India is the fastest growing large economy in the world. Even if we assume that the GDP numbers are correct and growth is much more than what former chief economic adviser Arvind Suramanian says it is, the quality of that growth may not be all that great.

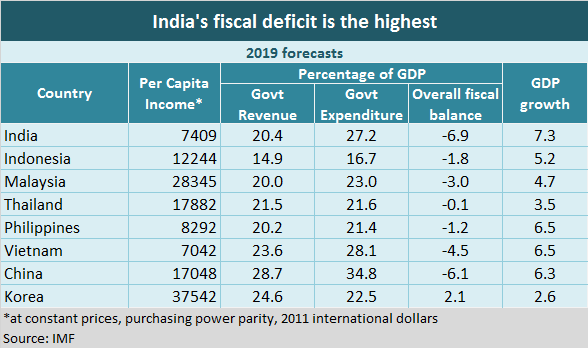

To understand why that is so, consider the accompanying chart. It has the International Monetary Fund’s 2019 forecasts of GDP growth for India and some of the other countries in the region, along with estimates of overall government revenues and expenditure.

The first thing to notice is that the overall fiscal balance, or the difference between government revenues and spending, as a percentage of GDP, is the highest for India. So while India is also the fastest growing economy among the lot, a part of that growth is due to the hefty fiscal stimulus. Vietnam, for instance, is expected to grow by 6.5 percent this year, but its fiscal deficit is a much lower 4.5 percent of GDP. Indonesia’s growth rate is much less, but then so if the fiscal push given by its government to the economy.

For India, the figures include the revenues, expenditures and deficits of the states. What is not included are borrowings by public sector units, which according to some estimates push up total public sector borrowing to around 9 percent of GDP. So the actual deficit could be even higher than the 6.9 percent mentioned in the IMF figures. Indeed, government consumption contributed a fifth of the GDP growth in the Jan-March quarter of 2018-19.

Is India’s higher deficit because we don’t tax enough? The answer to that question depends on which countries we compare ourselves with. The chart shows, however, that India’s overall government revenues as a percentage of GDP is higher than Indonesia, Malaysia and the Philippines, three countries in the region that have higher per capita incomes than us. Thailand’s government revenue to GDP ratio is only a bit higher than India’s despite Thailand being a much richer country, in terms of per capita income.

The reason for the higher deficit lies in the Indian government’s bloated expenditure. As the chart shows, it is much higher than several countries in the region, including South Korea, which is a developed country. A big chunk of these expenses is interest on past debt, which in turn is higher because of excessive borrowing by the government in the past. India’s general government gross debt as a proportion of GDP is much higher than for the other countries in the accompanying chart.

It has been argued that this is hardly the time for the government to curb its expenditure, as the economy is going through a slowdown. Indeed, as this article had pointed out, if we take out the push to the economy given by the government sector, then GVA (gross value added) growth in the March 2019 quarter, from a year ago, slips to 4.96 percent. The government is therefore unlikely to curb its spending, all the more so when investment demand fell off a cliff in the March 2019 quarter, according to the GDP data.

But it is also well-known that the interim budget’s estimates of revenues for the current fiscal year fall in the wide-eyed optimism category. How then to continue spending and at the same time keep the deficit under control? One thing the new finance minister can do is go through not just with disinvestment, but with privatisation. But that is something the Modi government has so far shown little appetite for.

On July 5th, we will eagerly watch how the finance minister proposes to square the circle.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.