The market mood has been sombre from last Diwali 2018, thanks to economic slowdown, subdued earnings, liquidity crisis, asset quality concerns, FII outflow, corporate governance issues (in a few cases) global growth fears amid endless US-China trade tensions etc, which clearly reflected in broader markets. Diwali 2019 is still two-week away.

The Nifty Midcap and Smallcap indices fell 11 percent and 14 percent respectively in Diwali 2019 (against 7 percent and 22 percent correction in Diwali 2018), but the picture was completely different in benchmark indices.

The Nifty50 and Sensex rallied 6 percent each (against 4.5 percent and 10 percent gains respectively in Diwali 2018) led by hope rally and buying in select bluechips.

Banking & financials and IT remained in forefront again in terms of gains (up 9 percent, 17 percent and 3 percent respectively) whereas the weakness continued in other sectors like auto, metals and pharma which showed double digit fall.

The July-September earnings are expected to continue to show the muted picture for another quarter. But, after several measures taken by the government along with RBI to revive economy and sentiment, the street looks hopeful of recovery in the second half of FY20 and strong growth in FY21, experts feel.

"We may see market sentiments turning buoyant in the second half of this fiscal if there will be an uptick in demand during the festive season, bolstered by the recent measures taken by the government to revive the economy. Further, the impact of corporate tax is likely to start reflecting on the corporate earnings from Q2FY20 onwards," Ajit Mishra, VP Research at Religare Broking, told Moneycontrol.

This is the period when the impact of transmission of low interest/borrowing cost (resulting out of 5 consecutive rate cuts by RBI) will be clearly visible at the end consumers' level, in terms of demand pick up, he said.

Generally, the effect of measures is always seen with a lag, hence considering the slowdown and its impact, the market seems to have priced in and may be gradually preparing for next upmove especially after government move, according to experts.

“We believe the market has already discounted and priced in the economic downturn, and we are at the end of the cyclical downturn trajectory. Tax benefits for newcomers will also attract new entrepreneurs and this may help the small and mid-cap sector to pick up the expected growth," Gaurav Garg, the head of research at CapitalVia Global Research Limited - Investment Advisor, said.

Vineeta Sharma, Head of Research - Narnolia Financial Advisors, also said though near term macro challenges persist, various initiatives by the government along with natural demand recovery post 12-18 months of the downturn will bring better days. The new tax regime now empowers companies to strategize further growth with better working capital, she added.

Hence, experts feel the period between Diwali 2019 and Diwali 2020 could be an exciting phase for the markets, expecting the market to return 15-25 percent and mid-smallcaps to outperform largecaps if demand improves in current festive season.

"Best case estimate is 14,000 on Nifty50 till Diwali 2020. We believe midcap and smallcap will outperform the largecap stocks," Garg said.

Sharma, who expects normalization of corporate earnings growth over the next four-six quarters, said the target for March 2020 was 12,300 on Nifty. She believes, from Diwali 2019 to Diwali 2020, there is a good chance of market delivering 15 percent upside.

Hence, as experts feel all these concerns mentioned above in few fundamentally sound smallcap and midcap stocks are overdone, there is an opportunity to pick not only largecap but also in mid-smallcap quality stocks.

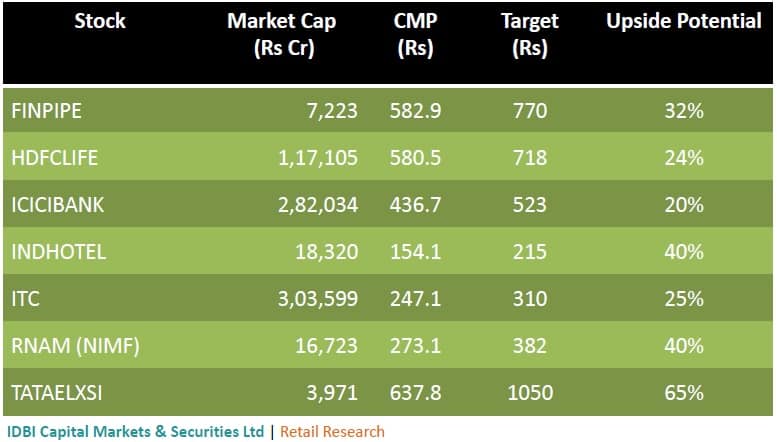

Here is the list of 13 stocks which could give 13-65 percent return by next Diwali:Brokerage: IDBI Capital Markets

Finolex is an undisputed market leader in agriculture pipes segment (70 percent of PVC pipes by volumes) with a very strong brand recall among farmers for its product despite low margins as compare to PVC/CPVC.

The company is transforming its business model from B2B to B2C as it increases internal consumption of its PVC resin for its pipes & fittings division. The mix value added products to push up margins in pipe segment to low double digits.

HDFC Life InsuranceHDFC Standard Life insurance has a strong parentage and a very reputed brand name which enables it to attract and gain new business from potential customers.

Recent strategies largely focus on growing Protection portfolio (which includes term and annuity business) as it is margin accretive which resulted in increase in improvement its over-all New Business Margins from 19.9 percent in FY16 to 24.6 percent in FY19. It has large protection opportunity in India.

ICICI BankThe new management team under the leadership of Mr. Sandeep Bakhshi is set to deliver on key priorities with sharp focus on core operating profit growth and improvement in asset quality.

Incremental NPA is moderating with slippages trending lower in the last four-five quarters. The below investment grade book stands currently at 2.6 percent of loans versus 4.8 percent in Q1FY19. It has sufficient provision coverage on NCLT accounts and is likely to see meaningful recovery through resolutions in the coming quarters.

Indian HotelsIHCL plans to add 15 new hotels every year, mostly through management contract route. It has signed 22 new contracts in FY19 and 7 in Q1FY20. We believe, with 65 percent industry occupancy, there are early signs of revival in hospitality industry, which will drive ARR growth. We believe IHCL would be a key beneficiary, considering its strong positioning in the domestic market and well planned expansion plan.

ITCWe believe ITC is now well poised to take moderate price hike and consequently support acceleration in EBIT. FMCG – other business has now gained scale and is competitive across many categories.

ITC is currently trading at 45-50 percent discount relative to broader India consumer universe.

Reliance Nippon Life Asset ManagementWith focus on retail which has relatively higher degree of reliability compared to institutional flows, share of total individual AUM has increased from 41.5 percent FY16 to 55.4 percent as of FY19.

Of all the financial savings products, mutual funds are the most under-penetrated in India with an AUM/GDP of around 12 percent, against a global average of around 55 percent. Hence, under penetration provides opportunity to grow.

Tata ElxsiTata Elxsi has developed good presence in the media & communication space. FTH and 5G has opened up new opportunities for service providers like Tata Elxsi across both communications and media space.

OTT Platforms (over the Top), another space within media sector which has gained traction globally, is another growth avenue for Tata Elxsi. The company already has both domestic and global OTT players as its clients.

Tata Elxsi has seen management change with Mr. Madhukar Dev, MD & CEO having retired and succeeded by Mr. Manoj Raghavan. At current market price, Tata Elxsi is trading at a PER of 16x/13.8x on FY20/FY21E which provides good risk reward. Thus we believe that the stock has strong re-rating potential as the growth improves in H2FY20/FY21. It also has a cash surplus of around Rs 500 crore.

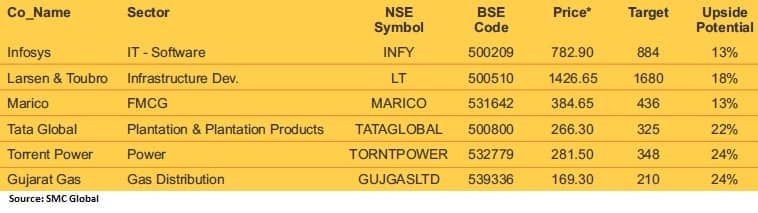

Brokerage: SMC Global

The management of the company remains reasonably optimistic about growth prospects due to increase in win rate and increase in large deal pipeline. These deals will help incentivize its multi-gate servicing capabilities through digital platforms and enhance presence in Europe. Growth in retail is driven by large deal wins, and differentiation on digital deals.

Strong order wins coupled with healthy order pipeline would give on visibility of revenue growth momentum. Thus it is expected that the stock will see a price target of Rs 884 in 8-10 months time frame on an expected PE multiple of 23 times and FY20E EPS of Rs 38.45.

Larsen & ToubroThe Company looks forward to a period of increased investment momentum and continued growth. Initiatives towards improved productivity, cost efficiencies derived from leveraging digital technology, capacity utilization and capability enhancement are expected to help the company maximize its shareholder returns (RoE) on a sustainable basis.

Thus, it is expected that the stock will see a price target of Rs 1,680 in 8-10 months time frame on an one year average PE multiple of 22.65 times and FY20E EPS of Rs 74.17.

MaricoThe company will continue to drive sustained profitable volume-led growth over the medium term, through its focus on strengthening the franchise in the core categories and driving the new engines of growth towards gaining critical mass. Over the medium term, the company retains the target of 8-10 percent volume growth and healthy market share gains in the India business.

Thus, it is expected that the stock will see a price target of Rs 436 in 8-10 months time frame on 2 year average PE multiple of 49.54 times and FY20E EPS of Rs 8.81.

Tata Global BeveragesThe management of the company has clearly highlighted its intention to be a broader FMCG company in India. With recently announced merger with Tata Chemicals, acquisition of branded tea business of Dhunseri tea and the JV between the PepsiCo India, it is all set to scale up its network and business to capture opportunities in long term.

Thus, it is expected that the stock will see a price target of Rs 325 in 8 to 10 months time frame on a current P/Ex of 38.65 times FY20E EPS of 8.41.

Torrent PowerThe company is reducing its debt equity ratio with a focus on improvement of efficiency. Moreover, improvement in T&D, focus on green power project and commissioning of renewable power plants would give good strength to the company. Government’s policy push like emphasis on clean coal technologies, replacing old plants with new super critical plants, policy on automatic transfer of coal linkage, stricter environmental norms and emphasis on digitalization will go a long way in reenergizing the coal based power generation sector.

Thus, it is expected that the stock will see a price target of Rs 348 in 8 to 10 months time frame on 3 year average P/E of 15.66x and FY20EPS of Rs 22.20.

Gujarat GasThe company has steady revenue growth momentum and sustainable margins. It shall continue to focus on growing the penetration in the current operating areas by increasing the PNG connections and additional CNG stations while tapping the untapped potential by expeditious rollout of distribution network in the newly acquired geographic areas as well. With this focused endeavour GGL shall continue its efforts in providing clean fuel solutions across all operational area to augment an energetic top-line and bottom-line in coming years.

Thus, it is expected that the stock will see a price target of Rs 210 in 8-10 months time frame on an one year average PBV multiple of 5.14times and FY20E BVPS of Rs 40.90.

Disclaimer: The views and investment tips expressed by investment expert on moneycontrol.com are his own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.