It was blockbuster expiry, followed by a blockbuster week close for Indian equities. This momentum could lead us to end the month at the highest price point of recent times.

Nifty had quite a joy ride. The expiry started with a downward spiral towards the consensus floor around 11,000. After a couple of gyrations, this final week of expiry began around the upper end of the range.

Against the usual expectation from a range-bound set-up though, Nifty kept the momentum up. So much so that all the sessions of the week the index posted gains.

Tiny but consistent gains pushed Nifty 2.43 percent higher than a week before. Also, we ended the expiry of the August series contracts. For the August series, too, Nifty added around 4 percent price increment.

Bank Nifty, on the other hand, had a rather topsy-turvy ride this expiry. The bank index moved around within a range of 1,000 points for most of the weeks in the expiry.

However, the week of expiry brought goodies for the bank index as well. The back to back rising sessions this week on top of a nervous start to the August expiry helped Bank Nifty add around 9 percent increment in the price for the August series.

However, it was stellar last session of the week with a mammoth 4 percent increment in price Bank Nifty posted almost 10 percent rise for this week alone.

On the open interest front for Nifty, the story still remains the same. Expiry of August series contracts brought some bit of reduction in OI.

But with average rollovers of around 77 percent, Nifty futures did manage to add over 8 percent in OI for the August series. Also, the week ended with around 4 percent additional increment in the index futures OI.

Bank Nifty futures on the other hand, unlike Nifty, did go through few cycles of Short- Short Covering this expiry.

As a result of that, the OI tally for Bank Nifty futures despite the average rollovers remain contracted for the August series.

Bank Nifty lost around 3 percent in OI for August expiry but it did manage to attract 18 percent of long interest additions in futures on the last session of the week.

Aggregate stock futures OI also rose by around 6 percent in August expiry. However, the highest tally of stocks still lost OI with a rise in price.

This does not include just the short-covering stocks but also includes some of the performing stocks where the conviction to carry forward longs lacked.

Slicing the stock futures data further, many sectors this expiry had sector aggregate post short covering with a rise in price yet fall in OI.

Maruti, Tata Motors and Ashok Leyland led short covering in the auto sector. Banking, both PSU and private, still had traces of longs in many stocks hence the sectors added on an aggregate basis OI with a rise in price.

Coming down to sentiments, Nifty OIPCR remains tightly wound around 1.64. Little on the optimistic side but healthy. On the risk front, India VIX though is a tad bit too comfortable and looks extreme especially after a drop of over a point this week.

Finally, Aggregate stock futures OI lacked the backing of fresh built-up in the recent rise. Sentimental indicators like India VIX and OIPCR are at the over-optimistic end. The previous hurdle of 11,500 could arrest immediate pull back but if it gets taken out, we may see deeper cut.

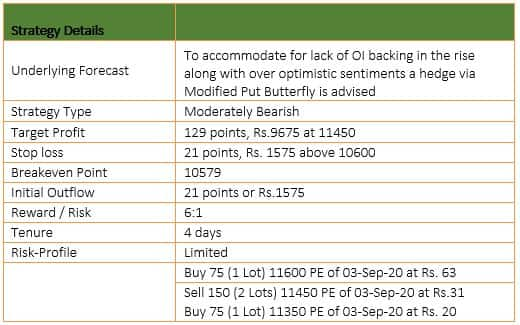

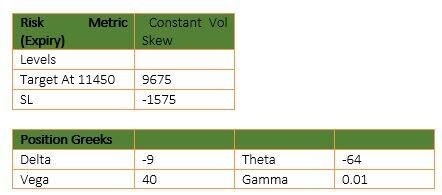

To accommodate for lack of OI backing in the rise along with over-optimistic sentiments a hedge via Modified Put Butterfly is advised.

Modified Put Butterfly is a 4-legged strategy where 1 lot of Put close to current underlying level is bought against that 2 lots of lower strike Puts are sold and 1 more lot of Put is bought but closer to the Put sold strike.

This keeps the lower but constant profits in case of a downward breakout. This is a fair risk-averse and a universal strategy.

(The author is CEO & Head of Research at Quantsapp)Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.