The Indian infrastructure sector is poised to sustain its healthy growth momentum over the medium term, supported by healthy and diversified capex outlay seen across various infrastructure sub-segments. During FY2019-FY2026, the capital outlay by the Government of India witnessed a robust CAGR of around 20.3%, primarily driven by a significant outlay in road, railways and the Defence sectors.

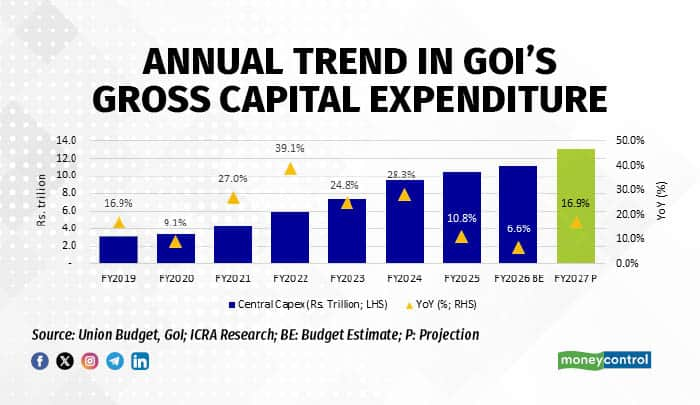

The Government of India’s (GoI) gross capital outlay stood at Rs. 11.2 trillion in FY2026 Budget Estimate (BE) and entails a YoY growth of 6.6% over Rs. 10.5 trillion recorded in FY2025 Actuals (A). Further, the actual capex undertaken by the GoI during April-November 2025 increased by 28.2% to Rs. 6.6 trillion (58.7% of FY2026 BE) from Rs. 5.1 trillion during April-November 2024 (48.8% of FY2025 A).

Likely to overshoot FY25 budget target

The stellar growth in the current fiscal is supported by upfronted spending in H1 FY2026, especially in roads and Defence and a favourable base effect following the moderation observed in FY2025 due to election-related disruptions. Further, rating agency ICRA anticipates the GoI to enhance the allocation for capex by around Rs. 250 billion, taking it to Rs. 11.5 trillion in FY2026 vs the BE of Rs. 11.2 trillion, thereby limiting the contraction in the last four months of the fiscal to 9.4%.

Capex growth in FY27 is likely to be high

ICRA expects the capex target to be set at Rs. 13.1 trillion in FY2027, which reflects a healthy 14% increase compared to Rs. 11.5 trillion capex spending expected in FY2026. While roads and railways will continue to account for a bulk of the capital outlay, other segments like defence and urban infrastructure are expected to be the key beneficiaries.

The increase in the capex arises from the fact that post-FY2027, the scope for further expansion in capex may narrow due to fiscal rigidities expected to set in from FY2028, primarily on account of the 8th Pay Commission. Within this capex, ICRA expects a sizeable increase in the outlay under the scheme for special assistance as loans to states for capital expenditure, from the budgeted amount of Rs. 1.5 trillion in FY2026, thereby supplementing the overall states’ expenditure.

Key sector wise trend:

* Roads

The Central Government’s strong emphasis on road infrastructure development is reflected in the significant increase in the capital allocation to the Ministry of Road Transport and Highways (MoRTH) by more than eight times to Rs. 2.72 trillion in FY2026 BE from Rs. 0.31 trillion in FY2014, increasing at an impressive CAGR of around 20%. Although the growth in capital allocation to the Ministry has remained moderate over the last two years, it is healthy at Rs. 2.72 trillion and accounts for 24.3% of the overall capital expenditure outlay under the Union Budget, which indicates the Government’s focus on the road sector.

ICRA expects the capital outlay for the road sector to remain healthy in FY2027 BE with a range-bound increase over FY2026 BE, which is likely to support the improvement in road execution. Roads and highways continue to dominate Government capex, which has consistently accounted for around 25% of the budgetary allocation over the past five years and is expected to remain at similar levels going forward.

The Ministry had spent Rs. 2.85 lakh crore (105%), higher than the Rs. 2.72 lakh crore of the revised budget allocation in FY2025. In line with past trends, the Ministry is expected to fully utilise the budgetary support in FY2026 as well, given that the road construction till 8 months (M) FY2026 is largely in line with 8M FY2025 levels with the Ministry spending Rs. 1.8 trillion (66% of capital allocation for FY2026 BE) out of the 2.72 trillion till November 2025. It is expected to spend around Rs. 1 trillion during the balance period of FY2026. Further, in line with earlier year budget announcements, the Government is expected to continue with the nil borrowing programme for the NHAI, while keeping the allocations at healthy levels.

* Railways

The overall capital outlay by the Railways touched a historic high of Rs. 2.65 trillion in FY2026 BE (including extra budgetary resources (EBR) via PPPs). While sustaining healthy levels, the year-on-year growth in budgetary allocations is expected to remain range-bound in FY2027BE, as has been the trend over the past two years as well. With broad gauge track electrification nearly complete, focus will remain on decongestion through capacity augmentation—new routes, gauge conversion, track doubling, and dedicated freight corridors. Infrastructure modernisation, including rolling stock upgrades and station redevelopment, alongside safety enhancements, will remain critical. Economic corridor development (e.g. ports and mineral logistics), coupled with accelerated deployment of Kavach 4.0 (automatic train protection system) and improving passenger amenities, are expected to dominate both budgetary priorities and execution strategies.

* Power

Expectations of sustained growth in electricity demand and a rapidly rising share of renewables in India’s generation mix emphasises the need to prioritise strengthening grid resilience and storage capacities. The intermittency associated with renewable power generation highlights the need for accelerated deployment of energy storage, with continued policy support and budgetary allocation anticipated for battery energy storage systems and pumped hydro projects, including viability gap funding.

The budget is also expected to reinforce self‑reliance by extending manufacturing incentives for grid‑scale batteries and promoting backward integration for solar module manufacturing ecosystem. Concurrently, higher allocations are anticipated for augmenting transmission infrastructure—particularly interstate systems and green energy corridors—through High Voltage Direct Current (HVDC) lines, pooling substations, and network strengthening. Continued reforms in the distribution segment remain critical, with enhanced funding under the Revamped Distribution Sector Scheme (RDSS) and sustained emphasis on smart metering to improve billing efficiency, reduce Aggregate Technical & Commercial Losses (AT&C) losses, strengthen demand forecasting, and improve discom cash flows.

Summing up, a combination of adequate budgetary allocation, planned asset monetisation and long-term financing coupled with favourable regulatory changes are expected from the Budget, which will provide the requisite stimulus to the infrastructure investments for the future.

(Suprio Banerjee, Vice President & Co-Group Head, ICRA Ltd.)

Views are personal and do not represent the stand of this organisation.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.