Over the past several articles, we have consistently examined the possibility that an AI-driven excess is quietly forming within the Mag 7 complex. The December quarter results have not invalidated that thesis; they have sharpened it.

Operationally, Big Tech remains strong. Cloud growth is healthy. Meta delivered robust earnings and free cash flow. Microsoft’s Azure continues to expand at scale. Google Cloud growth has accelerated meaningfully. These are not weak businesses.

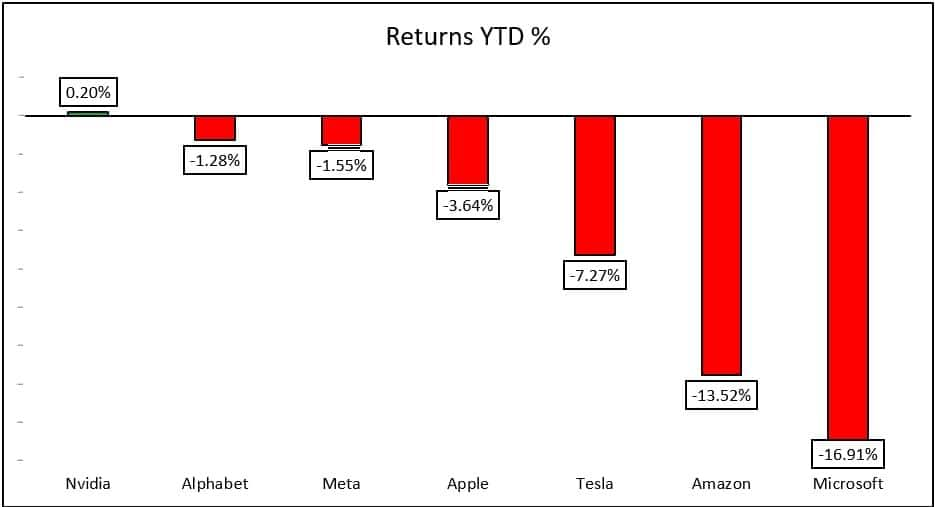

Yet markets are uneasy. Since the start of 2026, the Mag 7 as a group has not generated returns. Microsoft, Amazon, Tesla, Apple, Meta, and Alphabet have corrected following their quarterly numbers, while Nvidia is yet to publish results and is marginally positive at best. Leadership is no longer emphatic. The Bloomberg - BM7T Index, which tracks the MAG7 stocks, has been consolidating for four months, and the momentum that began in April 2025 has visibly faded.

Part of this normalization is fundamental. Over the past five years, leverage across the Mag 7 has meaningfully expanded, particularly at Meta and Alphabet, while Tesla, Nvidia, and Amazon have also added to their balance sheets. Only Microsoft and Apple have reduced debt. Rising capital intensity is increasingly being supported by higher borrowing, altering the risk profile.

(Source: Investing.com)

(Source: Investing.com)

What has unsettled investors this quarter is the scale of spending. Amazon’s proposed $200 billion capex for 2026 is unprecedented. Alphabet and Meta are committing similarly aggressive outlays. Nearly $685 billion in combined AI infrastructure investment is not incremental - it is transformational.

But here lies the tension: Capital expenditure is rising faster than free cash flow. Balance sheets remain strong, yet the era of surplus cash compounding is being redirected into an arms race. Markets are beginning to ask a simple question - when does this spending translate into durable incremental earnings?

I have seen similar cycles before - Fiber in 2000, Energy in 2014, Data centers in 2018. Innovation was real. Demand was real. But when capital intensity spikes across an entire sector simultaneously, returns become sensitive to execution and discipline.

This does not mean AI is a bubble. It means expectations are elevated while growth is normalizing and spending is accelerating. That combination compresses return potential.

The Mag 7 still accounts for over a quarter of S&P 500 earnings and a third of its market cap. When their return profile moderates, the broader index feels it.

AI may well redefine productivity over the next decade. But markets do not price decades; they price cash flows. And in 2026, the story has shifted from growth at any cost to returns on capital deployed.

That distinction will define the next phase of this cycle.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol are their own and not those of the website or its management. Moneycontrol advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.