Highlights: - Subdued demand pushed tractor segment margin to a seven-quarter low - Construction equipment segment posted significant margin expansion - Business outlook for the tractor segment is weak in the short term, positive for the long term - Construction equipment and railway segments continue to perform well - Reasonable valuations; accumulate for the long term

--------------------------------------------------

Escorts, the fourth-largest tractor player in India, reported a weak set of earnings for Q4 FY19, bogged down by multiple macroeconomic challenges that the industry is facing. The weak performance was due to subdued demand and higher operating expenses.

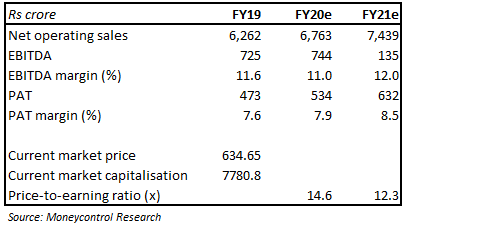

Its strong position in the domestic market, new product launches, focus on exports and reasonable valuation (14.6 times FY20 projected price-to-earnings) make it a long-term buy.

Result snapshot  Segment-wise break-up

Segment-wise break-up

Key highlights In the January-March quarter, revenue grew 14 percent year-on-year (YoY), led by 12.5 percent growth in tractor sales, which contributes 75 percent to total sales. The segmental show came on the back of a 6.7 percent growth in tractors and 5.5 percent growth in realisations, steered by a price hike taken by the company.

Escorts posted a 10.2 percent growth in construction equipment (CE) revenue, fuelled by traction in material handling equipment, backhoe loaders and compactors. Railway segment revenue grew 36.2 percent YoY.

In terms of operating profitability, tractor segment’s profit before interest and tax (PBIT) margin contracted sharply (200 bps YoY) and hit a seven-quarter low due to adverse product mix and higher operating expenses. CE, on the other hand, saw 198 bps PBIT margin expansion led by price hike and a favourable product mix.

The railways segment saw PBIT margin slide of 85 bps due to higher contribution of imported products.

Outlook

Industry opportunities – sluggish in the near term Multiple macroeconomic challenges, including the tentative outlook on monsoon, are expected to have a negative impact on the tractor industry in the near term and could lead to subdued consumer sentiment. In light of this, the management has guided at an industry growth of 5-8 percent in FY20. The management expects Q1 FY20 to be dismal and predicts a demand pick-up before the next harvesting season.

In the long term, Indian farm equipment and tractors are poised to grow on the strength of government’s focus on rural areas, increasing usage of tractors to improve productivity, farm loan waivers and rising rural income.

Escorts, which has a strong position in the market and has been expanding its share supported by network expansion and innovative products, would be able to beat industry growth.

Construction equipment and railways have started to add value Strong demand for material handling equipment, backhoe loaders and compactors, coupled with cost optimisation and improvement in product mix, have led the CE business to improve margin. Strong demand and operating leverage are expected to benefit the CE business going forward.

Railway segment is also expected to do well on the back of new product launches and improvement in demand.

Valuation at reasonable levels Valuation is at a reasonable level, with the stock trading at 14.6 times FY20 and 12.3 times FY21 estimated P/E. We advise investors to accumulate the stock for the long term.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.