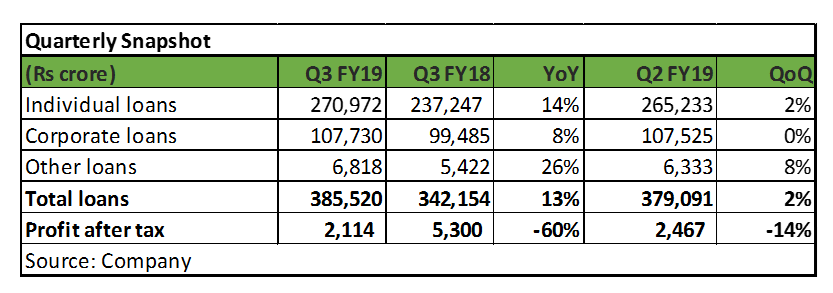

Housing Development Finance Corporation (HDFC), the largest housing finance company, reported net profit of Rs 2,114 crore in Q3 FY19 as compared to Rs 5300 crore in Q2 FY18 on the back of a healthy loan book growth and stable spreads.

The lender's performance in the current quarter is not comparable on a year-on-year (YoY) basis because in the same period last year (i.e Q2 FY18) the company had reported one –off gains of Rs 5,250 crore on listing its life insurance subsidiary.

Hence, after adjusting for exceptional items and one-time transactions (i.e. profit on sale of subsidiaries and consequent special additional provisions), the operating profit before provisions would have been Rs 2,984 crore for Q3 FY19 compared to Rs 2,352 crore in the previous year, representing a growth of 27 percent.

Loan growth and margin are the two key monitorables for HDFC. While the overall loan book growth slowed slightly, we aren’t too disappointed as it came on a very high base. More importantly, mortgage book growth after adding back loans sold was strong and faster than the industry. This is commendable as the housing finance space is going through turbulent times.

On the margin front, spreads continue to remain in a narrow range of 2.2-2.35 percent irrespective of the interest rate cycle.

Total lending book of HDFC stood at Rs 3,85,520 crore as of December-end, up 13 percent YoY. Growth in the total loan book after adding back loans sold in preceding 12 months was 19 percent YoY.

Individual loan book grew 14 percent YoY (24 percent after adding loans sold) and constitutes 70 percent of the total book. Non–individual book increased 9 percent.

Spreads in the overall book remained almost stable at 2.26 percent (individual book: 1.89 percent and non-individual book: 3.08 percent).

With gross non-performing loans at 1.22 percent, asset quality continues to be pristine. Non-performing loans in the individual portfolio stood at 0.68 percent while that of the non-individual portfolio increased to 2.46 percent in Q3 as compared to 2.18 percent in previous quarter.

The management's thrust on affordable housing segment continued as there was a strong traction in loans sanctioned to economically weaker section (EWS) and lower income group (LIG) segments.

We see HDFC benefiting of the liquidity shift towards strong and top quality names which will help it to continue to gain market share.

While the core mortgage business is on a stable growth trajectory, the financial conglomerate also stands to gain from equally strong performance of its subsidiaries.

For more research articles, visit our Moneycontrol Research page

(Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here)Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.