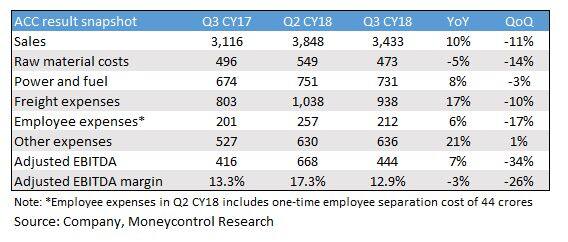

ACC, India's second-largest cement company promoted by global cement giant Lafarge Holcim, reported a stable set of earnings in the third quarter of 2018 on the back of healthy volume growth. The company reported a healthy topline, but operational performance came in slightly weaker as the industry continues to face challenging times on the cost front.

Result snapshot The company reported a 10 percent year-on-year (YoY) growth in revenue to Rs 3,433 crore, driven by an improvement in volume as well as realisations. Earnings before interest, tax, depreciation and amortisation (EBITDA) for the quarter gone by stood at Rs 444 crore compared to Rs 416 crore over the same period last year. EBITDA margin contracted about 40 bps as cement companies are facing input cost pressures.

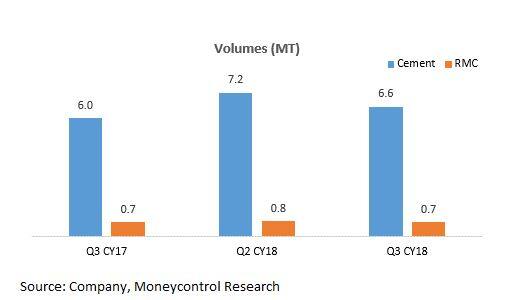

Volume growth continues Strong demand across regions, especially central and eastern markets, drove up cement volumes. The company reported a 10 percent increase in cement volume to 6.6 million tonne (MT), while ready mix concrete (RMC) volumes came in 12 percent higher YoY.

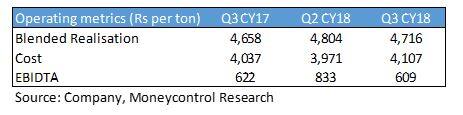

Realisations remained largely stable on a sequential basis despite a weak monsoon season. The company has a pan India presence and benefitted from premiumisation as well as higher realisations in the central region. This was, however, offset by moderate price weakness in other regions.

EBITDA per tonne declined on a sequential basis as a slight dip in realisations along with moderate increase in cost pressures (mainly petcoke and diesel) resulted in declining profitability. Cost per tonne increased by just 3 percent as the company continues to focus on operational efficiencies to mitigate challenges on the cost front.

Outlook Growth outlook for the sector as well as the company appears positive as demand from infrastructure segment continues to gather momentum. Despite the increasing cost pressures, the company continues to perform well on an operational basis and is constantly working on increasing cost discipline through route optimisation and other measures. The company stands to benefit from additional synergies from the signing of Master Supply Agreement (MSA) with Ambuja Cement.

ACC has strong fundamentals and a cash-rich balance sheet. The stock price has seen an increase by nearly 15 percent since the lows witnessed during June-July. From a valuation standpoint, the stock now trades at around 11 times FY19 EV/EBITDA and appears little stretched from a near term perspective. Amid increased market volatility, long term investors can look to accumulating this stock on every dip.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.