The market caught in a bear trap and plunged 2.5 percent in the last week ended January 23, pressured by renewed global trade tensions, geopolitical dynamics, persistent FII outflow, and uneven Q3 earnings.

Fresh US tariff threats against European nations linked to the Greenland issue dampened global risk appetite, prompting a shift toward safe-haven assets, but later, Donald Trump stepped back from immediate tariff action, which eased concerns of a US-EU trade war, but their relations remained strained.

The Indian rupee also hit a record low of 91.97 against the US dollar.

In the current trading week starting from January 27 till February 1 (except Saturday holiday), the cautious market is expected to be volatile with a major focus on the Union Budget and the Fed interest rate decision. Monthly auto sales data, US economic releases, and further corporate earnings will also be watched.

The BSE Sensex plummeted 2,033 points (2.43 percent) to close at 81,538, and the Nifty 50 fell 646 points (2.51 percent - the biggest weekly fall since September 2025) to 25,049, while the broader markets hit hard with the Nifty Midcap and Smallcap 100 indices crashing 4.55 percent and 5.8 percent, respectively.

According to Vinod Nair, Head of Research at Geojit Investments, in the current week, investors will closely track guidance from the Fed on the trajectory of interest rate cuts, while positioning may be influenced by anticipation surrounding the Union Budget, particularly any measures aimed at easing external trade pressures and supporting capital flows.

Sentiment is likely to stay cautious, shaped by global developments, currency trends, and earnings outcomes, with selective opportunities emerging in segments supported by resilient domestic demand, he said.

Siddhartha Khemka - Head of Research, Wealth Management at Motilal Oswal Financial Services said overall, markets would continue to track developments around global trade negotiations and geopolitical dynamics, while stock-specific action is expected to remain driven by ongoing Q3 earnings announcements.

Here are 10 key factors to watch out for this week:

The market participants will keenly watch the Union Budget 2026 - the major domestic factor - in the current week. The Finance Minister Nirmala Sitharaman will announce the detailed estimated revenue and expenditures for the new financial year 2026-27 on February 1.

Most economists and experts expect the government to maintain continuity and increase capital expenditure for the new fiscal by 10-15 percent over the previous fiscal year, particularly as private sector investment has remained muted in recent months. Further, the fiscal discipline remains a key priority with experts expecting the fiscal deficit to be revised downward to 4.2-4.3 percent of GDP for FY27, against 4.4 percent for FY26, limiting the room for an aggressive and across-the-board capex expansion.

As a result, the budget is likely to adopt a more selective approach, prioritising sectors with higher multiplier effects and strategic relevance, experts said. Railways, defence manufacturing, renewables, AI-led infrastructure, and data centres are expected to remain in focus, ensuring continuity in asset creation without straining public finances.

Performance-linked incentive (PLI) schemes are also expected to be continued and expanded to support electronics, including semiconductors, mobiles, display units, and the manufacturing of clean-tech goods such as EVs, battery storage systems, renewables, and green hydrogen electrolysers.

Experts also expect more details on the National Manufacturing Mission, which was conceptualized in the last budget, and some initiatives for labour-intensive tariff-hit sectors and industries, including textiles, leather, toy manufacturing, among others, as well as for critical rare-earth minerals.

Budget is also likely to focus meaningfully on targeted consumption support, with measures like further income tax relief, higher standard deductions, increased rural and agricultural spending, employment generation schemes, skilling initiatives, and focused welfare programmes.

The December quarter earnings season will be in full swing as nearly 500 companies are set to release their quarterly results in the current week. The list includes the prominent Nifty 50 names like Larsen & Toubro, Maruti Suzuki India, ITC, Axis Bank, Asian Paints, Tata Consumer Products, SBI Life Insurance Company, Bajaj Auto, Nestle India, NTPC, Power Grid Corporation of India, Bharat Electronics, and Sun Pharmaceutical Industries.

Apart from Nifty 50 names, several other key names like Tata Motors, Canara Bank, Bank of Baroda, One 97 Communications Paytm, Swiggy, Meesho, Vodafone Idea, Marico, Vishal Mega Mart, WeWork India Management, ACC, CSB Bank, Gland Pharma, Lodha Developers, Mahindra & Mahindra Financial Services, National Securities Depository, Pine Labs, SBI Cards and Payment Services, TVS Motor Company, Adani Power, Blue Star, Colgate Palmolive, Dabur India, Indian Energy Exchange, Manappuram Finance, Vedanta, Voltas, Ambuja Cements, Glenmark Pharmaceuticals, Jindal Steel, LIC Housing Finance, National Aluminium Company, Bharat Dynamics, and Gail (India) will also announce their quarterly earnings this week.

Auto Sales

Auto stocks including Tata Motors, Tata Motors Passenger Vehicles, Ashok Leyland, Maruti Suzuki, Hyundai Motor India, Eicher Motors, TVS Motor, Hero MotoCorp, and Mahindra & Mahindra will also be in focus this week as they will release their sales volumes data for the first month of this calendar year i.e. January, on the last day of this week i.e. February 1.

The focus will be on whether the double-digit growth observed across segments in December 2025 will be sustained in January.

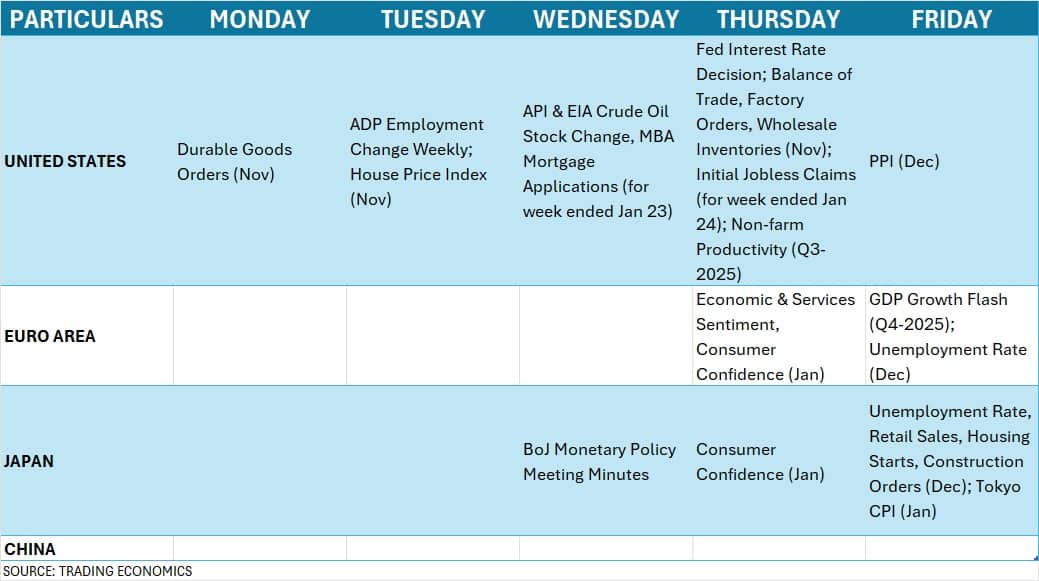

Domestic Economic Data

On the economic data front, industrial and manufacturing production numbers for December will be released on January 28. This follows fiscal deficit data for December, bank loan & deposit growth for the fortnight ended January 9, and foreign exchange reserves for the week ended January 23, which are scheduled on January 30.

FOMC Meet

Globally, apart from geopolitical tensions and Trump tariff threats, the focus will be on the two-day Federal Open Market Committee's first monetary policy meeting of the current calendar year, scheduled on January 27-28. Most economists expect the central bank to hold the Fed funds rate in the 3.5-3.75 percent range after three cuts last year, given steady inflation and resilient consumer spending in the US.

Weekly US jobs data, monthly PPI, and durable goods data due this week will also shape monetary policy expectations.

Global Economic Data

Further, Europe's GDP growth flash numbers for Q4-CY25 and unemployment rate for December, and Japan's recent monetary policy meeting minutes, monthly retail sales, and construction orders data will also be announced this week.

Back home, the market participants will keep an eye on the mood of FIIs (Foreign Institutional Investors) as they maintain persistent selling in Indian equities. In fact, they increased the intensity of selling in the last few weeks as it offloaded over Rs 14,600 crore worth shares in the recent week against over Rs 14,200 crore worth shares selling in the previous week, taking the total current month's outflow to Rs 40,700 crore (as per provisional numbers, which is the highest since August 2025).

The consistent weakening rupee against the US dollar, the delay in the India-US trade deal, and the unimpressive December quarter earnings seem to be key reasons behind FIIs selling, according to experts.

On the contrary, DIIs (Domestic Institutional Investors) continued to provide strong support to the market, though FIIs capped market upside. DIIs' net buying was far higher than FIIs' outflow, picking up shares worth over Rs 20,700 crore in the recent week, taking the total net purchases for January to over Rs 54,800 crore.

Meanwhile, the Indian rupee hit an intraday record low of 91.965 against the US dollar, depreciating 1.07 percent for the recent week to end at a new closing low of 91.635 and sustaining above the upper Bollinger bands.

The US dollar index fell 1.93 percent during the recent week (the biggest weekly fall since April 2025) to end at 97.456, the lowest closing level since June 2025, amid heightened volatility and shifting geopolitical dynamics.

The primary market will see five new companies - Kasturi Metal Composite, Kanishk Aluminium India, Msafe Equipments, Accretion Nutraveda, and CKK Retail Mart launching their IPOs amounting to Rs 226 crore - all from the SME segment - this week, while the action is absent in the mainboard segment.

The IPOs by Hannah Joseph Hospital and Shayona Engineering will remain open for subscription till January 27.

Meanwhile, five new companies will be available for trading on the bourses this week, including Shadowfax Technologies - the only company from the mainboard segment - scheduled for its market debut on January 28. The other four companies - Digilogic Systems, KRM Ayurveda, Hannah Joseph Hospital, and Shayona Engineering (all from the SME segment) will also be listed in the current week.

Technical View, F&O Cues

Technically, the Nifty 50 is expected to be volatile with a negative bias and likely to witness a broad trading range of 24,500-26,000 in the current week after reporting a sharp fall last week. The technical and momentum indicators are in favour of bears. The last week's low of 24,900 is expected to immediate crucial support for the index as below it, the 25,600-25,500 is the zone to watch, followed by 24,300 being crucial support (August 2025 low), however, the immedate resistance is placed at 25,160 (200-day EMA), followed by 25,450 and then 25,700-25,800 being critical hurdle as sustaining above it can get the bulls back on street, according to experts.

The monthly options data also indicated that the Nifty 50 is likely to see a trading range of 24,500-26,000. The maximum Call open interest was placed at the 26,000 strike, followed by the 25,250 and 25,400 strikes, with the maximum Call writing at the 25,300, 25,200 and 25,500 strikes, while the 24,500 strike holds the maximum Put open interest, followed by the 25,000 and 24,700 strikes, with the maximum Put writing at the 24,700, 24,600 and 25,050 strikes.

Meanwhile, as expected, the India VIX maintained its strong uptrend ahead of the Union Budget. It surged 24.8 percent last week (the biggest weekly rally since April 2025) to 14.19 (the highest closing level since June 2025) and hit the 200-week EMA, signalling elevated market uncertainty. It gained for the fourth consecutive week.

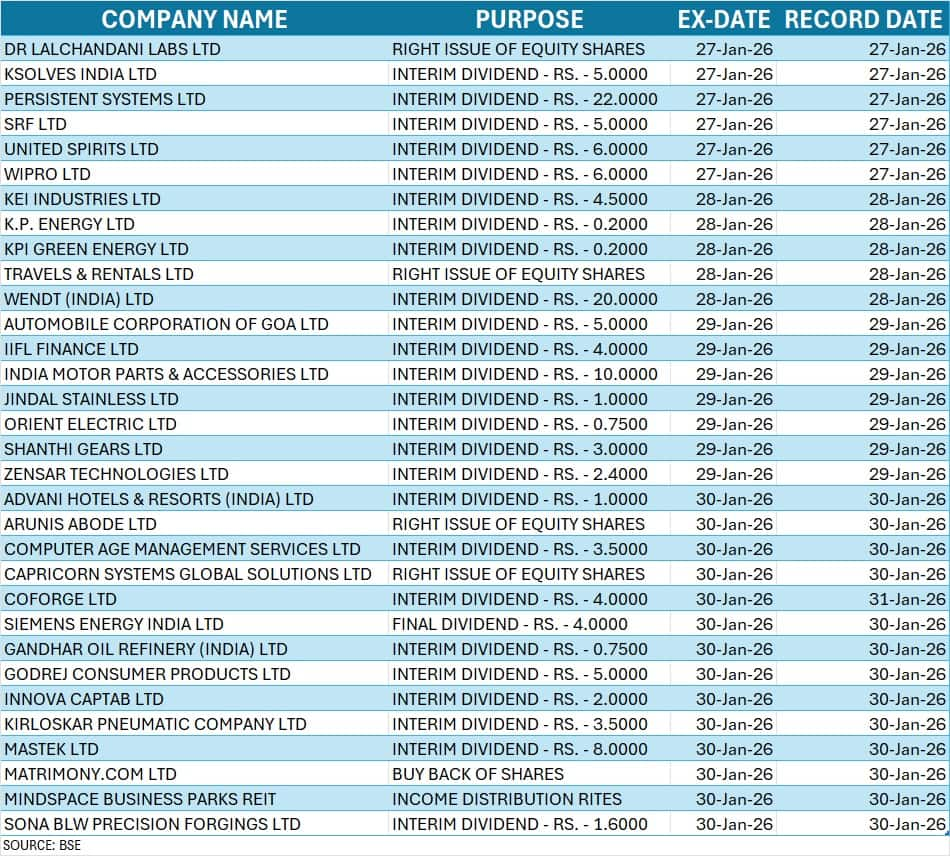

Corporation Action

Here are key corporate actions taking place this week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.