Dear Reader,

During the holiday-shortened trading week, Indian equity indices traded within a narrow range, with broader market segments outperforming their benchmarks. The Nifty50 edged up 0.29 percent, while the smallcap index gained a full percentage point and the midcap index advanced 0.3 percent.

Sectoral performance showed notable divergence. Defence stocks led the rally with gains exceeding 3 percent, followed by metal stocks, which climbed 2.7 percent, and media stocks, which added 1 percent. On the losing side, PSU Bank stocks shed nearly 1 percent, while both IT and pharmaceutical stocks declined 0.3 percent each.

Foreign institutional investors maintained their selling pressure throughout the truncated final week of 2025, offloading Indian equities worth Rs 4,290.96 crore. Trading volumes, which typically thin out as the year draws to a close, remained predictably subdued. Hopes for a traditional year-end or "Santa Claus" rally dissipated as FII selling persisted amid limited visibility on progress in US-India trade negotiations.

There were some positive developments, however. The Reserve Bank of India's liquidity interventions—executed through open market operations and a USD/INR buy-sell swap—helped stabilise the rupee, though persistent FII outflows continued to dampen market sentiment.

The US markets advanced during the shortened trading week, with both the S&P 500 Index and Dow Jones Industrial Average reaching record highs. The week's standout performers were gold and silver, which surged higher and continued their impressive year-to-date rally.

Economic data painted a robust picture of US growth. According to preliminary figures released by the Bureau of Economic Analysis on Tuesday, the US economy expanded at its fastest pace in two years during the third quarter. GDP grew at an annual rate of 4.3 percent in the three months through September, accelerating from the second quarter's 3.8 percent growth and comfortably exceeding market estimates of around 3 percent.

Despite GDP surpassing consensus forecasts, market scepticism remained evident, as other indicators—particularly consumption and employment data—failed to corroborate the strong headline number. Adding to concerns, the US Consumer Confidence Index declined for the fifth consecutive month in December, falling to 89.1 from November's upwardly revised reading of 92.9 and missing expectations of 91.5.

Looking ahead, the final week of 2025 is expected to remain subdued as investors prepare for the upcoming earnings season amid characteristically low trading volumes. As we transition into 2026, market direction will be shaped by three key factors: currency volatility, foreign institutional investor flows, and developments in India-US trade discussions.

Nifty at a Crossroads

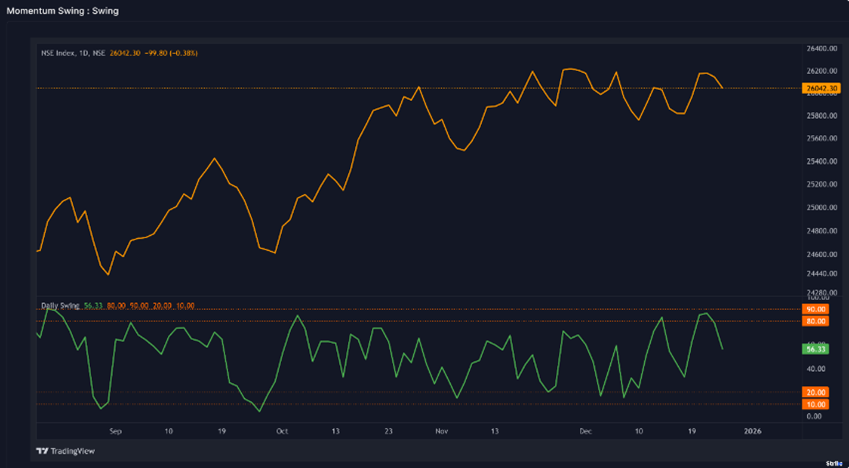

Nifty ended the week on a marginally positive note, yet daily sentiment indicators suggest the short term has entered overbought territory. This leaves us watching critical levels as the new week begins: Will Nifty hold above 23,800, or will it break lower? Is this a market gradually losing strength, or have we seen the worst?

The Banking sector registered its third consecutive weekly decline. Both indices are forming a series of doji candles—a telltale sign of indecisive weeks as the market awaits a clear directional signal.

The daily swing, a short-term momentum indicator, tells an instructive story. Recent readings above 80 have consistently triggered market pullbacks, and this week proved no exception. While a deviation from this pattern is anticipated, it hasn't materialised yet. Now the focus shifts to waiting for the swing to turn upward and for Nifty to establish a higher bottom above 23,726.

Source: web.strike.money

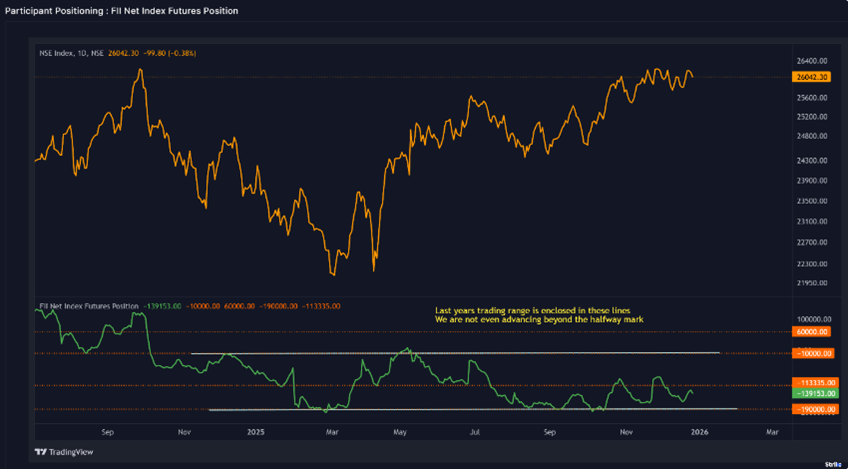

FIIs have shown little appetite for covering their short positions. It's been over a year since they held a net long position in index futures. Throughout this period, their net position has oscillated between -190,000 and -10,000 contracts, with only brief and ultimately false breakouts beyond these boundaries. More recently, they haven't even managed to breach -113,335 contracts.

In recent days, there were signs they might cover more shorts as an upward trend began emerging in their positions. However, Friday's session halted that momentum. This persistent bearish positioning has prevented the market from falling sharply, yet it has also failed to generate sufficient positive momentum for a sustained multi-week rally.

Source: web.strike.money

The Open Interest Put/Call ratio has remained range-bound for over a year. Readings near 0.95 have consistently marked market tops, with the most recent occurrence last month. Conversely, readings near 0.77 have signalled bottoms, and the market did indeed advance from those levels.

What's notable now is that the indicator hasn't returned to the overbought zone. Could this suggest more upside remains ahead? One can hope.

Source: web.strike.money

Sector Rotation

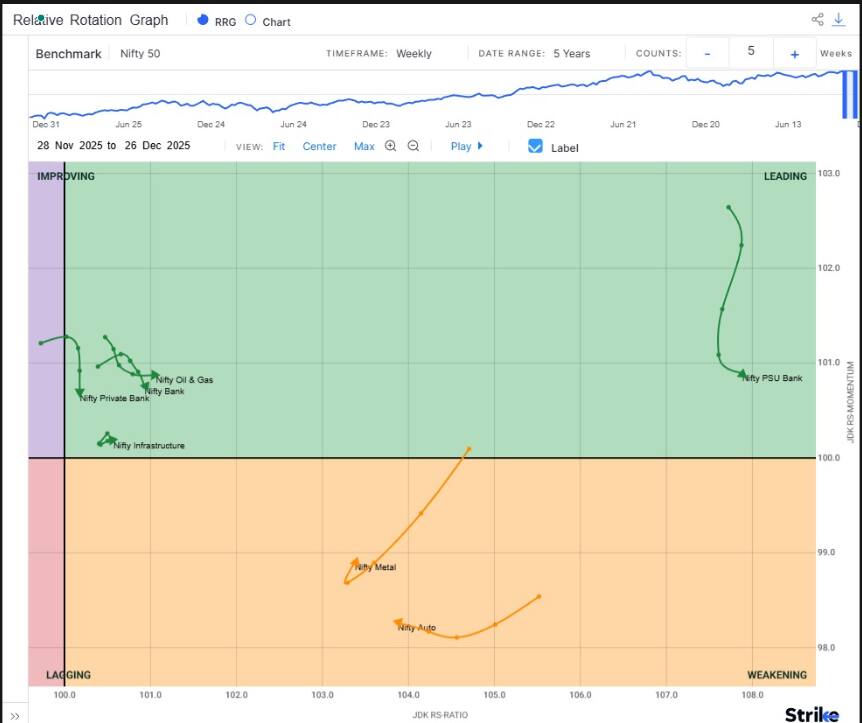

Nifty 50 – The Benchmark Index ended higher by +0.29% this week and closed at 26042.30.

Weekly RRG:

Leading Quadrant:

Nifty Private Bank has seen a decline in momentum, but its relative strength remains unchanged this week. The Nifty Oil & Gas index’s momentum has flattened out this week, but it has seen significant improvement in relative strength. Nifty Infrastructure continued to show improvement in both momentum and relative strength this week. The Nifty PSU Bank continues to see a dip in momentum, but there is some improvement visible in the relative strength this week.

Weakening Quadrant:

Nifty Metal has seen a meaningful uptick in both momentum and relative strength this week. If this trend continues, Nifty Metal can see a significant outperformance against the benchmark index in the coming weeks. Nifty Auto continues to see improvement in momentum, but the relative strength continues to weaken

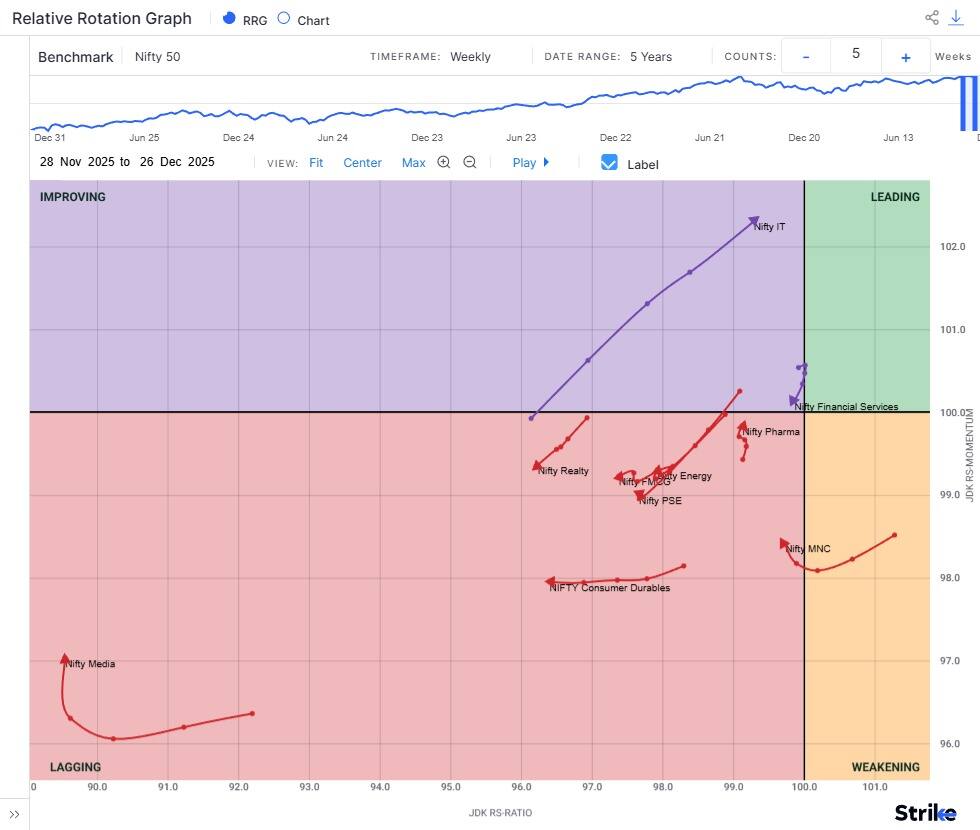

Improving Quadrant:

Nifty IT continues to see sharp improvement in momentum and relative strength. On the other hand, Nifty Financial Services is witnessing a decline in both momentum and relative strength.

Lagging Quadrant:

The improvement in momentum couldn’t last long for the Nifty FMCG, and this week it has seen a decline in both momentum and relative strength. The Nifty Consumer Durable index continues to show a sharp decline in relative strength. Nifty Realty index continues to show declining momentum and relative weakness. Nifty Energy, Nifty PSE, and Nifty Pharma have seen improvements in both momentum and relative strength. The Nifty MNC index also saw some improvement in momentum, but the relative strength continues to decline. Nifty Media has seen a sharp improvement in momentum in the past couple of weeks. However, improvement in relative strength is not visible yet.

Stocks to watch

Among the stocks expected to perform better during the week are Titan, Eicher Motors, MCX, Laurus Labs, Maruti, National Aluminium, NMDC, IDFC First Bank, Hindalco, Phoenix Ltd, Vedl, IIFL and Ashok Leyland.

Cheers,

Shishir Asthana

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.