We had initiated the coverage on Minda Corporation (Minda), a well-diversified auto-component manufacturer. It posted an excellent set of numbers for Q4 FY18, led by topline and operating performance. With marquee clients in its kitty, no client concentration, focus on research to develop technologically advanced products and turnaround at Minda Furukawa, the company beckons investor attention.

Earnings snapshot

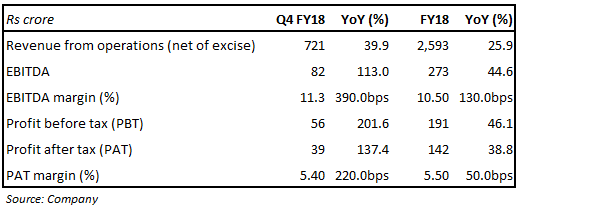

In the quarter gone by, net revenue from operations grew 40 percent year-on-year (YoY) on the back of growth accruing across major business segments. On the profitability front, the company posted a 390 bps YoY expansion in earnings before interest, tax, depreciation and amortisation (EBITDA) margin and 113 percent YoY growth in EBITDA. Margin expansion was driven by operating leverage, led by favourable product mix and reduction in employee and other operating costs. Profit-after-tax (PAT) grew 137.4 percent YoY with PAT margin expanding 220bps YoY.

On a full-year basis, the company posted a 25.9 percent increase in net revenue. EBITDA grew 44.6 percent, with margin expanded 130bps. PAT grew 38.8 percent.

We continue to maintain our positive view on the company due to:Diversified across segmentsMinda has a well-diversified product portfolio with a presence across a variety of segments in the automobile industry.

The group has about 30 customers in more than 20 countries. The management wants to capitalise on its global footprint and has many initiatives underway to increase its focus on exports. The company generated export revenue of Rs 275 crore in FY18 compared to Rs 170 crore YoY. The management maintains its FY20 export revenue target of Rs 500 crore.

Huge order bookFor Q4 FY18, Minda received Rs 1,361 crore in orders (lifetime value) across domestic and export businesses. Of which, Rs 564 crore relates to safety, security and restraint system and Rs 607 crore to driver information and telematics. For FY18, the company received an order worth Rs 4,221 crore (life-time value). These orders will be executed over the next four to six years.

R&D to drive next leg of growthThe company has been focusing and investing a lot on R&D. The management sees higher demand for electronics and advanced products. To develop technologically advanced products, it has established a technical centre - Spark Minda Technical Centre (SMIT) - in Pune.

Recently, Minda acquired EI Labs for an enterprise value of Rs 6.5 crore, underscoring its focus on R&D and electric vehicle (EV). In the second quarter, EI Labs bagged a prestigious order from Energy Efficiency Services (EESL) to supply mobility components for EVs.

Enough resources for acquisitionThe company recently raised Rs 310 crore through a qualified institutional placement (QIP). One of the issue objectives was to raise capital to fund its acquisition plans. The company may also use the amount raised to pare down some of its debt, manage its working capital and other general purposes.

Significant expansionThe management has significant expansion plans. It started a greenfield plant at Mexico in April last year to supply plastic interiors to the Volkswagen Group. It has also set up a third die casting plant in Pune, which will start generating revenues from this fiscal. Minda has an existing production capacity of 4,600 million tonne per annum and is targeting to raise the same to 9,600 mtpa by FY20.

The company is in the process of setting up a production line for new product ‘control cables’ at Pant Nagar and has already bagged its first order from a global two-wheeler manufacturer in India.

Turnaround in Minda Furukawa EBITDA positiveThe management has been focusing on turning around Minda Furukawa, which has been non-profitable. It has chalked out plans for the same. Its efforts are bearing fruit as the company has turned EBITDA positive in FY18. PAT, however, turned negative due to exceptional items.

Valuation

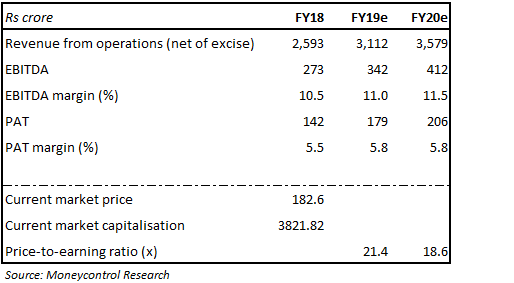

In terms of valuation, the company is trading at 21.4 and 18.6 times FY18 and FY19 projected earnings, respectively. After initiating coverage, the stock has run up around 32 percent in eight months. From a longer-term perspective, we are comfortable with the valuation and advise investors to accumulate the stock.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.