NTPC is expected to report a muted performance in Q3FY26, as soft power demand and lower thermal generation weigh on operational metrics. The power major is expected to announce its earnings for the quarter ending December 2025 on January 30.

While power demand conditions improved toward the end of the quarter, the late recovery is unlikely to materially lift volumes. Earnings, however, are expected to remain largely insulated by the company’s regulated cost-plus framework and incremental additions to its regulated equity base, keeping profit growth modest but stable.

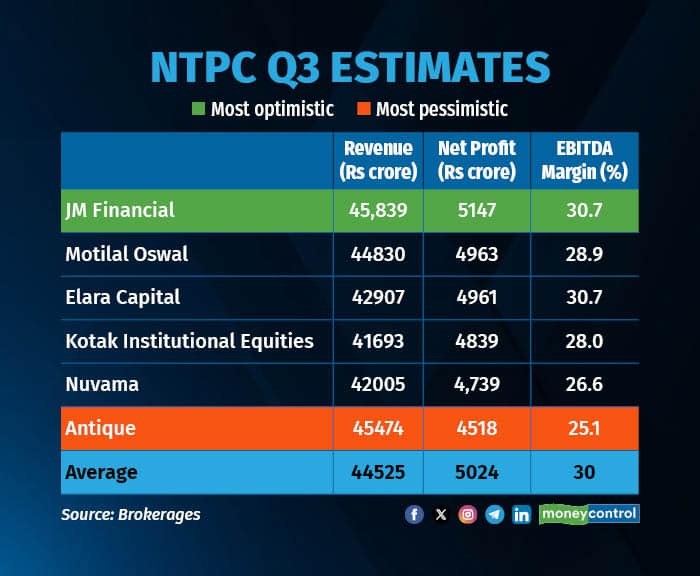

According to a Moneycontrol poll of 6 brokerages, revenue is estimated to rise 7.7 percent year-on-year to Rs 44,525.3 crore in Q3FY26, from Rs 41,352.3 crore in Q3FY25, reflecting steady topline growth. Net profit is projected to increase 6.6 percent YoY to Rs 5,023.7 crore, compared with Rs 4,711 crore in the year-ago quarter, supported by improved operating leverage. The EBITDA margin is expected to expand by about 120 basis points to 30.1 percent in Q3FY26 from 28.9 percent in Q3FY25.

Here are the key drivers for earnings:

Weak demand keeps generation under pressure

Power demand remained subdued during most of the October–November period, before improving sharply in December. JM Financial highlighted that while energy and peak demand rose in December, quarterly energy demand was largely flat, resulting in a year-on-year decline in conventional and thermal generation in Q3FY26. Kotak Institutional Equities also flagged a decline in generation, attributing it to modest power demand, which weighed on thermal plant load factors during the quarter.

Regulated cost-plus model limits earnings volatility

Despite weaker generation, NTPC’s earnings are expected to remain relatively stable due to its regulated business framework, under which returns are linked to regulated equity rather than volumes. Motilal Oswal expects ~8% YoY growth in revenue and EBITDA and ~7% growth in adjusted PAT, while Antique noted that lower PLFs have limited impact on profitability under the cost-plus structure.

Capacity additions aid equity base, ramp-up gradual

Antique highlighted that NTPC’s installed capacity increased on both standalone and consolidated bases during the quarter, with capacity commercialised on a consolidated basis supporting incremental regulated equity growth. Elara, however, noted that limited new additions in FY26 and gradual ramp-up of recently commissioned projects mean that the earnings contribution from these capacities will accrue progressively.

Higher hydro and renewable output offsets thermal decline

JM Financial pointed to stronger hydro generation due to a favourable monsoon and higher renewable output supported by capacity additions during the quarter. While this helped offset the decline in thermal generation, it also led to lower thermal PLFs, reflecting the shift in the generation mix.

Fuel availability and de-risking remain supportive

Fuel supply conditions remained comfortable during the quarter. Antique highlighted ongoing fuel de-risking initiatives and stable coal availability, which helped ensure smooth operations and limited downside risks to margins despite weaker generation.

What analysts will watch

Analysts will focus on generation and PLF trends, particularly whether the December demand recovery translates into improved thermal utilisation. Growth in regulated equity and capex execution will be closely monitored, as will updates on capacity commissioning across thermal, hydro and renewable segments. Commentary on fuel availability, coal linkage conditions, tariff trends and the power demand outlook for FY27 will also be key to assessing near- and medium-term earnings momentum.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.