Surging costs of hospital stays, diagnostics and doctor visits are forcing more and more people to buy health insurance but buyers are unsure about the right mix, one that provides adequate protection without high premium costs.

In the market, there are broadly two types of health insurance policies. One is a standalone health insurance policy, also known as a base health policy, and the other is a super top-up plan, which comes with a threshold limit, commonly known as a deductible.

Base health policy

A base health policy is the primary cover that covers hospital bills up to the sum insured and includes features such as cashless treatment, pre and post-hospitalisation cover and no-claim bonuses.

"A higher sum insured under the base policy provides greater coverage from the very first claim, without any deductible. This is very important for managing typical hospitalisations and ensures smooth settlement of claims," said Naval Goel, Founder and CEO of PolicyX.com.

Typically, many policyholders opted for a cover of Rs 3 lakh to Rs 5 lakh. However, with medical inflation remaining high, experts suggest this amount can be exhausted very quickly during a serious illness or a complex surgery. Hence, one should ideally opt for a sum insured of at least 10 lakh under their base cover.

BajajCapital Ltd joint chairman and MD Sanjiv Bajaj said, "Premium optimisation is sensible but peace of mind should never be traded away quietly. The goal is to feel secure, not to feel smart until the first claim arrives."

This means reducing the sum insured under the base health cover can lower premiums but it also increases your financial exposure for initial hospital expenses. Insurers generally allow changes at renewal.

"In cities where treatment costs are high, a lower base cover may not be sufficient even for a single major hospitalisation. Before making this shift, assess average medical costs and your comfort with out-of-pocket payments. The base cover should remain strong enough to manage routine and moderate claims," Goel said.

So , if you want to lower your premium and get good coverage, you can do so by opting for super-top plans. In such cases, your premium can be adjusted to a certain level but you must watch for gaps when opting for such plans.

What are super top-up plans?

Super top-up health insurance is an add-on policy that provides extra medical cover beyond your chosen limit (deductible) once it is exceeded in a year. It is mainly used to increase the total health cover at a low premium. Therefore, these plans only pay after the policyholder’s deductible has been met on an aggregate basis across the year.

"If the policyholder’s base health policy partially settles a claim, their super top-up might not trigger because the deductible wasn't formally exhausted. The deductible must match or be less than the policyholder’s base health policy’s sum insured. Otherwise, there will be an uncovered gap," said Siddharth Singhal, business head of health insurance at Policybazaar.com.

How to plan?

Suppose you have a base health insurance policy with a sum insured of Rs 10 lakh. With medical inflation remaining high, this amount can be exhausted quickly during a serious illness or a complex surgery. So, what should you do? This is where a super top-up plan comes in. It provides additional coverage once you pay an amount up to the deductible limit.

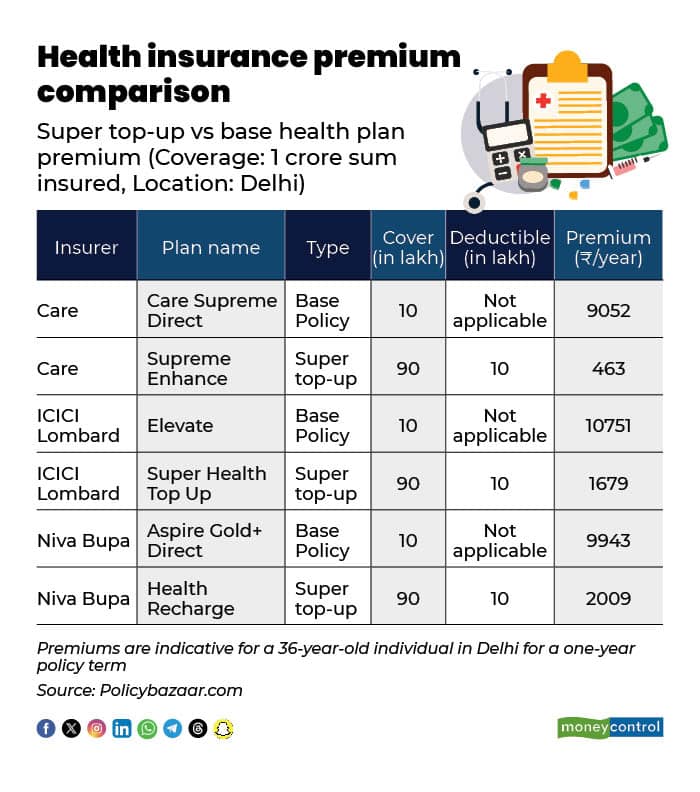

For instance, if you have a base policy of Rs 10 lakh and want a super top-up of Rs 25 lakh, you must opt for a Rs 10 lakh deductible under your super top-up plan. The base health policy will pay the first Rs 10 lakh (which is your deductible under the super top-up plan), and then the super top-up takes care of the remaining expenses. The biggest advantage is cost efficiency. A large super top-up cover is far cheaper than buying a high base policy of the same size.

"Super top-ups are significantly cheaper for the same total coverage — a base plus top-up combo costs roughly 60 percent of an equivalent standalone high base health policy," Singhal said.

What is the right mix?

The right strategy would be to first arrange a base health plan that comfortably covers hospitalisation bills in your city. After that, a super top-up plan can be layered to safeguard against high-value medical emergencies at a relatively low cost.

"It is advisable not to drop the base below Rs 5 lakh in metros or Rs 3 lakh in smaller cities, as hospital costs for moderate procedures can leave the policyholders bearing major financial stress. Two policies also mean two claims, and if the base insurer is low, the top-up claim will wait until then," added Singhal.

Choose an insurer based on your city's cashless network and coverage. Avoid room rent caps, get restoration benefits, so one claim doesn't exhaust the family cover, and skip maternity if you are not planning more kids.

Keep the same insurer for both the base health policy and super top-up plan, if possible, to reduce gaps. "For most middle-class families aged around 35-40, a moderate base (Rs 10 lakh base plus Rs 25 lakh super top-up) with a large super top-up is most cost-efficient. Choose pure high base only if simplicity and single insurer cashless access matter more than saving money," Singhal said.

You must also consider choosing a high base if you live in a metro where routine procedures cost several lakhs. This way, a higher base cover reduces friction. It limits deductibles, simplifies settlement, and ensures that most hospitalisations are handled without second thoughts.

"The two are not alternatives. They serve different emotional and financial roles. A sensible choice is not about maximising one over the other. It is about ensuring that everyday medical needs are handled smoothly, while rare, high-cost situations are never overwhelming," said Bajaj.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.