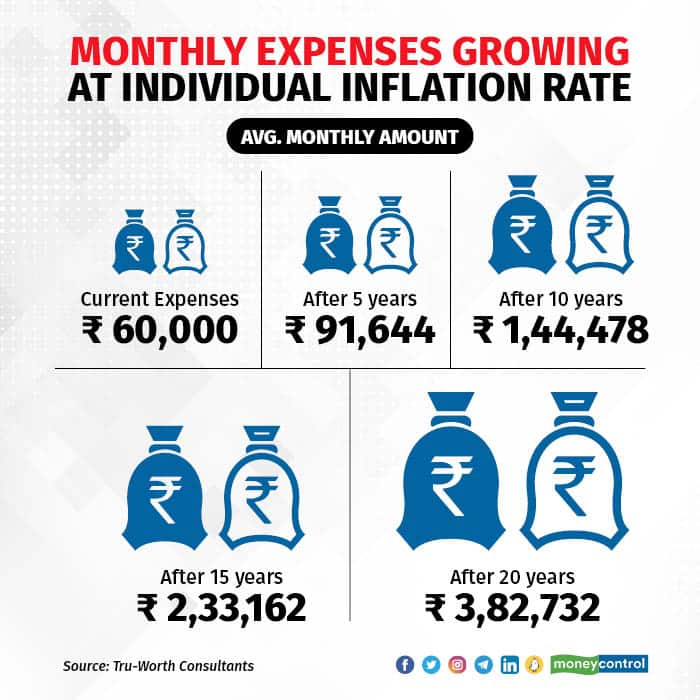

To put it simply: if your current monthly expenses are around Rs 60,000, at the current rate of inflation, in 10 years’ time you would need around Rs 1.44 lakh per month to buy the same goods and services; after 15 years, you’d need Rs 2.33 lakh per month. In short, inflation reduces the purchasing power of your money.

That is why financial planners often factor in inflation for various goals one saves money for. But how much inflation should you really budget for? Would prices of all commodities and lifestyle spends rise by that much?

Thr rise of monthly expenses over time

Thr rise of monthly expenses over timeIn May 2022, vegetable prices rose at 18.3 per cent. Medical and educational expenses apart from the cost of travel also rose at a faster pace. “While planning for future expenses, we consider grocery to rise at 6 percent, education expenses at 10 percent, holiday planning at 8 percent and so on,” said Tivesh Shah, financial consultant and founder, Tru-Worth Finsultants.

But he adds that over the past two years these numbers have been further elevated by 2 percentage points, across categories <see graphic>.

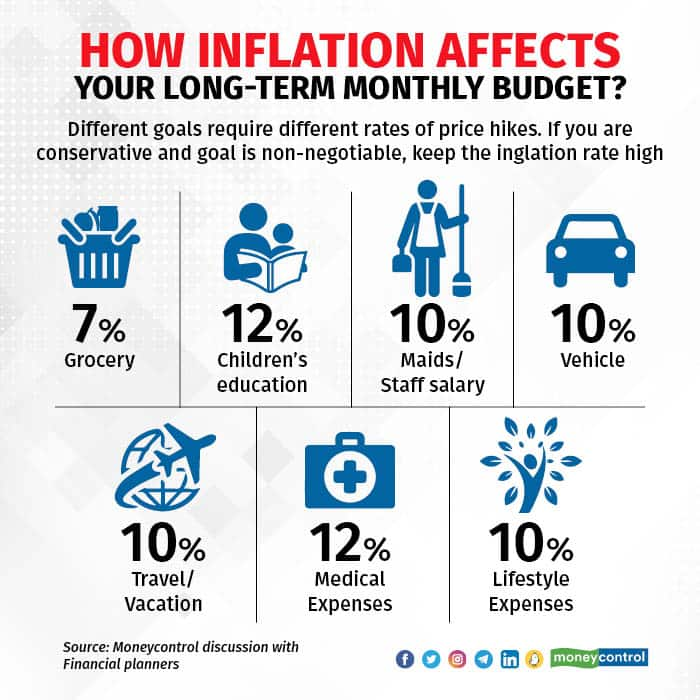

While planning for future expenses, consider how prices of different items rise..Medical inflation

While planning for future expenses, consider how prices of different items rise..Medical inflationIn a rising inflation scenario, higher costs of healthcare services need to be planned for. “Medical inflation rates reached a peak of 20-22 per cent during COVID,” said Adarsh Agarwal, chief distribution officer at Digit Insurance, a Bengaluru-based General Insurance Company.

Health insurance costs, too, escalated. A Mercer Marsh Benefits report says that premiums for company health coverage increased by 15 percent in 2022, the steepest rise in Asia.

But planners have been factoring in medical inflation at 12 percent. So should financial planners factor in a higher rate of inflation for health insurance?

Also read | Prices of medicines used to treat common ailments set to increase steeply this year

“Rates will not stay at this level. While choosing an insurance plan, one should consider 11-12 percent inflation in medical costs. A basic cover of Rs 15-20 lakh can be opted for and a top-up cover that enhances the sum assured by 15-20 percent every two years would help with sum-assured sufficiency,” said Agarwal.

"We observed that the overall claim cost escalation saw a rise of more than 30% in the first year of the pandemic which can be attributed to hospitals administering some pandemic related basic necessary tests and hygiene. This was moderated to close to 10% inflation in the subsequent year. In line with the medical inflation which happens year-on-year, it is imperative that customers should consider this while choosing the adequate sum insured whilst buying a health insurance policy so that they are safeguarded against any medical exigencies and at the same time avail of quality medical treatment without exhausting their savings,” says Bhaskar Nerurkar, Head – Health Administration Team, Bajaj Allianz General Insurance.

Vivek Damani, founder, Jeevan Prabandhan, a Mumbai-based financial services firm, suggests a separate medical emergency fund “as a large part of medical bills are not covered under insurance”.

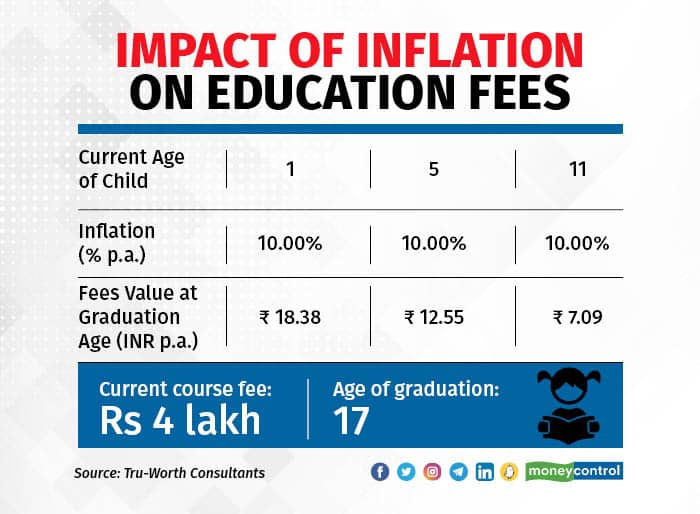

Educational inflationJust like medical expenses, school and college fees also go up. Since these expenses cannot be compromised on, financial planners advise greater conservatism. Damani says that while factoring in education goals, you must budget costs to go up by at least 12-15 percent even though general inflation in the country hovers at around 7 percent.

Education inflations rises at a higher rate than the common and consolidated inflation rate that gets declared. Take a higher inflation rate to be on conservative side.

Education inflations rises at a higher rate than the common and consolidated inflation rate that gets declared. Take a higher inflation rate to be on conservative side.If it’s foreign education, make sure your budgeting widens and you save more and expect an inflation rate steeper than that.

Also Read: Looking out for international scholarships. Here is how to maximise your chances

Lifestyle expensesShah points out that lifestyle expenses also tend rise as income levels and aspirations go up. “Men, who weren’t much into grooming earlier, now spend on grooming and self-upkeep.

Fitness and gym fees too have been added to the monthly budget after COVID. Smartphones for each family member have to be replaced in a couple of years,” he said, all pointing to the need to budget for higher inflation.

Despite factoring in higher costs, things might still go out of hand. “An Indian postgraduation dream might get turned into a foreign education dream. A simple wedding financial goal might need an upgrade if the family now wants a destination wedding,” said Suresh Sadagopan, founder of Ladder7 Financial Advisory.

How to avoid disappointmentsHere are three tips to consider the right inflation rate to ensure that your financial goals are met:

Higher corpus: Try and invest more than you think you can. When most of us begin our investment journey, we fear unexpected expenses and budget for liquidity, sometimes a bit too much. Work around the higher expenses, but don’t stop your investments. “With the increase in expenses, the surplus can be affected and hence we keep a margin. So, if a person with Rs 2.5 lakh monthly income can manage saving Rs 1 lakh-plus, we commit systematic investment plans of Rs 70,000 to Rs 80,000,” said Sadagopan.

Reducing returns: Be conservative when it comes to projecting returns in your financial plan. Many financial planners that Moneycontrol spoke to told us that in the past, they used to project an expected return from equity investments of about 15 percent. Not anymore. Now, many plan for a 12 percent equity return.

Shah prefers to be still more conservative. “The rate of return from equity and mutual funds is being factored in at 10-11 percent as the overall global economy has been seeing slow progress and the rate of growth would be lower. Due to inflation the input costs for businesses would be high and their profitability could be affected,” says Shah.

Even debt fund returns have gone down in recent years, from around 9 percent to 4 percent.

Save well in the earning years: Invest more, and then incrementally more. Vivek Rege, founder and CEO, VR Wealth Advisors, says it’s important to save more while you are working. “High inflation could affect your finances when the active phase is over and you realise that the money spent during the income years could have been saved,” he said.

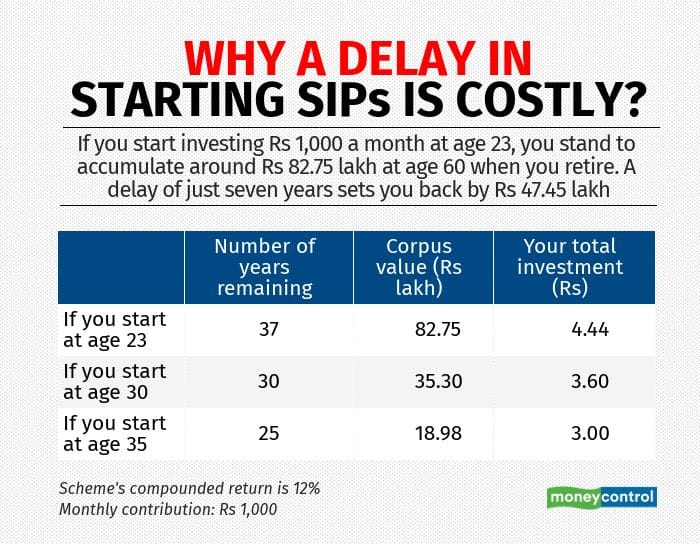

A delay in SIPs can cost you heavily in later years

A delay in SIPs can cost you heavily in later yearsThe earning period for many, too, continues to shrink due to burnout or other reasons. A forced early retirement also shortens the period to build that nest egg.

Also Read: Cost Inflation Index enables big tax savings

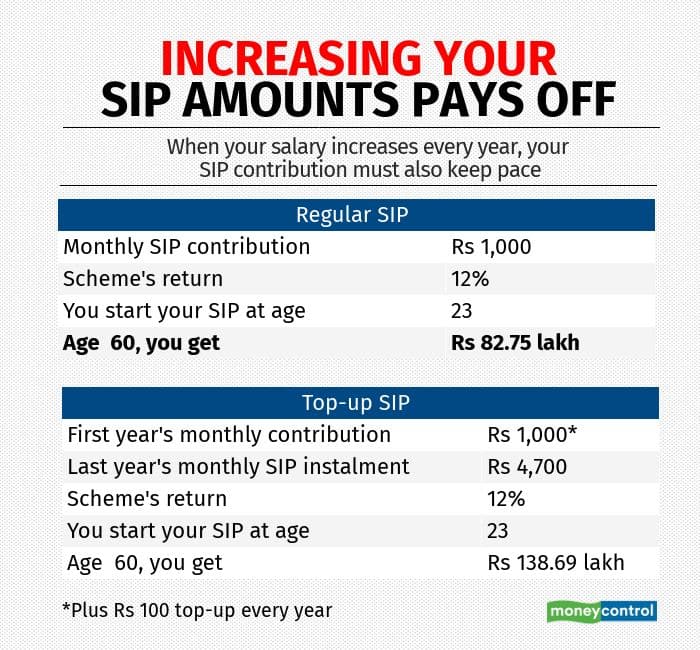

Topping up your SIPs, even once a year, gets you closer to your financial goalsInflation is not all bad

Topping up your SIPs, even once a year, gets you closer to your financial goalsInflation is not all badIf inflation can reduce the purchasing power of your money, it can also help you save taxes. That's because it also reduces profits from selling different assets like equities, debt mutual funds, gold jewellery and real estate to calculate the tax you need to pay, especially if you have stayed invested for more than two years in real estate and three years in debt mutual funds. This is called indexation benefits.

In simple words, indexation artificially inflates the cost price of your asset. This ensures that, at least on paper, the difference between your selling price and cost price reduces and you pay less tax on the capital gains.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.