gave an option to individuals and HUFs to pay taxes at reduced rates, at the cost of letting go of certain exemptions and deductions otherwise available under the old tax regime, including the standard deduction to salaried taxpayers.")

Budget 2023 aimed at bringing sustainable growth, infrastructure investment and a focus on research and development spending. However, the most awaited part of the budget was (as it has always been!) the personal tax proposals. Here are some of the key personal tax proposals and their implications for a salaried taxpayer.

Rejig in the simplified tax regimeAfter the tepid response to the new simplified tax regime over the last two years, in a bid to make it more attractive and widen its coverage, the finance minister has made the following changes in the regime:

The simplified tax regime (STR) gave an option to individuals and HUFs to pay taxes at reduced rates, at the cost of letting go of certain exemptions and deductions otherwise available under the old tax regime, including the standard deduction to salaried taxpayers. It is now proposed to allow taxpayers to claim the standard deduction of up to Rs 50,000 from their salary income and Rs 15,000 from family pension under the STR as well, though certain other deductions and exemptions will continue to be unavailable under the STR.

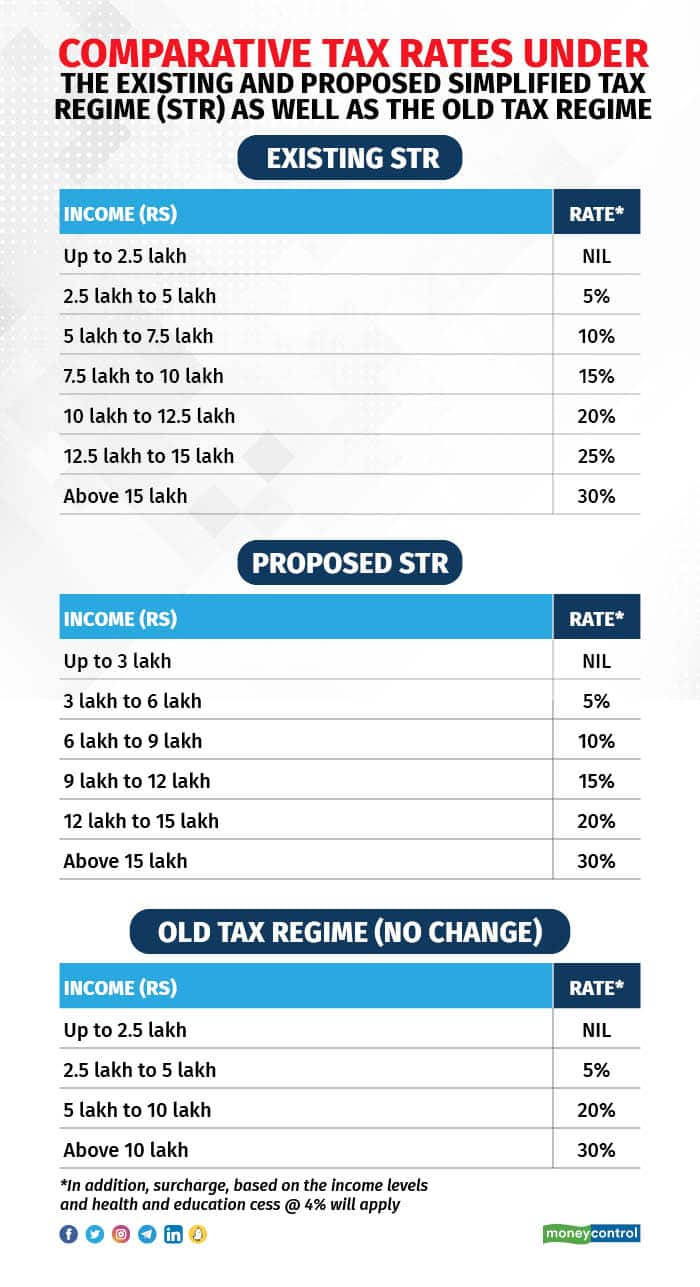

Also read: New income tax slabs, hike in rebate: 5 big personal income tax changes in Budget 2023The budget has proposed to change the tax structure in the STR by reducing the number of slabs from six to five and increasing the basic tax exemption threshold from Rs 2.5 lakh to Rs 3 lakh. Here are the comparative tax rates under the existing and proposed STR as well as the old tax regime:

The rebate under Section 87A of the Income-tax Act, 1961 is proposed to be increased from the existing Rs 12,500 to Rs 25,000 (under STR only), as a result of which there will be no income tax payable by a taxpayer with an income up to Rs 7 lakh under STR. The rebate will continue to be Rs 12,500 under the old tax regime under which individuals with incomes up to Rs 5 lakh do not have to pay tax.

STR shall be the default tax regime for a taxpayer. This means that unless a taxpayer specifically opts for the old tax regime, his or her tax will be calculated as per the STR. A taxpayer will have to exercise this option before the tax filing due date. In the case of a taxpayer who has income from business/profession, the option once exercised will continue to apply (with just one chance to revert to the STR later), but other taxpayers can exercise the option every year.

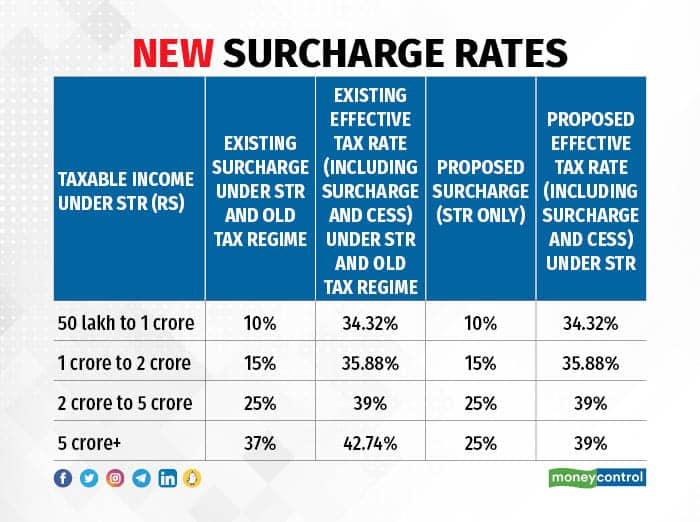

The surcharge for taxpayers with income exceeding Rs 5 crore is proposed to be reduced from 37 percent to 25 percent under STR, bringing some relief to ultra-high net-worth individuals. The new surcharge rates would be as follows:

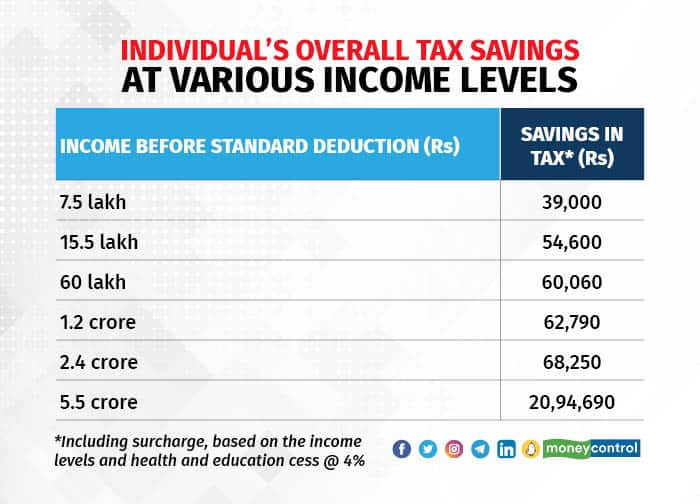

An individual’s overall tax savings (including surcharge and cess) at various income levels under STR as it exists today and as is proposed in the budget will be as below:

The limit for tax exemption on leave encashment on retirement for non-government employees was last fixed in 2002 at Rs 3 lakh. Considering that salaries have increased manifold since then, the budget has proposed to hike the exemption limit from Rs 3 lakh to Rs 25 lakh. This proposal will have to be made effective by way of a notification.

Capital gains exemption cappedSections 54 and 54F of the I-T Act provide for exemption for long-term capital gains on the sale of house property and other long-term capital assets, respectively, upon reinvesting the capital gains/net sale proceeds in either purchasing or constructing a residential house. The exemption that was allowed without any limits is now proposed to be capped at Rs 10 crore.

Proceeds from life insurance policies taxable in certain casesProceeds from unit-linked insurance policies in certain cases were brought under the tax net in Budget 2021. It is now proposed that proceeds from other life insurance policies shall also be taxable where the aggregate premiums paid for all new policies issued on or after April 1, 2023, put together, exceeds Rs 5 lakh in any financial year. The proceeds, net of the premiums paid (not already claimed as deduction under Section 80C) would be taxable under the head income from other sources and the manner to calculate the taxable income shall be prescribed. The only exception here would be proceeds on the death of the insured, in which case the proceeds will be tax-exempt.

Higher TCS on certain foreign remittancesWhile the rate of tax collected at source (TCS) on foreign remittances for education and for medical treatment will continue to be 5 percent for remittances over Rs 7 lakh and the rate of TCS on foreign remittances for education through loans from financial institutions will also continue to be 0.5 percent in excess of Rs 7 lakh, foreign remittances for other purposes under the Liberalised Remittance Scheme (LRS) more than Rs 7 lakh and for overseas tours (without any threshold) will attract an increased rate of TCS of 20 percent instead of 5 percent.

Taxation of online gaming winningsA new scheme of taxation is proposed for winnings from online games under which the net winnings will be taxed at the rate of 30 percent. With effect from July 1, 2023, the net winnings from online games in the user account will be subjected to tax deducted at source (TDS), without any threshold, at the end of the financial year, unless there has been a withdrawal from the user account during the year, in which case, the TDS will be deducted at the time of withdrawal.

(Monil Gangar, Manager and Swapnil Desai, Tax Senior, have contributed to the column).Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.