The second wave of the COVID-19 pandemic and the partial lockdown being announced in some of the states are bringing back fears of last year’s events. Salaried borrowers struggled to repay loan instalments every month. Companies had laid-off employees or reduced salaries. To provide financial-aid, there was a loan moratorium announced for the individual borrowers by the Reserve Bank of India (RBI) from March to August 2020. But, there were several instances of borrowers being unable to repay loan instalments on time. And borrowers had reached out to the respective banks for loan restructuring.

Numerous salaried borrowers fell into a debt trap by taking pay-day loan schemes, personal loans from fintech lenders and revolving credit card dues at higher interest rates (between 36 and 48 per cent per annum). Now, if your source of income seem dries up due to fresh lockdown curbs, it may be difficult to service multiple debts. In these situations, a salaried borrower can seek initiation of insolvency and bankruptcy proceedings in respect of outstanding debts in the event of his/ her inability to repay loans when they become due.

We will discuss the existing bankruptcy law, process to apply and how it’s expected to benefit individuals under the Insolvency and Bankruptcy Code (IBC).

Also read: COVID-19: Money lessons for the second wave from the first

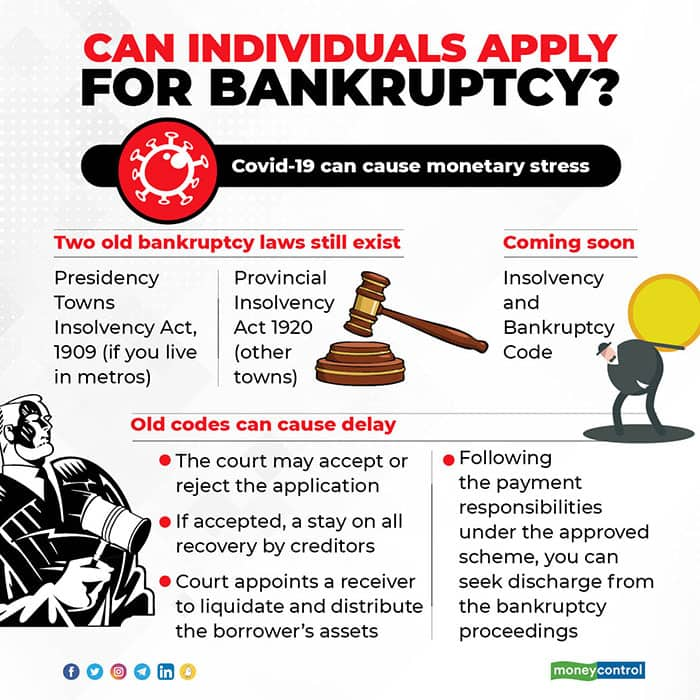

Applying for the bankruptcy processIf you reside in metropolitan cities such as Chennai, Kolkata or Mumbai, you can file for insolvency under the Presidency Towns Insolvency Act, 1909. But if you live in any other city of India, then you can file for insolvency under the Provincial Insolvency Act 1920. Both the acts are similar and you can file for bankruptcy if you are unable to repay debt exceeding Rs 500.

Every insolvency petition has to be presented by a person before the high court or district court as per the jurisdiction under the acts, depending on where the person usually resides/ is engaged in gainful employment. After analysing whether the conditions for filing of bankruptcy have been met, the concerned court may accept or reject the application filed by the debtor.

“Upon admission of the application for bankruptcy, the court, at its sole discretion, may grant a stay on any legal proceedings against the property or assets of the debtor,” says Y Sriniwas Arun, Partner at Link Legal. In other words, there would be a stay on all recovery proceedings from your creditors, till such time as the insolvency proceedings continue.

Zulfiquar Memon, Managing Partner at MZM Legal says, “After the application/ petition is accepted, the competent court appoints a receiver for the assets of the individual debtor (borrower) who shall then proceed to liquidate and distribute the assets of the borrower, unless a compromise or settlement is arrived at between the parties.”

Following the payment obligations under the approved scheme of arrangement / composition ensures you can seek discharge from the bankruptcy proceedings. This will allow you to build your finances afresh. You won’t be chased by your previous creditors. But remember, you won’t be discharged from any debt due to government or any debt incurred due to fraudulent activity under these acts.

Arun says, “The filing for bankruptcy by individuals and the underlying documents required for such filing is not the same across jurisdictions in these acts, the current law is outdated, lacks transparency and does not adhere to timelines for resolution of financial stress which is the essence of any insolvency proceedings.” The Insolvency and Bankruptcy Code, 2016 (IBC), which proposes a streamlined and transparent process for conduct and conclusion of individual insolvency proceedings in a time-bound manner by repealing the existing acts, is yet to be notified.

Also read: Stood as guarantor? Know how to protect yourself if the borrower defaults on loans

Illustration of how existing insolvency act worksWhen you file for the insolvency under the Presidency Towns Insolvency Act, 1909, the possession of the assets shall be taken over by the receiver/ assignee appointed by the court. Then a repayment plan will be considered, prepared and placed before the creditors.

Then a plan is prepared for payments to your creditors as full and final discharge of all your obligations in a phased manner.

What will change when IBC for individuals becomes effective?“In my opinion existing acts are obsolete and more harmful to individuals and creditors, as the individual debtor can get away from a lot of credit liabilities with such a low threshold,” says Memon. Similarly, creditors can threaten individuals under such obsolete laws and wrongly seize individual assets. So, legal experts are suggesting that the replacement of these laws with IBC is extremely important for bringing in a streamlined and transparent process to individual insolvency. Section 243 of the IBC provides for repeal of the existing insolvency laws. However, this section has not yet been notified. So, petitions for insolvency can be filed by individuals under the existing laws until this section of IBC is brought into effect by the Central Government.

Shreni Shetty, partner at ANB Legal says, “First, under IBC, the proceedings are expected to be conducted in a transparent and time bound manner. Second, once the application is admitted by the Adjudicating Authority it will provide you automatic moratorium on debt repayment until it’s restructured.” Under existing laws, stay on a debt recovery is decided by the court.

With partial lockdown being announced in several states, debt is expected to increase for individuals. This will lead to a rise in delinquencies and bankruptcies. So, it’s important to have IBC in place sooner rather than later for a quick bankruptcy process. This will help several borrowers restore their financial and credit worthiness.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.