Index funds have increasingly become the default suggestion for many investors, especially those who don’t want to spend time picking stocks or chasing fund managers. The logic is simple: choose a broad market index, invest through a low-cost fund that tracks it, and stay invested for the long term. Over time, this approach has worked well enough to build a reputation for index funds as reliable, low-maintenance investment options.

Because of this, investors often assume that once the benchmark is fixed, the outcome should be fairly predictable. So, if two funds are tracking the same index, their returns should more or less look alike, right? But when you start comparing numbers, the picture isn’t perfectly aligned.

Even funds tracking the same benchmark can show small return differences, not dramatic, but consistent enough to catch attention. Two different funds linked to the Nifty 50 reflect this pattern across multiple time frames, hinting that passive investing isn’t entirely frictionless.

And the reason this gap is tracking error, a metric that quietly shapes how closely an index fund mirrors its benchmark.

A subtle but persistent gap

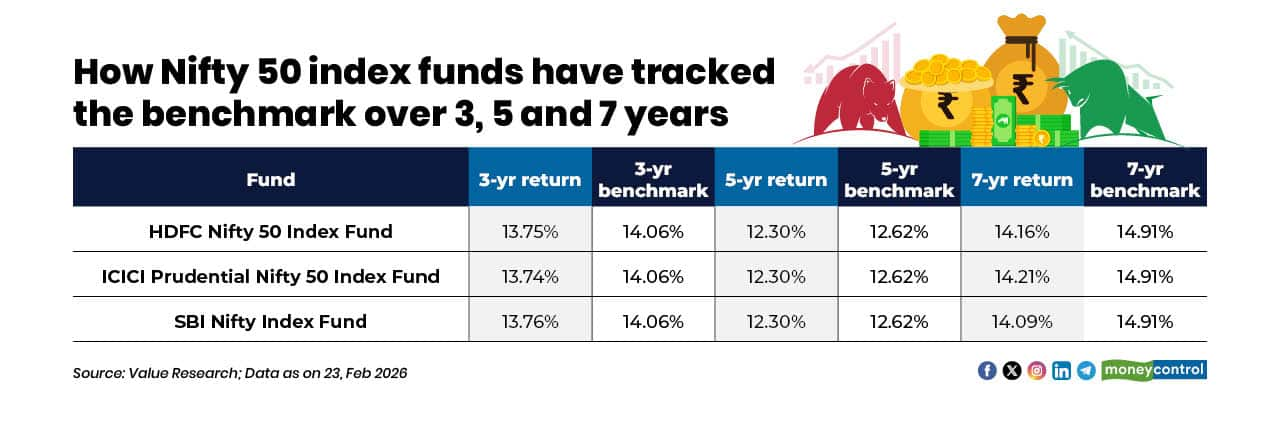

Return data from three popular Nifty 50 index funds, HDFC Nifty 50 Index Fund, ICICI Prudential Nifty 50 Index Fund and SBI Nifty Index Fund, highlights this subtle gap.

Over a three-year period, all three funds delivered returns in the 13.7 percent range, marginally below the benchmark return of 14.06 percent. The pattern continues over five years, where each fund generated about 12.3 percent compared with the index’s 12.62 percent.

Even across a longer seven-year window, the gap persists: the funds posted returns between roughly 14.09 percent and 14.21 percent, while the benchmark stood higher at 14.91 percent.

Seen together, the numbers suggest that while these funds closely mirror the Nifty 50, they don’t replicate it perfectly.

The differences are marginal, but they persist across time periods. This is where the idea of tracking error becomes central to understanding passive fund performance.

How gaps can translate into money

The impact of these frictions becomes clearer in funds tracking broader indices like the Nifty Smallcap 250.

For example, the Nippon India Nifty Smallcap 250 Index Fund delivered 18.54 percent over five years, while the index itself returned 19.56 percent. The percentage gap may not look dramatic, but the corpus impact is tangible.

A Rs 1 lakh investment in the fund would have grown to about Rs 5.47 lakh, compared with roughly Rs 5.96 lakh from the index, a difference of nearly Rs 50,000.

Tracking Error: The quiet driver behind return gaps

Tracking error sits at the centre of why index fund returns don’t perfectly match the benchmark. It reflects how smoothly a fund is able to follow its index in the real world.

Even though index investing is passive, the process of copying an index isn’t friction-free. Funds still operate within practical constraints such as costs, trading realities and portfolio adjustments. These small frictions gradually show up as return differences.

Broadly, three factors tend to drive tracking error:

1) Costs create a steady drag

Every index fund charges an expense ratio, however small. Over time, this cost acts like a mild headwind, which is why fund returns often trail the benchmark slightly. The gap may look negligible in a single year, but it tends to persist across time periods.

2) Cash, flows and rebalancing add short-term deviations

Index funds usually keep a small cash buffer to manage investor inflows, redemptions and expenses. That portion doesn’t move with the market, which can create temporary mismatches. Similarly, when the index changes its constituents or weights, funds need time to rebalance. In fast-moving markets, or in stocks with limited liquidity, this can lead to small slippages.

3) Replication challenges become more visible in broader indices

Not all funds replicate an index in exactly the same way. Some hold every stock in the benchmark, while others use sampling to manage costs and liquidity constraints. This difference is usually less visible in large cap indices but can become more pronounced in wider indices where trading a large basket of smaller stocks is harder and costlier.

Taken together, these factors explain why even well-managed index funds rarely match the benchmark perfectly. In most cases, experts say the gap is not a red flag, it is simply the practical cost of replicating a market index in the real world.

“An index fund cannot copy its benchmark perfectly every day. Small gaps arise from costs, cash buffers for redemptions, rebalancing timing, taxes and whether the fund uses full replication or sampling. While this gap is usually modest in the Nifty 50, it can widen in broader indices like the Nifty Smallcap 250 due to liquidity challenges,” says Kirang Gandhi, a Pune-based financial mentor.

Tracking error vs tracking difference: a quick distinction

These two terms sound similar and are often used interchangeably, but they capture different aspects of index fund performance.

Tracking difference is the simpler concept. It refers to the return gap between a fund and its benchmark over a specific period. If the index delivered 12 percent and the fund returned 11.7 percent, the 0.3 percentage point shortfall is the tracking difference, showing how much the fund lagged or exceeded the index.

Tracking error, in contrast, looks at how consistently that gap behaves over time. A fund may have a small average tracking difference but still show a high tracking error if its deviations vary across periods, sometimes close to the index, sometimes wider.

A useful way to think about it:

For investors, both metrics matter. Tracking difference reflects the actual return impact, while tracking error indicates how smoothly the fund mirrors the index.

What this means for investors

For passive investors, the objective isn’t outperformance, it’s efficient replication. That makes consistency just as important as returns.

A small gap is inevitable and often harmless. But persistently higher deviations can signal structural inefficiencies, particularly in segments where replication is harder.

“Investors should look beyond past returns and review three- to five-year tracking error trends, costs and consistency with the benchmark. Funds with low and stable tracking error, along with lower costs, are generally better choices,” says Gandhi.

In passive investing, small deviations are part of the journey, but funds that keep them predictable can help investors stay closer to the market over time.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.