Most investors don’t lose money because they pick the wrong asset. They lose out because they don’t stay invested long enough.

Market volatility, short-term underperformance, and the constant noise around returns often push investors to exit just when time is beginning to work in their favour. The true power in long-term investing comes from patience.

To see how this plays out, let’s look at some simple numbers.

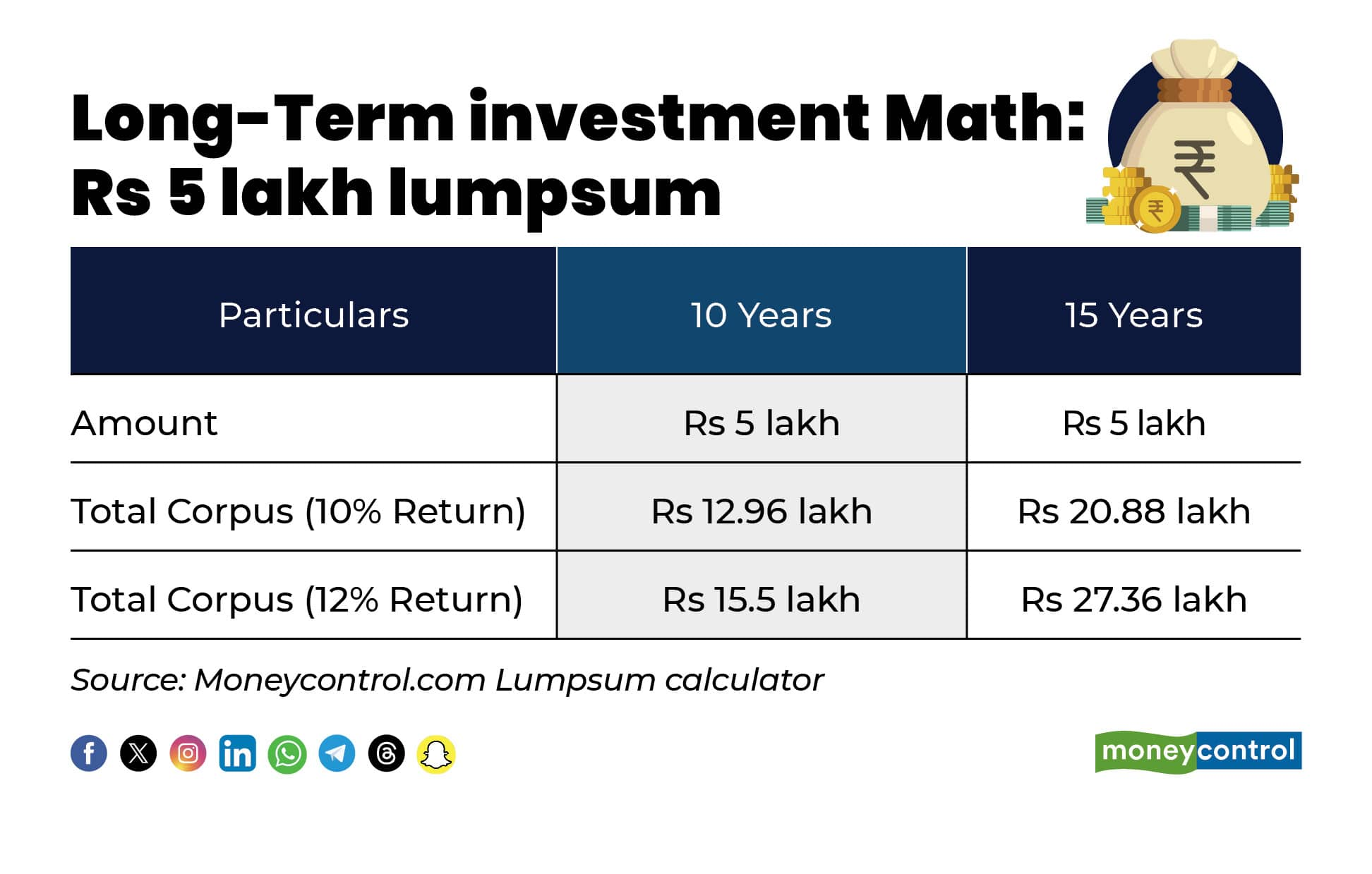

What time does to a Rs 5 lakh investment

Assume an investor puts Rs 5 lakh as a lump sum into a core equity-oriented portfolio. This is not an aggressive assumption for a mid- to high-income salaried professional who has built savings over five to seven years of working life.

Now, let’s see what time does to this investment. For this example, we have assumed a 12 percent annual return, broadly in line with the long-term historical average delivered by diversified equity mutual funds across market cycles. Equity large-cap funds have delivered returns of 13.91 percent over the past 10 years, while equity flexi-cap funds have generated 14.58 percent during the same period.

A Rs 5 lakh lump sum can grow to about Rs 15.5 lakh in 10 years at a 12 percent annual return. If the investor simply stays invested for another five years, the corpus rises to roughly Rs 27.36 lakh. The key point here is that the investor hasn’t added fresh money, the growth comes purely from compounding, where earlier gains begin generating their own returns. Extend the investment horizon by five more years, and the effect becomes even more visible. Over 20 years, the same Rs 5 lakh can grow to around Rs 48.23 lakh, nearly nine times the original investment, underscoring how time, more than anything else, does the heavy lifting in wealth creation.

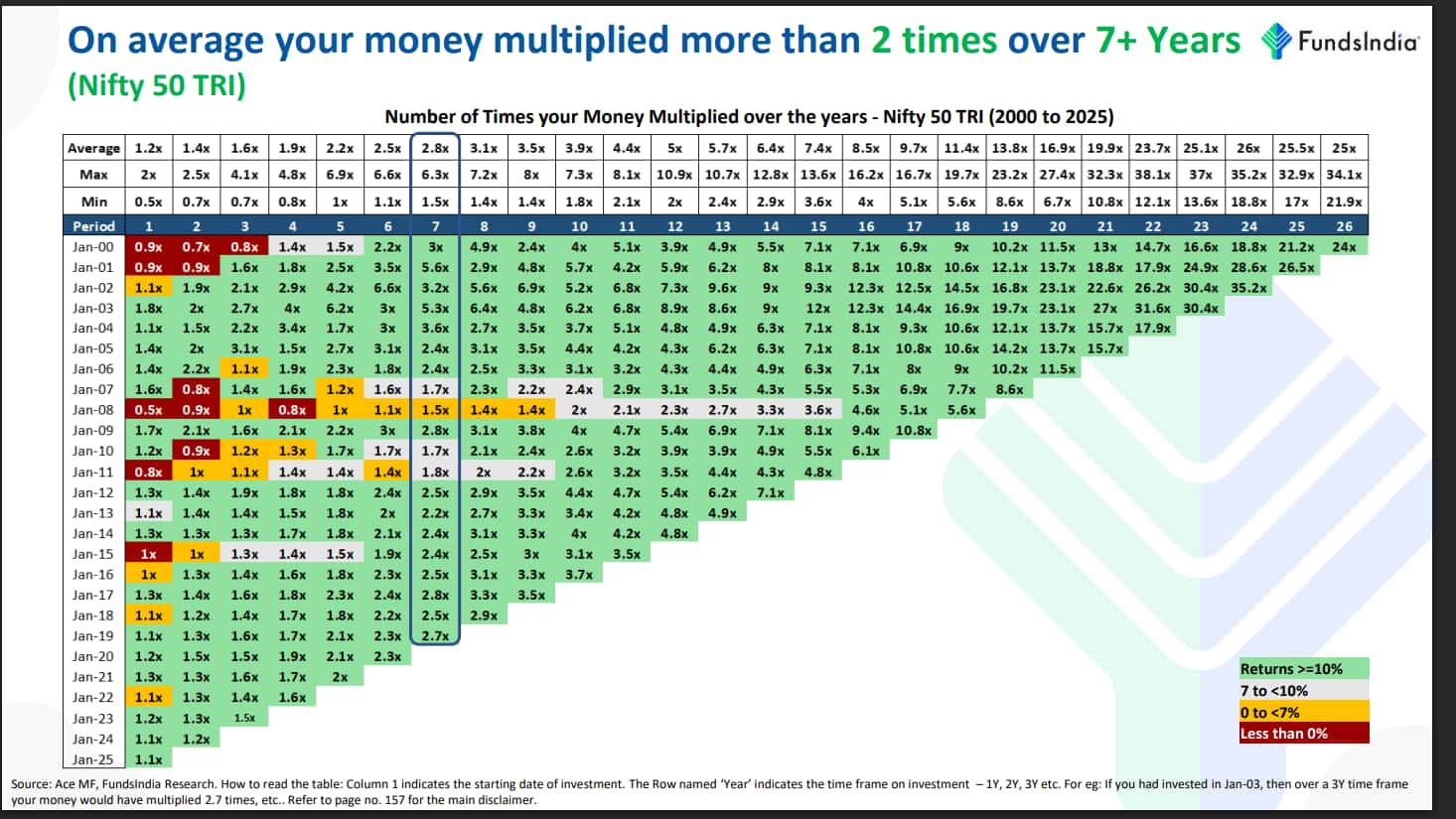

A similar pattern emerges in a recent FundsIndia analysis of Nifty 50 performance since 2000, which shows how strongly time improves outcomes. Investors who started investing in the early 2000s and stayed invested for seven years saw their money grow roughly 2.5–3 times on average, despite multiple market cycles. Even investors who began during volatile years like 2007 or 2008 experienced meaningful recovery and growth when they stayed invested longer. Over time, once holding periods stretched beyond seven years, investments historically more than doubled.

What stands out is how little changes from the investor’s side. There are no additional contributions, no increase in risk, and no improvement in annual returns. Yet, by staying invested for just five extra years, the final corpus rises sharply.

This is the compounding effect at work. Returns generated in the early years begin to earn returns themselves, and over time, this snowballing becomes visible in the final numbers.

Notice what is doing the heavy lifting here. It is not a dramatic jump in returns. It is simply staying invested for longer.

Smaller investments, same compounding power

Long-term wealth creation is often assumed to require a large starting capital. In reality, time can compensate for size.

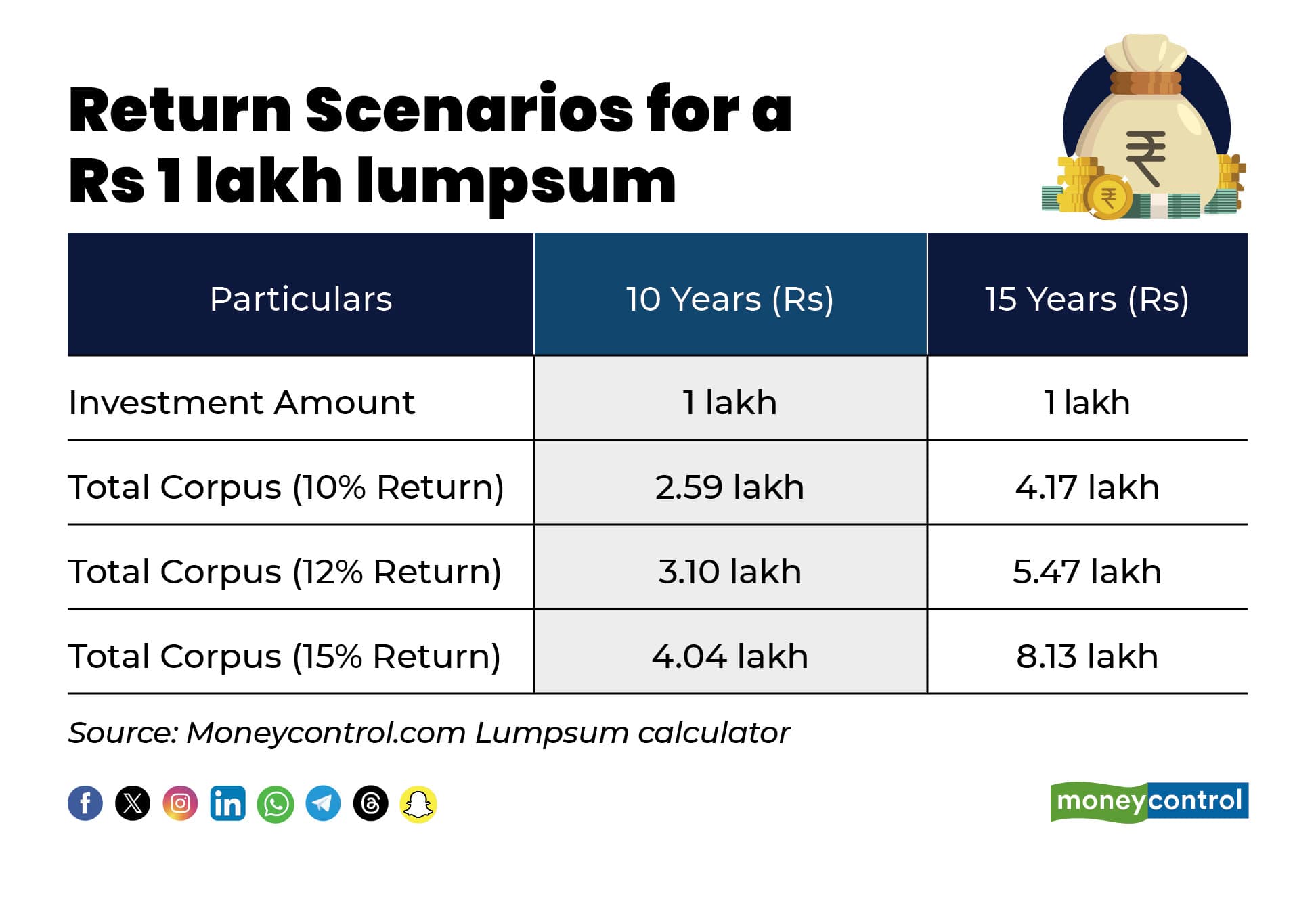

Consider a more modest lump sum investment of Rs 1 lakh. For many urban professionals, this is an amount routinely spent on annual subscriptions, lifestyle upgrades, or EMIs. With conscious saving over time, setting aside Rs 1 lakh as a lump sum investment is far more achievable than it appears.

Neha Chhabra, Assistant Vice President, Avisa Wealth Creators, says, “For many people, consistently saving smaller amounts is not very different from what they already pay towards EMIs. Over long periods, that kind of disciplined investing can still grow into a crore-plus corpus.”

Here is how a Rs 1 lakh lump sum grows over different time frames and return scenarios. Even at a moderate 12% return assumptions, it can grow to over Rs 3 lakh in 10 years. Extending the investment horizon to 15 years lifts the corpus to around Rs 5.5 lakh, purely through the power of compounding.

Bottom Line

The numbers underline a crucial point. The jump in wealth does not come from chasing higher returns alone. Even at the same return level, the additional five years of staying invested materially changes the outcome.

In practical terms, many investors stop or redeem investments once an initial goal appears “good enough.” But extending the holding period often turns a decent outcome into meaningful wealth.

The key takeaway is simple: the difference between stopping at year 10 and continuing till year 15 is often the difference between doing okay and building serious wealth.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.