Highlights: - Growth slowdown in the euro area a key concern; European Central Bank hopeful of a rebound later - China: Stimulus programme and a possible trade deal can stabilise economy - Brexit remains a key watch on geopolitical risk - Central banks’ independence emerges as another key discourse - Emerging markets: Capital flows could sustain due to better economic momentum -------------------------------------------------

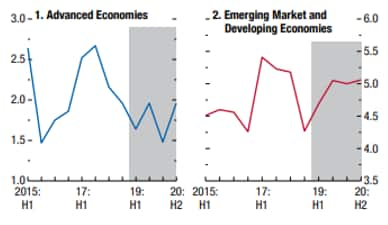

The recent spring meeting of the International Monetary Fund (IMF) and World Bank provided yet another occasion to assess the global economic strength and the risks to it. Earlier this month, IMF flagged off further deceleration in global growth compared to its assessment in January. It has projected a growth of 3.3 percent in 2019 – a downgrade of 20 basis points. However, its projection of 3.6 percent for 2020 remains intact, implying a rebound next year.

IMF global outlook

Growth concerns in the euro area and China Among the major downward revisions in its projections, IMF downgraded its growth outlook for the euro area to 1.3 percent in 2019 from 1.6 percent at the start of the calendar year. It expects growth to be weaker in several major European economies. In Germany and Italy, the growth downgrade has been much sharper. The export-oriented economy of Germany has not only been impacted by weak global demand, but tougher car emission standards have weighed on its automobile industry in recent times.

Given this context, the European Central Bank (ECB) kept its interest rate policy on status quo, marked by liquidity measures like new long-term loan programmes. However, it remains hopeful of a rebound in the economy later this year as some of the factors that have held back growth appear to be waning.

In the case of China, surprisingly, there has been a slight upward revision in IMF's projections, implying that growth could be stabilising here after the recent stimulus programmes.

Geopolitical risks – Brexit and trade tensions Brexit remains a key geopolitical risk. While officially the Brexit deadline has been postponed to October 31, UK Chancellor of the Exchequer Philip Hammond is hopeful that a Brexit deal should be struck between the government and Labour Party in weeks. Jeremy Corbyn (Leader of the Labour Party) has demanded keeping the common external tariff policy with the EU. It’s noteworthy that the volatility in the pound versus the dollar has significantly eased over the last few days.

Volatility in the pound  Source: Investing.com

Source: Investing.com

A deal announcement between the US and China with regard to their ongoing trade war may take some more time, but media reports suggest that a mutually accommodative stance seems to be in play. For instance, US negotiators have reportedly agreed to soften their demand asking China to curb industrial subsidies.

Central bank’s independence and board’s transition One of the key concerns that was discussed at the IMF meeting was with regard to the central bank’s independence. Over the years, there have been noise in this regard in some emerging markets. The Federal Reserve has also been under constant review by the market participants on whether it is able to tackle political pressures from the White House.

ECB President Mario Draghi took it a step further by saying he is “certainly worried about central bank independence, particularly, in the most important jurisdiction in the world." This is an obvious reference is to the Federal Reserve and comes at a time when Trump is making a case for his candidates -- Stephen Moore and Herman Cain -- to the board.

In the eurozone as well, this year marks an important transition for incumbents of the central bank. Three members of the ECB’s six-member executive board will complete their term, which includes Draghi and Chief Economist Peter Praet. This year, eight of the 19 Eurozone national central bank governors would also step down.

Silver linings How the key board transitions in the central banks play out remains to be seen. Nevertheless, the global focus remains on growth deceleration and the ways and means adopted by central banks to mitigate that.

So far, financial markets factor in a low possibility of recession in the near term. Hopes of a rebound next year is backed by a shift in the interest rate tightening policy by some central banks, recent stimulus in China and hope of an easing in geopolitical risks.

As per IMF, the waning of some temporary drags on growth in the euro area and a gradual stabilisation of conditions in stressed emerging market economies (including Argentina and Turkey) should aid the recovery. Better economic momentum expected for EMs (versus advanced economies) could lead to further acceleration in capital flows.

Follow @anubhavsaysFor more research articles, visit our Moneycontrol Research pageDisclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed hereDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.