The Bad Bank was a big-ticket item in the last Union Budget. In this Budget too, the banking industry will keenly follow the finance minister’s speech for updates on the proposal, which, unfortunately, is yet to take off

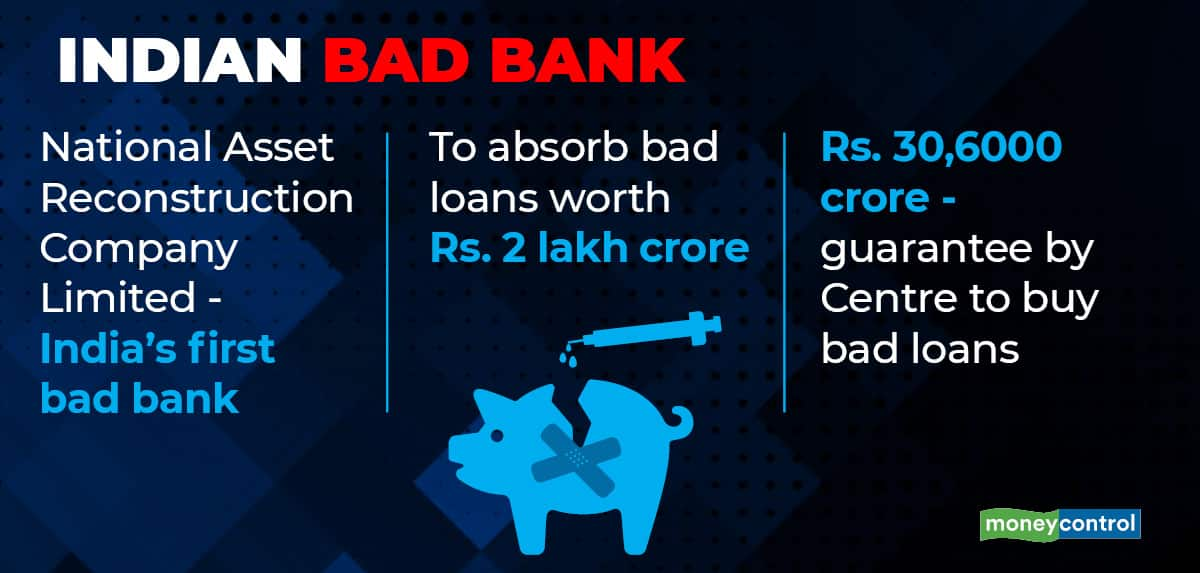

The Bad Bank was conceptualized with the objective of absorbing bad assets from public sector banks for a clean-up of the lenders’ balance sheets. Banks are weighed down by huge amounts of bad loans, or loans on which no interest or principal has been paid for over 90 days.

India has a bad loan problem that cannot be wished away. Stress tests have revealed that banks' gross non-performing assets (GNPAs) may jump from 6.9 percent of assets in September 2021 to 8.1 percent by September 2022 under a baseline scenario and to 9.5 percent under a severe stress scenario, the Reserve Bank of India (RBI) said in its Financial Stability Report on December 29. If the current wave of COVID-19 led by the Omicron variant drags on, the figure could escalate.

So what’s the problem if non-performing assets (NPAs) go up?Well, banks need to set aside more money to cover such loans. These are called provisions in banking industry jargon. The higher the provisions, the bigger is the pain felt by the bank—its profitability subsequently takes a hit. The bank will require more capital to plug the bad loan hole.

A huge pile of bad loans on its balance sheet impairs the ability of a bank to extend fresh loans. When credit growth slows, as was the case to industries over the last few years, the economy suffers. This (economic slowdown and consequent job losses) further impacts the ability of companies and individuals to repay bank loans.

What happened to the Bad Bank proposal?The government, in consultation with RBI, tried to find an answer to this problem and end the vicious circle by keeping bad assets separate from the banks by shifting them to a different entity called the Bad Bank.

But the idea is stuck at the implementation stage. What are the problems here? To begin with, the central bank seems to have some concerns with the dual structure of the Bad Bank through the National Asset Reconstruction Company Limited (NARCL) and the India Debt Resolution Company Limited (IDRCL). Only after approvals come from the RBI will the entity get the initial capital to start operations.

What will banks get in return for transferring NPAs to the Bad Bank?According to details shared by the finance minister at a press conference last year, banks will receive 15 percent of the value of assets being transferred upfront in cash; 85 percent will be given as security receipts (SRs).

It’s not just the organizational structure and regulatory concerns. The Bad Bank may also encounter valuation hurdles in a tough market.

To begin with, most of these bad assets are already fully provided for, written down accounts on the books of banks. They no longer nurture hopes of any meaningful recovery from these assets. Coming to the Bad Bank deal, the most critical part will be how banks arrive at a valuation for the transfer of these assets to NARCL.

Even if some mechanism for price discovery is worked out, the value of the assets is unlikely to exceed 10 percent to 20 percent of the assets at the time of transfer. Banks will want maximum value for the assets being transferred.

If the debt resolution doesn’t happen within a five-year period, the government will have to pay banks against the SRs if the guarantee is invoked. Now, these are really bad assets. Most of these assets have been stuck with banks for long and despite the best efforts of bankers, a resolution hasn’t been achieved. For years, banks have tried to resolve a big chunk of corporate bad debt, but with limited success. There are no takers for such assets. Bad Bank managers will have their task cut out.

What will be the effect of the delayed implementation of the proposal?The delay in Bad Bank execution will mean two things: One, banks will have to find costlier ways to deal with the existing stock of bad assets. Second, the next round of NPAs will add to their pain if there is no resolution to the existing stock.

Although most of the big-ticket corporate NPAs are pushed to insolvency courts, there is a possibility that loans to small and medium sized companies could turn bad if there is no expected recovery in the economy.

While these are all challenges, the Bad Bank’s creation can still help the sector in bad asset resolution with some sort of reformist touch. But timely execution is key.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.