Budget 2023 has proposed many tax benefits for the common man, such as increase in the basic exemption limit to Rs 3 lakh (from the current limit of Rs 2.5 lakh), eligibility of rebate increased for income up to Rs 7 lakh (from the earlier limit of income up to Rs 5 lakh), adjustments to tax slabs and reduction in the maximum rate of surcharge from 37 percent to 25 percent for the super-rich.

The key point to note here is that all of these benefits are available only under the new tax regime, which was introduced by the government back in 2020. If you choose to be covered under the old tax regime, you would still be governed by the existing provisions and tax rates.

Under the new tax regime, most of the deductions and exemptions that are available under the old regime need to be foregone. One of the most common deductions that helps reduce tax outflow is the payment towards housing loan.

Benefits under the old regime if you take a housing loan

If you have found your dream home and decided to avail a housing loan, here’s how the old regime helps you save tax.

Equated monthly instalment (EMI) payments towards housing loans comprise two components ― interest on the loan and the repayment of principal. Each of these components has a tax benefit under the old tax regime. Here’s a look at some of the benefits of the old tax regime.

1. If the house towards which the loan is availed is occupied by you (self), interest on housing loan can be claimed as a deduction up to Rs 2 lakh. And this amount is per person in case of co-owners and co-borrowers of the loan.

2. If the house is given on rent, interest payable on home loan can be deducted from the taxable rental income. However, the maximum loss under the head house property (after deducting interest from taxable rental income) is capped at Rs 2 lakh. Any excess loss is allowed to be carried forward and is eligible for adjustment with taxable rental income of future years.

3. Apart from interest, the principal component of EMI can be deducted from total income, under Section 80C up to a maximum of Rs 1.5 lakh.

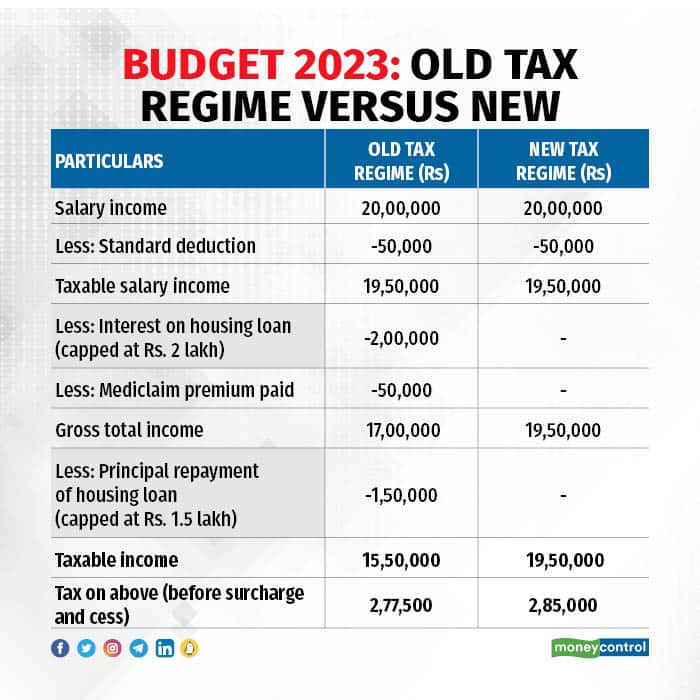

Let us consider an example. Say, you have taken a home loan (for a self-occupied house) of Rs 40 lakh at 9 percent interest rate, repayable in 15 years. The annual EMI payable would be about Rs 5 lakh, consisting of Rs 3.50 lakh of interest and Rs 1.50 lakh as principal in the initial years. If you are a salaried taxpayer in the 30 percent tax bracket, the tax payable under both the regimes would be as under:

So, if you are making EMI payments and also have other deductions and exemptions to claim, you may be better off following the old tax regime, than the new one.

4. Are you currently staying on rent? If you are a salaried taxpayer staying in a rented accommodation, you would note that a key component of your salary, viz., house rent allowance (HRA) can be claimed as a tax exemption subject to certain threshold limits. The exemption for HRA is available only under the old tax regime.

Whilst it may not be a straight-forward answer, it is important to do a quick math to check whether the old tax regime with all the exemptions and deductions or the new tax regime with lower tax rates is more beneficial for you. So, choose wisely!

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.