Nitin Agrawal

Moneycontrol Research

Highlights:

- Decent topline growth in Q3 FY19

- Operating margin continues to remain under pressure

- Short-term business outlook weak, positive for the long term

--------------------------------------------------

Motherson Sumi Systems (MSSL), India’s largest automotive wiring harness company and one of the largest domestic automobile ancillary players, posted in line set of Q3 FY19 earnings on the back of a demand slowdown in both domestic and international markets and margin contraction for Samvardhana Motherson Peguform (SMP) and its India business.

The capex cycle is coming to an end and ramping up of new plants is expected to result in an increase in operating leverage. This, coupled with the push towards electric vehicles (EV) and transition towards Bharat Stage-VI (BS-VI) emission norms should result in healthy growth in the topline and gradual increase in margin. MSSL is currently trading at reasonable valuations, which warrants investor attention.

Quarter in a nutshell

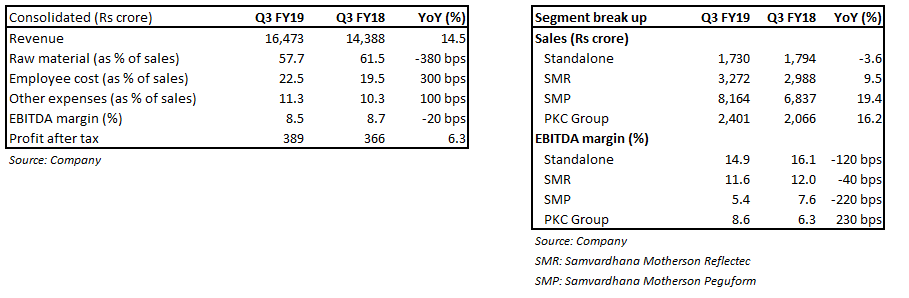

While the company posted a year-on-year (YoY) growth of 14.5 percent in its consolidated net revenue, earnings before interest, tax, depreciation and amortisation (EBITDA) margin was marred by poor operating performance for SMP, Samvardhana Motherson Reflectec (SMR) and its Indian business.

Segment-wise, the standalone business witnessed a 3.6 percent revenue decline, led by a 6.9 percent decline in domestic business, which was on the back of subdued domestic consumer sentiment. International business, however, saw a 15.5 percent increase in revenue.

EBITDA margin contracted 120 basis points (100 bps=1 percentage point) to 14.9 percent, which is at multi-quarter lows. The contraction was led by a weaker dollar-rupee and rise in raw material prices, which got partially offset by cost control measures taken by the management.

SMP, which is into modules and polymer component business, is a leading global supplier of door and instrument panels and bumpers. The business saw its revenue decline 2.3 percent in euro terms, on subdued demand post-implementation of Worldwide Harmonised Light Vehicle Test (WLTP) norms. EBITDA margin fell 30 bps due to cost of setting new plants and negative operating leverage.

SMR, a leading global supplier of exterior mirrors, saw its revenue grow 1.5 percent in euro terms and EBITDA margin contract 40 bps YoY.

In euro terms, revenue for PKC, a Finland-based wiring harness specialist company) grew 7.7 percent. The business was impacted by weak demand from the eurozone. EBITDA margin contracted 20 bps on negative operating leverage.

Factors to watch out for

Expansion on track

The company has set up 33 new plants in the last four years to meet its growing order book. The management said production will commence at Tuscaloosa in Q4 and that all key greenfield projects are now complete and are in a ramp-up phase now. Once the ramp-up is complete, operating leverage will kick-in, thus contributing to margin expansion.

PKC: The key future growth driver

Integration of PKC has been happening smoothly as is evident from the strong growth during Q3 on the back of healthy traction coming in from the North American (NA) and European truck market. It commands a 62 percent market share in NA Class 8 (really heavy trucks) truck wiring harness and 54 percent of its revenue accrues from there. PKC is also aggressively targeting the China truck market and has already ventured into three joint-ventures catering to different customers. It has received a 280 million euro order from Bombardier and is in discussion with various original equipment manufacturers to develop and supply electric system.

EVs an important growth driver

Given the global focus on EVs, this segment would be an important growth driver for the company going forward. As per the management, battery driven vehicles would need more wiring components, which would increase content per vehicle by close to 10-20 percent. Other businesses related to polymer and mirror-based products are immune to the shift to EVs.

India business outlook

Demand outlook continues to be muted for the passenger vehicle (PV) segment in India. Wiring harness demand, however, is expected to outperform PV industry growth driven by increase in content per vehicle and new product launches. In fact, implementation of BS-VI emission norms would lead to complexity in wiring harness and consequently value. MSSL is in a strong position to take advantage of the growth accruing in the domestic PV segment.

Debt starts to fall

Rising debt levels on the back of its amplified capex plans and the quest to grow the business inorganically has been a concern for MSSL. With the capex cycle coming to an end, the company has started paying off its debt and repaid Rs 1,600 crore in Q3. Its net debt has now fallen to Rs 9,705 crore as of December-end.

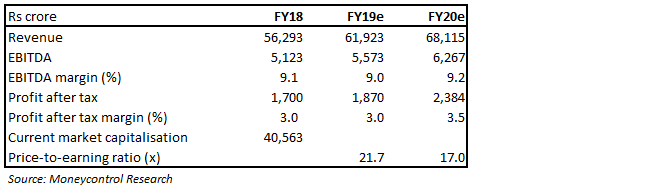

ValuationsIn light of subdued demand and outlook, the stock has corrected quite significantly and down 48 percent from its 52-week high, making valuations reasonable. The stock currently trades at 21.7 times FY19 and 17 times FY20 projected earnings. We advise investors to accumulate this business in staggered manner.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!