")

PhonePe founder and CEO Sameer Nigam never pulls his punches. So, it wasn’t surprising when he shot back, “Can my next ad be: please don’t install my app,” when we asked him how he would lower his market share to adhere to NPCI’s guidelines on market share.

The National Payments Corporation of India (NPCI), which operates digital payment rails such as UPI, IMPS, and BBPS, shared guidelines in March on how it plans to cap the market share volumes of payment apps at 30 percent. The move is aimed at providing opportunities to multiple players and to mitigate the systemic risks that could arise from a few dominating the space.

The volume cap for a Third-Party Application Provider or TPAP (payment apps such as PhonePe, Google Pay, Amazon Pay etc) will be effective from January 1, 2021. Existing TPAPs that exceed the volume cap as of December 31, 2020 will have two years from the effective date to comply with the provisions. However, bank apps (Paytm, Axis, etc) have been exempted.

While adoption of digital payments has intensified in the last few years, the pandemic has accelerated it, with UPI clocking 3.5 billion transactions in August 2021. In value terms, monthly UPI transactions grew from Rs 2.06 lakh crore in March 2020 to cross the Rs 6 lakh crore mark in just 17 months.

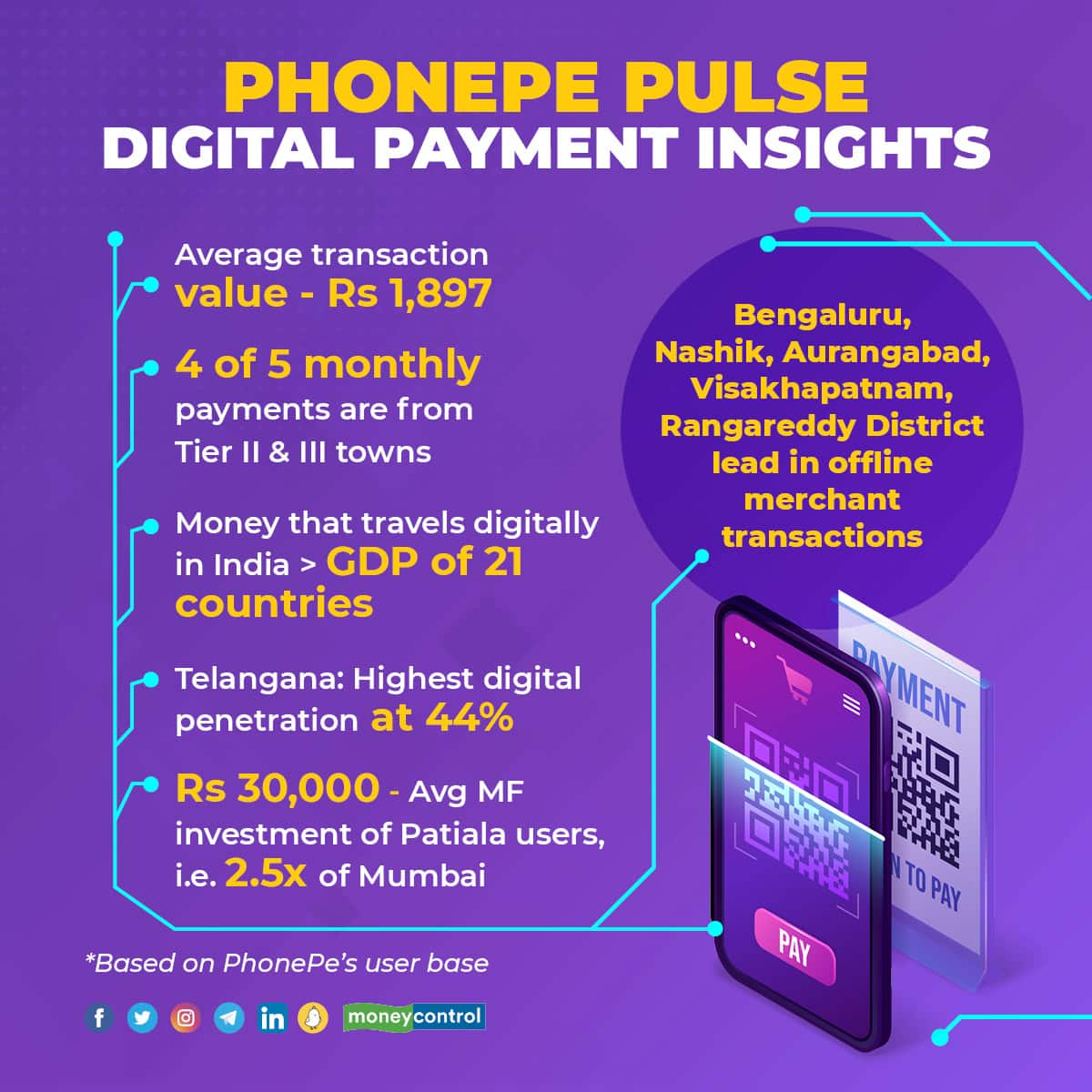

PhonePe dominates UPI transactions with a 46 percent market share. This has given the fintech the confidence to share data, insights, and trends on digital payments in the country through a website: PhonePe Pulse. The company says that with its market share, this data is representative of India’s digital payment habits.

In an interaction with Moneycontrol’s Chandra R Srikanth and Priyanka Iyer, PhonePe Founder and Chief Executive Officer (CEO) Sameer Nigam said that PhonePe as a business cannot deliberately reduce its share in a free market. Over a freewheeling conversation, Nigam outlined his plans to enter businesses such as AMC, as well as his plans for lending. Edited excerpts.

Why the move to put out granular data? Reserve Bank of India (RBI), NPCI has high-level data. There was a committee that anyway recommended that internet companies should put out non-personal data. Is it a precursor to that? Because you were not in favour of that.I am still not in sync with that. Just because it’s a good idea, I don’t think it should become a law. Just because one thinks that people should share data, it is not fair to tell private businesses or enterprises that they need to put out data. NPCI and RBI are very different because they are government-backed enterprises. That is the public domain, that is taxpayer money, while PhonePe and its competitors are not. We have chosen to do this because we were a beneficiary of the open ecosystem thinking concept, not because some law is pressurising us.

It is because people like Pramod Varma and Nandan Nilekani and then all these folks at India Stack collaborated with people in RBI and NPCI and said what if all banks expose their user base through Application Programming Interfaces (API) to apps like PhonePe. If they had not said let’s open up the market, this would not have happened.

If every kid who’s graduating today from college knows where people are making digital payments, knows what’s happening in their district or State, it will be helpful. Everyone is talking about hyper-local businesses, but where is the data to tell you about the demand and supply. Data has been typically gathered and made available to government agencies. I’m sure NPCI has all the data. So, for PhonePe the motivation was to give back to the ecosystem in terms of information and let it spawn questions and opportunities. We are not doing this either under duress or to set the tone that this is what everyone must be obligated to do. Just because we are doing it, I don’t think everyone should do it.

Is it also because you want to capture some mindshare — when people are talking about digital payments in India they will look at PhonePe? If we look at your monthly transactions, it is dominated by UPI, not so much by card or net banking. So, don’t you think this is a very narrow lens of looking at digital payments?Our transactions, while skewed towards UPI, are reflective of the direction of the market overall. UPI’s total transactions last month were 3.5 billion. All wallets put together were around 400 million as per RBI data, which is sub-10 percent of UPI. Wallet and card transactions together are 25 percent of the market. PhonePe is well over 1.5 billion transactions today, so the data is representative enough.

We have the second-largest aggregation of cards on file today. When the new payment aggregator guidelines kick in, we will be putting tens of millions of cards into the token system. We are probably the largest or second-largest RuPay transaction gateway in the country. It is a very large volume of card processing that we do.

It is fair to say that we are not a perfect representation of how the market overall would look in terms of instrument split. But at an aggregate level, the sheer volume of data is representative of consumer behaviour. We are going at PIN code levels, not saying we know individuals best.

The idea is to have people question a lot of stuff, not to say we are the largest. I don’t care about that. I care way more about: can this help?

Does this make us the authoritative source? The right way to answer that is that there are a lot of people in the industry, including regulators, government and media who are curious about how payments are opening up.

Will this still be representative when you move to 30 percent market share?You are assuming I will.

But don’t you have to?It is not a norm, not even a regulation; it is an NPCI guideline. There are three levels: zero-merchant discount rate (MDR) is a law, two-factor authentication is regulation, and this is a guideline.

So, are you saying you don’t have to adhere to it?I didn’t say that, I am just clarifying the technicality. I have not been giving cashbacks for the last two-and-a-half years. No one new is entering the market. It’s a perfectly competitive open ecosystem — anyone can enter. If no one is entering because there is no incentive on zero-MDR, that’s not my problem. If no one’s putting cash in the system because investors are saying it’s not worth it, that’s not my problem. If despite 150 apps having launched in the last four years, we have a large market share, none of that has anything to do with me — I’m just doing my job.

If PhonePe is the app of choice in a perfectly competitive market space, I can’t do anything about the market share cap.

So, what will you do when the deadline kicks in on January 1, 2023?I can’t do anything anyway; they have to do what they want to. What do you want me to do? Tell the next person that installs PhonePe: ‘Don’t use me’? Can my next TV advertisement be ‘Please don’t install the PhonePe app’ because our market share is the best?

That is ludicrous, right? I can’t tell people not to use my app, I am a businessperson. The cap applies to us until January 2023, and that’s five quarters away. There is no point losing my sleep over this. Because NPCI has to tell us what we have to change.

They can tell me that the network will fail transactions, I will wait until that happens. Let them come at me for doing right in an open market. It’s not the government’s job, that is why it’s not a law. It’s not the regulator’s job, that is why it’s not a regulation. The network can dictate.

And NPCI’s Managing Director and CEO Dilip Asbe has said on the record that they will look at market conditions and give extensions when necessary; they will not hurt the growth of UPI.

For students and developers, regulators, and government bodies we will not monetise. I would love to be able to add a lot more data down the line. Merchant analysis is very different from consumer analysis work. We have built a ton of data sets around risk and fraud practices, but we need to talk to regulators and law enforcement agencies as there are certain sensitivities about publishing that data in the public domain. So, different data sets will come in.

We spoke with BillDesk Co-founder Srinivasu MN. He was of the opinion that payment companies have to start making money, otherwise they will end up like the telecom sector. With zero-MDR, how will companies make money in India?They will make money on cards. Tokenisation is coming. They will make money by going international because UPI international makes money. They will make money on wallets if wallets don’t become interoperable and get flow to zero. Wallet interoperability will drag wallet MDRs to zero very quickly.

If at any point in the next two years we realise the payments industry is not healthy enough, the top two or three players will survive like in telecom. Or, I think the decision-makers will realise that we have stumbled upon the most innovative, disruptive interoperable ecosystem ever, and we need to restore market forces in India. I’ll bet on the latter, but my gut says it will be a bruising battle before that. Srinivasu is right.

Payments will be the graveyard of a lot of businesses that don’t get to scale and sustain. Because it is exactly like telecom. Any industry that is healthy at scale should allow for new entrants. But to say that the market cannot have consolidation based on preference is false.

When you say going international, what plans do you have there?Everything changed due to Covid-19, else we were looking at entering new markets in 2021 to test out. Our investor Walmart had said Mexico seemed interesting. Dubai and Singapore, too, as NPCI took UPI there. After the second wave, we decided to wait it out. Because we are much more bullish on being able to impact financial inclusion deep in the Indian market. With a 10-year view, we are better positioned in trying to solve that for Tier III markets in India.

You seem to be getting a series of licenses — insurance broking, account aggregator, etc. How will you monetise in these verticals because you are more of a facilitator in these spaces?Account aggregators have to pay for themselves. It is a standalone business where you charge the Financial Information Users (FIUs). The reason we got it was to get in very early to make sure the ecosystem actually sustained itself, like UPI. You need a few accelerants. We were one of the accelerants for UPI. We will be an accelerant for account aggregators. We will not just build for PhonePe, but for anyone in the market.

On the consumer or merchant side, our aspirations are to tear open the sectors we get into in the financial inclusion space — small ticket, very large volume, SIPs, sachet insurance etc. I think there’s a lot of money in it if you can crack it. I am pretty bullish about what we can do there.

Have you also applied for an Asset Management Company (AMC) license?We are one of the fastest-growing mutual fund distributors. There is a bunch of licenses, and you will see them.

So AMC, stockbroking, and NBFC?At the minimum.

Do you also believe that fintechs in India need to get into lending to make money?No, I don’t think that is true. BillDesk is making money; Razorpay is. I think the right fitment is lending. It is a very attractive sector to be in; it’s a natural adjacency and people should and can be in it.

(But) It is folly for people to believe just because they did well in payments they will do well in lending. One does not beget the other, it’s just an adjacency. Will we get into lending? All these years I said that once my payment businesses achieve scale and maturity and the financials are healthy, we will get in. So, that’s your cue, we are getting there.

You hold a 36 percent stake in MapMyIndia, which is going for an Initial Public Offering (IPO). Will you be selling a stake or holding the entire stake post their IPO?We will be selling some stakes back to the promoters. I’m very bullish on MapMyIndia. They have been profitable for 10 years, growing at a steady pace, and have more points of interest than even Google Maps. I won’t sell a share until I have to.

What’s your take on what is happening with respect to Apple and Google? They seem to be facing the heat globally. South Korea recently cracked down in terms of commissions. Do you think India needs to do something similar?I think India will do something that is at the Competition Commission of India (CCI) or legal level. I think the single issue is that they are a natural monopoly. I don’t mind the challenge of 30 percent on the Google Play Store.

I have a problem with the fact that the Play Store is so dominant because of the practices that have endured for 10 years. Play Store distribution policy should be illegal. You can’t say open-source and then say I am the only app store.

Are you well capitalised for the licenses, businesses, and initiatives that you are pursuing?We are going to become more of a financial services group than a super app. We are very well capitalised and backed by long-term investors. So, we're not going to raise money, not going for an IPO.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.