In 2016, online learning firm Toppr was all the rage. Not in the headline grabbing, massive fundraising way that its ecommerce and fintech peers were, but in its own way, it was on fire. Toppr had one million students using its platform. It had achieved this raising $12 million in three years — paltry considering how many others had raised much more every few months.

A year earlier, founder Zishaan Hayath had rolled out a new Toppr — a revamped, new-look platform improving on its promise of tech-based learning for students from Class 5 to 12 — nearly endless question banks, questions that adapt to your personal difficulty level and curated study material. Things were looking good. The education market was humongous, entrenched in old practices and ripe for disruption with internet usage exploding. Investors, employees… everyone was upbeat.

The Toppr product was always highly spoken of, by students, parents and even its rivals in board meetings and investor pitches. An intuitive app, attractive visuals, a product that promised to make learning interesting. For example, you wouldn’t get 20 breezy questions, and then hit a wall with 10 of the hardest ones. It promised to make the questions tougher incrementally and gradually, depending on how you were at answering them.

In those heady days of growth, rival app Byju’s was always around, but every sector has competition. The company was not too worried. CEO Hayath even claimed students spent three times as much time on his app than on Byju’s.

Toppr was so confident that it even rolled out a snarky advertisement campaign. Byju’s, India’s highest valued edtech firm, calls itself “the learning app” in all its advertisements. Qualifiers came in later ads — “all new and personalised”, but “the learning app,” along with actor Shah Rukh Khan remained part of all of its ad campaigns. In April 2019, Toppr rolled out a television commercial campaign touting itself as “the better learning app.” Better than what? It did not say, but the ad was a subtle dig at Byju’s, already a multibillion-dollar company.

Toppr’s snarky attempt at one upmanship and showing it has a better product seems ironic considering the final outcome. Today, Byju’s, the $12 billion company, is close to acquiring Toppr — for whom fundraising has been a permanent struggle — for a paltry $150 million. Sources tell Moneycontrol the deal should be announced in a month, and Toppr’s investors are debating whether to take a cash exit or take shares in Byju’s instead.

But the “better learning app” ad is about more than mocking a rival. It is about promise, even reality, to some extent. But eventually, having the better app did not quite matter.

This is the story of how Toppr had to fold up inside Byju’s, its opportunities and struggles over the years. It has been pieced together weaving disparate strands from people inside the companies, investors, competitors and others. They all spoke to Moneycontrol on condition of anonymity. Byju’s and Toppr did not respond to queries seeking comment.

Toppr was founded in 2013 by Zishaan Hayath, an IIT-Bombay graduate and a well-known face in the Mumbai startup scene. In 2008, Hayath co-founded Chaupaati Bazaar, a phone-commerce startup that enabled India’s mobile users to buy home appliances, children’s products, books and magazines over the phone. In 2010, it was acquired by Future Group — India’s largest retailer then — after which Hayath worked at Future till 2013 as Vice President of Products.

Byju Raveendran couldn’t have had more different origins. It’s a story that has become a legend today — Raveendran is an engineer from Kerala who turned teacher. His teaching methods and concepts were a hit with students, and he went around the country running Byju’s as an offline test preparation centre. At some point he was so popular that he conducted classes for 20,000 students in a stadium. From 2015, Byju’s transitioned from classroom learning to an app and tablets.

For the last six years at least, Raveendran and Hayath have been playing in the same space — online education content for students from the 5th to the 12th grade — video classes, concepts, stories and test series.

They have expanded into other areas more recently, but this was the core. And according to an investor who evaluated both firms in 2016 and later, Toppr always had the better product. “They had very good question banks. Student feedback was great. Based on how you answered those questions, they would give the next set of questions. Very intuitive,” this investor said.

Moneycontrol spoke to three students who used both products over the last few years. Two of them said a few years ago the Toppr app was much smoother while the Byju’s app lagged when transitioning from one question to another, or switching from class to practice.

One student in the 9th grade said she liked the Byju’s app, but her phone constantly heated up using the app. She later found Toppr’s teaching and customer support better, and the app was slicker too.

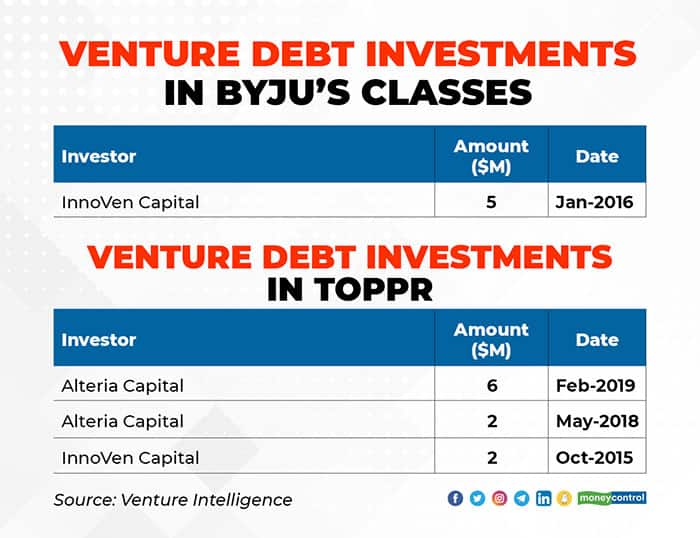

Funding gapBut revenue and funding were always hard for Toppr to come by. Byju’s raised funds from top investors, including Sequoia Capital, Lightspeed Venture Partners and Manipal University’s Ranjan Pai. Toppr also raised funds from SAIF Partners (now Elevation Capital), Helion Ventures and Eight Roads Ventures — all respectable names — but was unable to raise follow-on rounds of funding anywhere as quickly as Byju’s did. The gulf has become wider recently, but funding data from the early days tell a story.

Toppr raised $2 million in March 2014, $10 million in May 2015 and $7 million in August 2017, while Byju’s raised $144 million in 2016 alone, across 3 rounds. It raised another $71 million in 2017.

By the end of 2017, Byju’s had already raised 12 times the capital that Toppr had. But the real fundraising hadn’t even begun. In 2018, Byju’s raised $567 million, including a mammoth $540 million round, led by Naspers, General Atlantic and Canadian pension fund giant CPPIB. That one deal transformed Byju’s, its promise and the entire edtech space. The same year, Toppr raised $35 million.

As much as products, services and founders are important, in the competitive fast-growing startup space, fundraising moves the needle like nothing else. Byju’s constant fundraising threw everyone else out of the water. No large investor had the guts to compete with Byju’s billions, a strategy reminiscent of Uber. The ride hailing giant became famous for raising billions constantly with investors fuelling losses but beating competition and winning the valuation game.

Byju’s case is a little different. It has not been burning cash like Uber, or like other Indian internet startups. At the other extreme, Byju’s has been profitable (more on this later)

So, when its operations do not need endless venture capital, why has Byju’s raised so much money? “Vision, aggression and booting out competition,” said an edtech investor, summing it up.

“Byju’s does not burn cash. They keep raising money because they want to consolidate their market leadership, and make sure no one can even smell an opportunity to challenge them. When you can raise that much money, you can dream of a multibillion giant with potential global dominance, which is how ambitious Byju (Raveendran) is,” the person added.

In a classic startup paradox, Byju’s has been able to raise billions because it tells investors that it does not really need these billions. It is profitable anyway.

The real differentiatorAlong with funding, there’s another big reason for Byju’s explosive growth — its 20,000 and growing sales team, larger than many conglomerate call centres.

“See, both Byju’s and Toppr are in a space where you have to push for sales. You have to create that demand. Revenue is not going to come in automatically or from being discovered online. You have to push and push,” says a senior executive in the space.

So, Byju’s hired aggressively, courting 21-year-olds fresh out of college with a salary of Rs 10 lakh per annum (30 percent variable pay). One person inside Byju’s told Moneycontrol that the company today has 40,000 sales executives — business development (BD) executives as they are known internally. This includes a newer concept of BD trainees. Within one month if they perform, they are converted to full-time employees, else they are let go, the person said.

These executives call parents, visit them, cajole them, offer scholarships and discounts that expire if they don’t bite immediately and create a sense of FOMO — fear of missing out. This sales machinery is the cornerstone of the company’s scale, people say.

Business wise, it’s a strategy that has paid off phenomenally. Revenue doubled in FY20 to Rs 2,800 crore, and could be close to the billion-dollar mark (Rs 7,000 crore) for FY21, driven by the pandemic, according to reports. And, it is profitable, something almost no Indian unicorn — many older than Byju’s — can claim to be. It had profits of Rs 20 crore in FY19, a figure that is only expected to get bigger as revenue swells.

In the same space, with a similar product, Toppr had Rs 56.4 crore of revenue in FY19, its last publicly available figures. This could have doubled at best recently, but is still a far cry from Byju’s. And three people involved with both companies say there is only one big reason for this.

“Zishaan (Hayath) was never able to crack sales. Toppr did not hire good sales talent early on,” said one person. Hayath initially hired top engineers like himself to drive sales, a move that, in retrospect, did not work. Hiring engineers for sales stems from a product-driven mindset — a good thing you would think — but success in this space has been determined by sales muscle, something Toppr realised late, and that its CEO acknowledged recently.

Toppr, in fact, priced its products higher than Byjus for a few years. Feeling this was not working, it later reduced prices to increase sales.

But volumes did not take off even at a lower price, and this hit overall revenue even more. While multiple people say Toppr’s product was superior, it was not better to the extent that people were leaving Byju’s and using Toppr, or discovering Toppr despite Byju’s sales acumen.

In addition, it is a fact that in any sector, the player that is able to raise funds fastest is able to corner the market. Whether the better company got more money, or whether more money made a better company, becomes a chicken-and-egg question. But Byju’s took a clear lead, raising hundreds of millions of dollars each year till 2020, from investors such as General Atlantic, Naspers and Tencent. In 2020, the year of the pandemic, which turbocharged edtech, Byju’s raised a billion dollars, more than the entire industry the previous year. In 2020, Toppr was supposed to have raised Rs 350 crore ($47 million).

Funding troublesOf the $47 million that Toppr raised in July 2020 from Foundation Holdings, a UAE-based family office, nearly half the money still has not come in yet, a person directly aware of the matter said. While Moneycontrol could not ascertain the exact reason — it could be because the money was contingent on a revenue milestone, or was supposed to be in debt or convertible warrants — the deal was in trouble from the start. “The round barely closed. It dragged on for months on end. One proposed investor pulled out. Then another got cold feet. Then everything gets delayed. All the investors were so relieved when the deal, in whatever form, got done,” the person added.

But in a warning sign, even in the supposed $47 million, except Kaizen Private Equity (which first invested in late 2018), none of Toppr’s existing investors participated in the round. Unless you’re an extremely mature or highly valued company (which Toppr isn’t) this is rare. It is likely that the investors were aware that Toppr’s final outcome would hardly be spectacular in which case why invest; or they weren’t sure what their investment had yielded so far, and hence were not willing to double down.

Like many startups world over, Toppr’s fate is very tightly tied to its fundraising struggles. In any sector, when one company is able to raise large rounds of capital quickly (as Byju’s did), other players in the sector have to scramble for survival.

“The promise was there. The moment they advertised, spent on sales, revenue spiked big time. The growth was up to expectations. But the moment investment in marketing slows a little, so does growth. So, you constantly need to be raising money,” an investor said.

Some people close to the company wonder whether Toppr would have been better off as a smaller, maybe niche but profitable company. But that seems like wisdom in hindsight, because small and niche are not words that resonate with most startups. The DNA of internet startups is growth — finding the next big thing, raising venture capital, and chasing market leadership to justify all that venture capital. To think of being smaller and profitable, after years of chasing growth and raising money, is to try to change your company’s DNA overnight, and that’s next to impossible.

Toppr was on a treadmill where it constantly needed that large round of funding to build the large outcome that its early investors were promised. The large round never came, and funding struggles almost started defining the company’s trajectory.

For most entrepreneurs, each round of funding is an exhaustive, seemingly never-ending exercise that distracts you from your core vision. You are raising money for that vision, but the process of fundraising — flights, pitching to multiple investors, having due diligence done on you with a fine tooth comb, finalising legal agreements — takes months away from focusing on the core business and issues. More so when you are Toppr, and raising money is hard anyway.

Toppr was growing, but not quickly enough; it had revenues but not large enough; and it was not profitable. Given this, “either you keep raising money, or you find a home for the company”, an investor said.

Slowly and perhaps unintentionally, Toppr started becoming more like Byju’s as well. It hired more sales executives, tried to make sales a core function, and became more aggressive.

Along comes ByjuWhen Byju Raveendran offered to buy out Hayath and his company a few months ago, it came as a relief to Hayath, said a person close to the transaction.

Hayath is still very bullish on the space, and one person said Hayath and Raveendran got along well — if their visions can align, then building Toppr inside Byju’s without looking for funds constantly could be a relief.

Tellingly, even as the Byju’s offer came, Toppr had two investment term sheets of $20 million and $60 million, respectively, said a person directly aware of the matter. Moneycontrol couldn’t ascertain the names of the investors, but they were offering to invest at Toppr’s existing valuation, which was a no go for Hayath and other investors, whose stakes would get diluted. Byju’s offer of $150 million — it could go up if some investors take stock instead of cash — is above the $100 million Toppr was valued at eight months back. But having raised $90 million over the years, a $100 million valuation is poor.

“From Toppr’s point of view, that figure ($150m) is just enough for Toppr to find itself respected and accept, and just enough for its investors to get a half-decent outcome. No one loses money at least, and from Byju’s point of view, that figure is not huge for a company whose fundraising abilities are unparalleled,” a partner at a venture firm said.

Moneycontrol could not ascertain Toppr’s current revenue, but its user numbers do make it an important player in the market. In late 2019, Toppr had about 3 million users on its platform, which became 10 million in March 2020, and 30 million in September 2020. In grades five to eight, the engagement rate is 100 minutes per day, while in higher grades, it is about 140 minutes per day, Hayath told The Morning Context in an interview last year.

So what does all this mean for Toppr? “It leaves a bittersweet taste. It is a decent exit, for many years of toil for everyone. The endless funding struggle will end. I think he’s doing the right thing by taking the deal. This kind of consolidation in a bit of a distress situation is always hard to see, especially considering that if the superior product could have cracked sales everything could have been different,” a person close to Hayath said.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.