Highlights

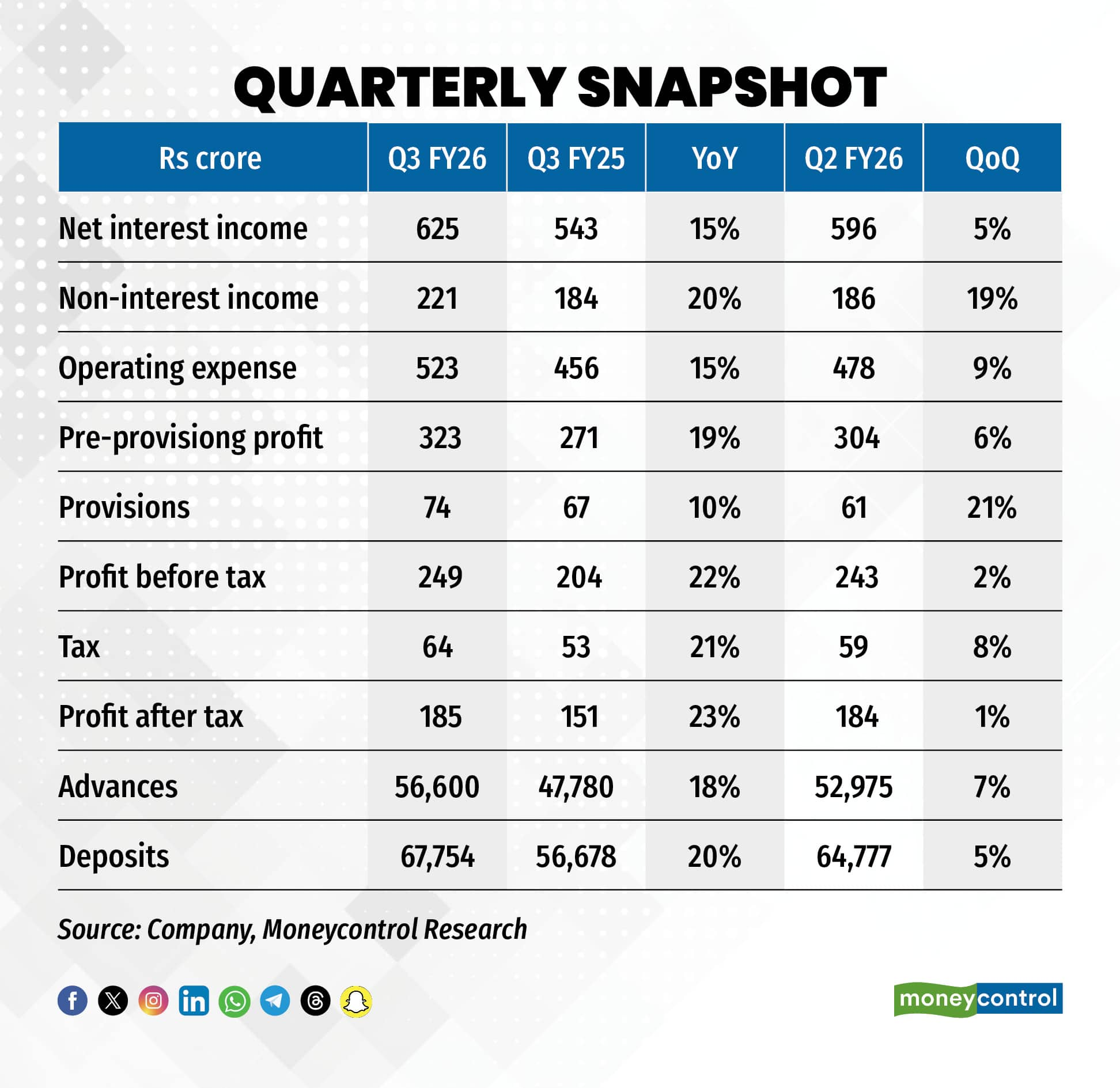

DCB Bank (CMP: Rs 198; Market cap: Rs 6,379 crore; Rating: Overweight) reported its highest-ever quarterly profit of Rs 185 crore in Q3 FY26, marking an increase of 23 percent YoY (year-on-year) despite one-off expense related to new labour code. The bank’s performance was broad-based, driven by healthy loan growth, robust fee income, better margins, improvement in operating efficiency, stronger asset quality, and contained credit costs.

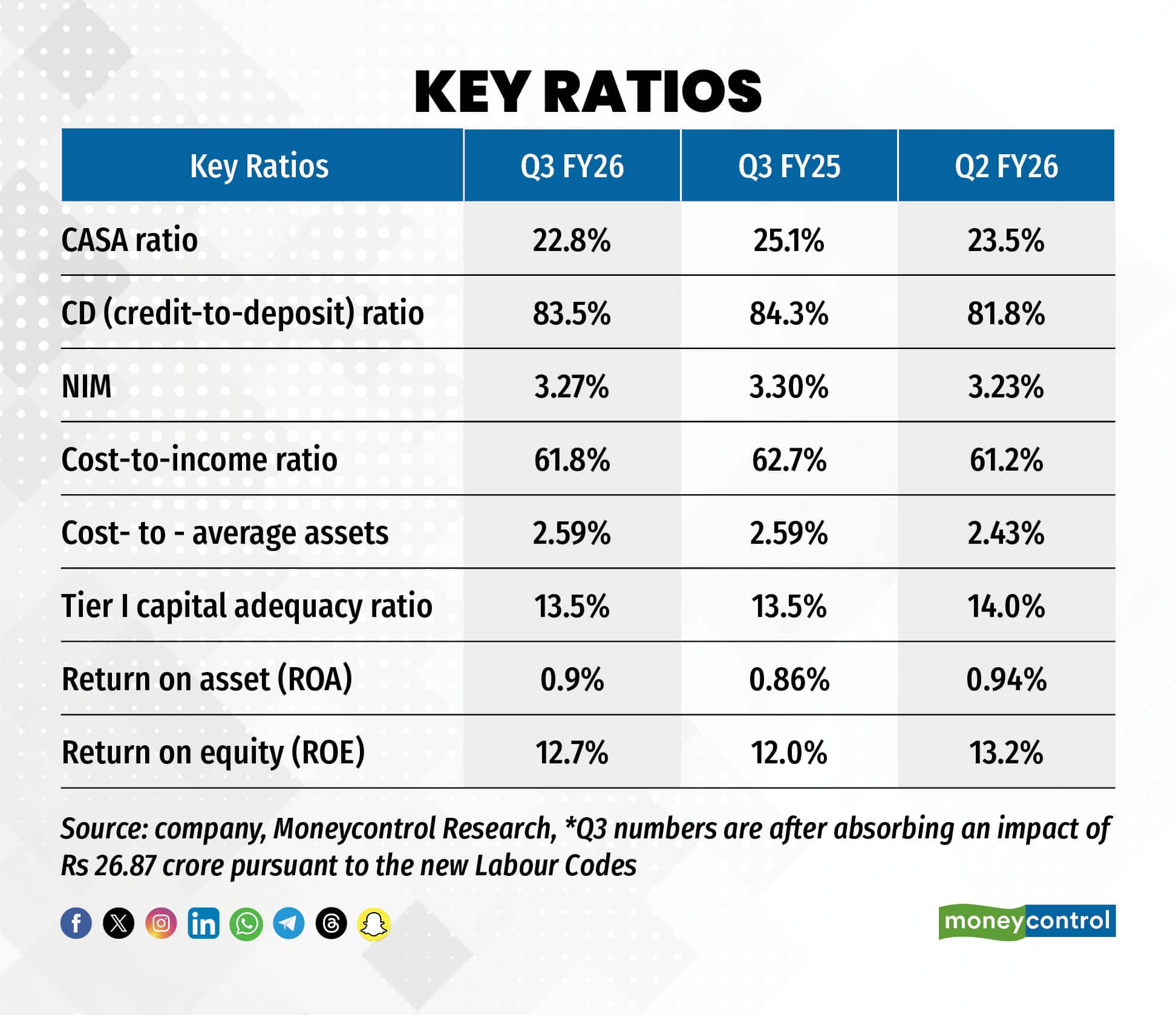

More encouragingly, the management expects margin expansion to continue through Q2 FY27, assuming no further rate cuts by the RBI. It has guided for a ROE (return on equity) of 13.5 percent in FY26 and 14.5 percent in FY27 — levels the bank has already effectively achieved in Q3 FY26.

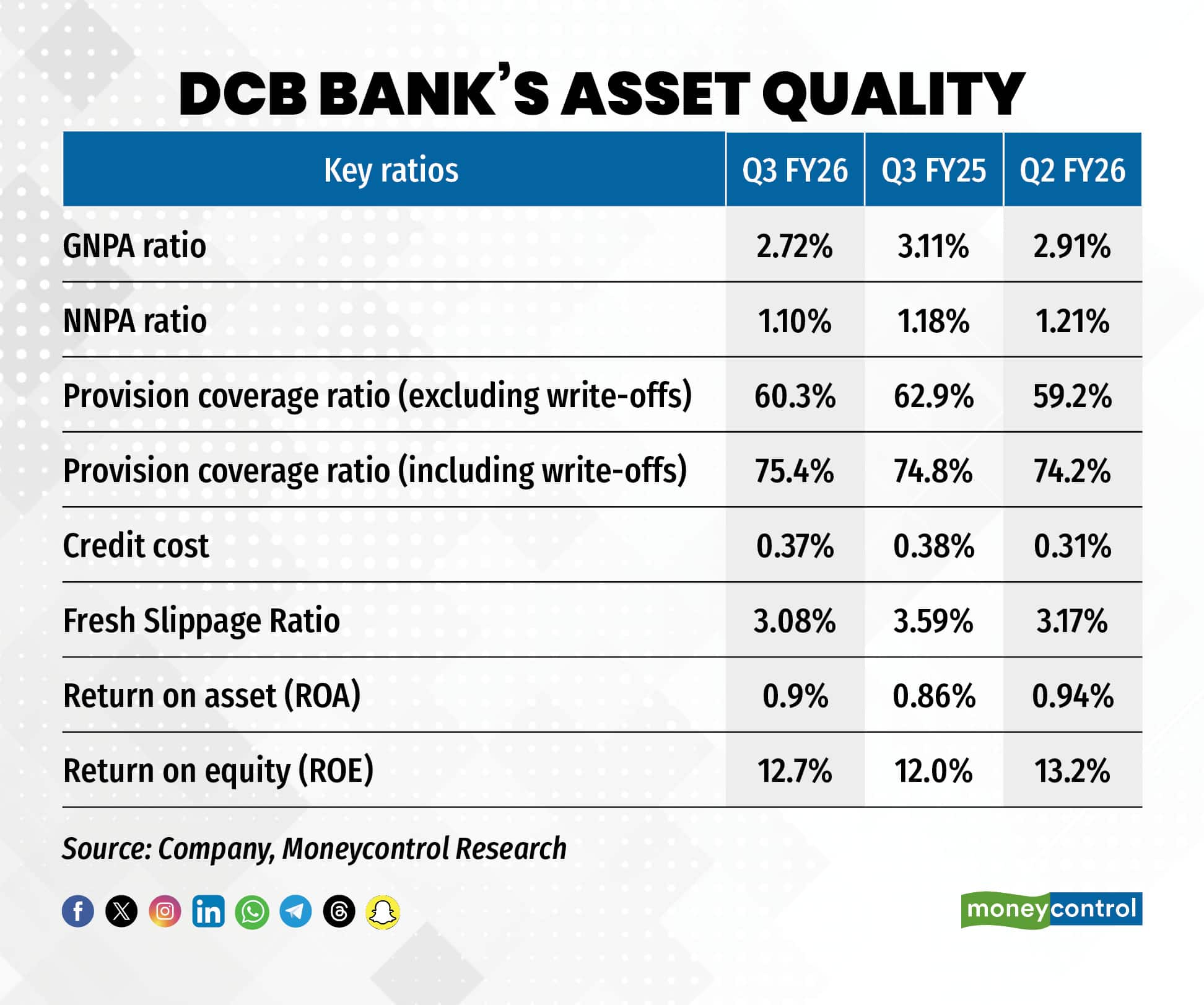

The reported ROA (return on asset) and the ROE for the quarter stood at 0.91 percent and 12.73 percent, respectively. However, excluding the one-off impact of the new labour code, the ROA would have been 1.01 percent and the ROE a healthy 14.1 percent in Q3 FY26, underscoring the underlying strength of profitability.

DCB Bank’s stock has outperformed the sector benchmark (Bank Nifty) and overall market (Nifty) surging 46 percent and 70 percent in the past 6 months and 1 year respectively. The key question now is whether this rally can sustain.

The most compelling aspect of DCB Bank is its valuation. Even after a sharp rally, the stock trades at only 0.9x its estimated FY27 book value, making it attractive. While a valuation re-rating hinges on the bank’s ability to sustain consistent performance, several profitability levers are in place that could drive further upside.

Healthy business growth, robust fee income

DCB Bank has maintained steady growth, with net advances rising to Rs 56,600 crore as of December 2025, reflecting a 18 percent YoY increase. DCB Bank aims to double its balance sheet over the next 3-3.5 years, targeting an annual loan growth of 18-22 percent.

Mortgages constitute around 50 percent of the loan book as of September end.

DCB’s deposits grew by 20 percent YoY till end December’25, higher than the banking system deposit growth, albeit on a smaller base. DCB’s CASA deposits ratio of 23 percent remains much lower compared to the banking system average.

That said, it is reassuring to see the bank strengthening the granularity of its deposit base. Deposits from the top 20 depositors have come down to 6.61 percent of total deposits as of December 2025, compared to 15 percent in FY18, which adds stability to its funding profile.

DCB Bank’s core fee income grew a strong 29 percent YoY, driven by robust traction in third-party distribution, trade finance, and processing fees. The management expects this momentum to sustain in Q4, which is seasonally strong for fee income. Over the medium term, the bank is confident of sustaining fee income at around 1 percent of average assets, broadly in line with the 1.1 percent achieved in Q3 FY26.

Margin expansion to continue

DCB’s net interest margin (NIM) came in at 3.27 percent in Q3 FY26, up 2 basis points YoY from the previous quarter (Q2 FY26). The management has guided to a gradual margin expansion from here onward till Q2 FY27, assuming the RBI doesn’t implement further rate cuts. The improvement is expected to play out over the next 3-4 quarters as the bank’s long-tenure fixed deposits will mature and get repriced at lower rates.

In addition to lower funding costs, improved yields are expected to drive margin expansion. Over the past five years, DCB Bank has steadily built its home loan portfolio, which now accounts for nearly half of its mortgage book. Going forward, the bank aims to raise the share of business loans (LAP), which generate higher yields than home loans, while keeping the lower-margin co-lending portfolio capped at 15 percent of total advances.

The bank had borrowings of more than Rs 8,000 crore as of March’25, which has declined to less than Rs 5,000 crore as the bank replaced it with relatively lower cost deposits.

Together, the decline in funding costs and a more profitable product mix should support margin expansion.

Operating efficiency improves

DCB Bank effectively controlled its operating expenses aided by a reduction in employee base. Despite the one-off expense of Rs 27 crore in Q3 FY26, the cost-to-average assets ratio remained stable at 2.59 percent in Q3 FY26. Looking forward, the bank expects to benefit from the operating leverage as the balance sheet grows further. The management anticipates the cost-to-average-assets ratio to remain steady in the range of 2.5-2.6 percent and targets a cost-to-income ratio of 60 percent or below in the near term.

Asset quality strengthens

DCB Bank’s asset quality improved meaningfully in Q3 FY26, with a decline in both gross and net NPAs. More importantly, slippages fell to an 18-quarter low, signalling better asset quality trends. As a result, credit costs remained contained at just 37 bps—well below management’s guided 45 bps—even after accounting for floating provisions.

The restructured book eased slightly but remains elevated at Rs 811 crore (1.4 percent of advances) as of December 2025 and needs to be monitored closely.

View and Valuation

Overall, DCB bank is poised for a healthy loan growth, margin expansion (assuming no further rate cut), stable cost-to-assets ratio, and a very low credit cost in near to medium term. This guidance is very encouraging and should drive healthy earnings growth in FY27

Despite the sharp rally post earnings, DCB Bank is trading at just 1 time FY27 estimated book value. The valuation can move above 1x forward BV on sectoral tailwinds which along with healthy earnings growth will drive a meaningful stock upside in the near to medium term. Long-term investors should buy the stock.

Follow @nehadave01. For more research articles, visit our Moneycontrol Research page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.