Navin Fluorine International (market capitalisation: Rs 3,762 crore), one of the largest chemical companies in the fluorine value chain, exhibited moderate growth in the fourth quarter of last fiscal, backed by contract research and commodity end markets but was partially offset by sluggish agri-chemicals. Read: Navin Fluorine: Leading player in the transformative chemistry of fluorine

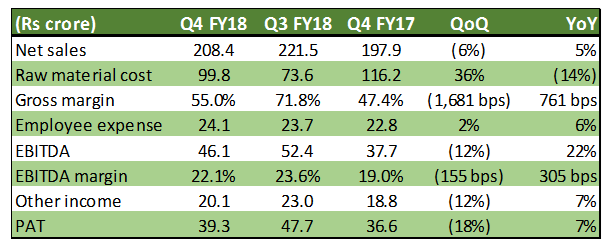

Q4 result updateNavin’s Q4 FY18 sales were up five percent year-on-year (YoY) aided by value growth in inorganic fluorides (29 percent YoY) and contract research and manufacturing services (CRAMS, 32 percent YoY). Its refrigerant gas business was up 17 percent YoY led by pricing and exports. Performance of its specialty chemicals business was weak on account of headwinds faced by global agrochemical companies.

Gross margin improved YoY, but there was a sharp contraction sequentially due to a 36 percent YoY increase in raw material prices. Moderate increase in employee cost, however, cushioned the impact on EBITDA margin.

Manchester Organics under transitionNavin said its subsidiary, Manchester Organics, had a tough year due to management-related changes. Enterprise resource planning (ERP) investments have also impacted the bottomline. However, the management is hopeful that its core business would normalise in a couple of quarters.

Capex for Dewas unitCapex (Rs 115 crore) for additional current good manufacturing practice (cGMP regulations as enforced by the US Food and Drug Administration) for its Dewas facility is on track and expected to come onstream by June next year. The new capacity would be utilised for the contract manufacturing of value-added complex chemicals and fluoro intermediates used by global pharma chemical entities.

Elevated raw material pricesIn the last couple of quarters, fluorspar prices have shot up and so have the prices of bromine, chloroform and sulphur. The management expects raw material prices to remain elevated in the near- to medium-term.

Overall quarterly result was inline with expectations as far as the traction of various business units are concerned. The refrigerant gases business is expected to benefit from higher pricing going forward. Improving end market (steel, oil & gas), exports and lower supply from China is expected to boost the inorganic fluoride business. CRAMS business has emerged as the management’s focus area. However, a slowdown in operations at its joint-venture with Piramal Enterprises and Manchester Organics needs to be watched. Its specialty chemicals business remains a laggard in the near-term.

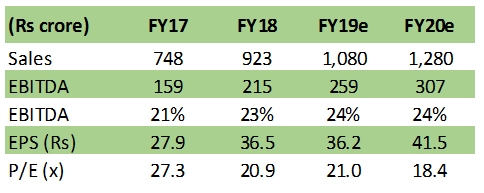

Navin is a beneficiary of strong entry barriers in the fluoro-chemical value chain, management’s focus on high margin contract research and steady cash flow generation. It therefore remains an accumulation candidate as the stock trades at 21 times FY19e earnings, inline with the sector average.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.