Have you considered investing in Fixed Maturity Plans (FMPs)? FMPs are close-ended debt mutual funds with a maturity period which could range from one month to five years. These funds usually invest their corpus in highly-rated securities, AAA corporate bonds, certificates of deposits (CDs), commercial papers (CPs), and even bank fixed deposits among others. At a time when interest rates on fixed deposits and other small savings are coming down, FMPs might be a good option for those seeking assured income from their investments.

“FMP invests in securities that are not easily offered to retail investors, which allows individuals to access the unreachable securities. The money collected by FMPs from investors is invested in debt instruments. These include instruments like Non-Convertible Debentures (NCDs), Government Bonds, Highly rated Corporate Bonds, Commercial Papers, Certificates of Deposit, etc. Hence, the risk of loss of capital is relatively lower than that in equity funds,” said Abhinav Angirish- Founder - investonline.in.

Benefit available – Indexation, Lower expense ratio, highly rated bondsIf you are looking for better tax adjusted returns than bank fixed deposits and corporate bonds, you should consider an investments in FMP. It works out to be better due to the indexation benefit.

“While comparing it with the Fixed Deposits, the interest earned is added to the investor’s income and taxed at individual personal income tax rate. Interest from Fixed Deposits is categorized as ‘Income from Other Sources’ under the Income Tax laws. In the case of an FMP, the tax implication depends upon the investment option chosen - Dividend or Growth. But the choice of either of them will still turn out to be better than FD returns due to indexation advantage & ability to invest in securities, which fetch higher returns,” said Angirish.

Indexation benefit is applicable on investments in debt mutual fund schemes where it allows investors to pay tax only on the real or the actual gains over a period of time. The gains are calculated on the basis of cost inflation index (CII) numbers. After calculating the profit component, the gains are taxed at 20 percent. The CII for the years 2017-18 stands at 272.

Adhil Shetty, CEO - BankBazaar.com said that FMPs have a buy-and-hold strategy, and are typically held until maturity. So the expense ratio associated with these instruments are lower (The expense ratio is normally kept below 1% in most of the schemes. However, in some schemes it may get charged between 1% to 2%) as there is no frequent buying and selling of instruments. “The tenors for these instruments range from 3 months to up to 5 years. So, you can choose the tenor suiting your investment objectives and needs,” he said.

To know more about FMPs and Fixed Deposits, you may also read: How fixed deposits and FMPs bolster your retirement portfolio

Be cautious before investing in FMPsFMPs are the closest that mutual funds come to fixed deposits. However, their returns are indicative and not assured. Also, the actual returns can be higher or lower than indicated during the New Fund Offer (NFO). Moreover, FMPs can be tricky as they impose a hard lock-in on your funds, so investors should be very sure that they do not require the designated FMP money for the duration of the investment. Also, they do not always make for compelling investments.

Harsh Gahlaut, CEO – FinEdge said that whether or not it’s a good time to invest into FMPs would depend upon the current yields on AA-rated papers (as that’s where most FMPs invest) as well as the current credit environment. “Presently, with bond yields having gone up and the credit environment improving, investors are likely to see 3-year FMP returns that are very close to 3 year AA YTM’s – which is roughly 8.25% to 8.50%. Given that this is a good 200 bps spread over most FD rates of the same tenure, it may make sense for fixed income investors to allocate some portion of their funds to FMP’s at the moment. Having said that, investors can likely achieve similar or better returns, with higher access to capital, from Credit Opportunities Funds right now. Just make sure you stick with the large AMC’s who have solid risk controls in place,” he said.

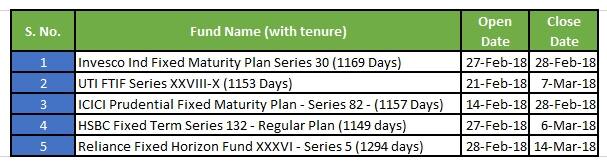

Here are some of the FMPs of the month

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.