When we start planning for long-term goals such as retirement, a child’s education or financial independence, we tend to quietly fix a few numbers in our minds.

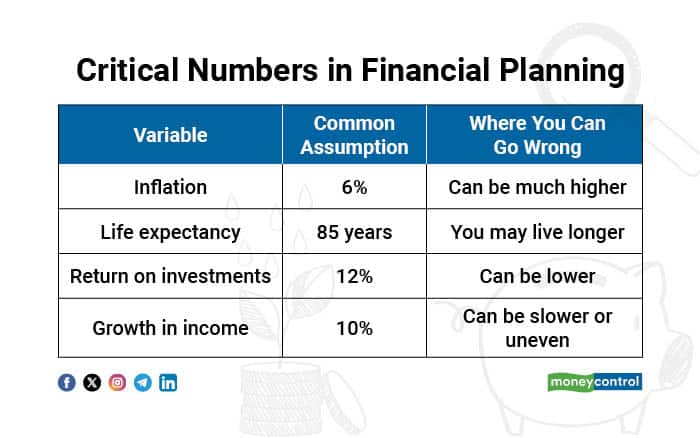

Most financial plans are built around standard assumptions: equity investments are expected to deliver about 12 percent annual returns, inflation is assumed to average around 6 percent, life expectancy is pegged at 85 years, and income is projected to grow at roughly 10 percent every year.

These numbers aren’t random. They are widely used benchmarks in financial planning. The problem is not making assumptions, it’s treating them as certainties rather than educated estimates.

In reality, inflation doesn’t move in straight lines. Markets don’t deliver steady returns. Careers don’t grow predictably. And life expectancy, that’s the one number we almost always underestimate.

And when even one of these numbers goes wrong, the impact compounds quietly over decades, often without us noticing until much later. That’s why, in financial planning, the biggest risk isn’t market volatility. It's a wrong assumption.

What are the 4 Critical Numbers in Financial Planning?

Broadly, there are four numbers that carry the most weight in any financial plan.

Let’s look at each of them and how you can use them more realistically.

1. Inflation: The Quiet Wealth Killer

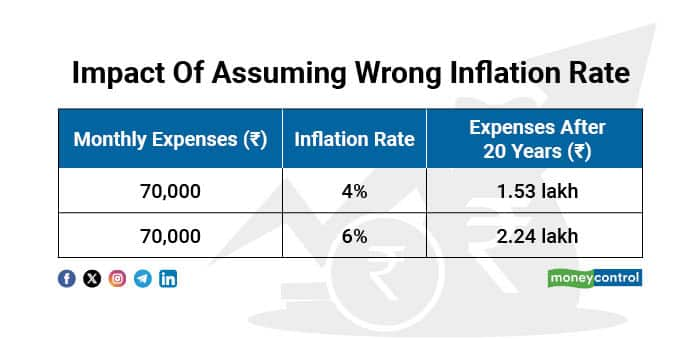

Inflation rarely feels significant in the short term, but over long horizons, its impact compounds. It may not seem like a big deal, but even a 2–3percent difference can completely change the outcome.

For instance, assume current monthly expenses of Rs70,000.

Impact of Wrong Inflation

Impact of Wrong Inflation

At 4percent inflation, Rs 70,000 of monthly expenses grow to about Rs 1.53 lakh after 20 years.

But bump inflation up to 6percent, and the same expenses jump to Rs 2.24 lakh, almost Rs 70,000 extra every month, just because of that 2percent difference. The lifestyle is unchanged. Only the inflation assumption differs.

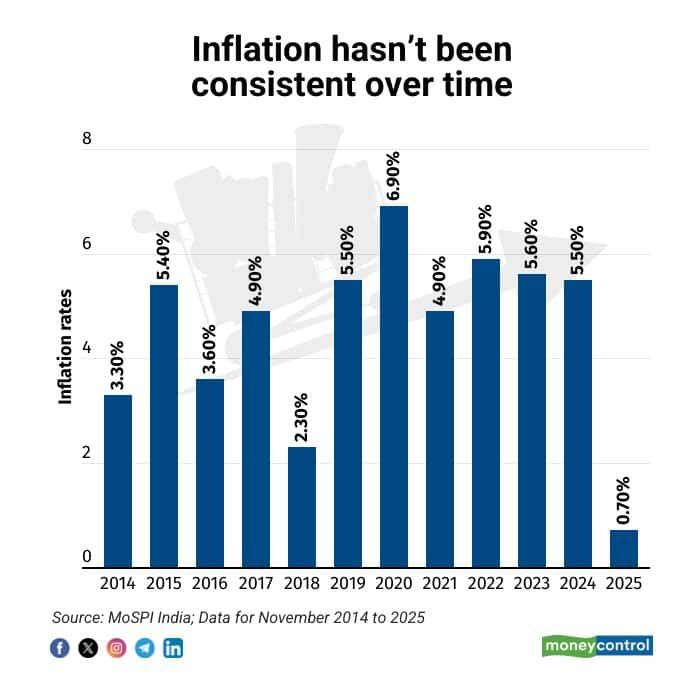

Historically, India’s retail inflation has averaged around 6percent, but it has not been consistent.

Inflation not consistent over long run

Inflation not consistent over long run

For retirement, 6 percent is a reasonable long-term assumption. However, some goals, such as higher education, have historically seen 10-12 percent inflation, making a single inflation rate unsuitable for all goals.

2. Rate of Return: Planning vs Performance

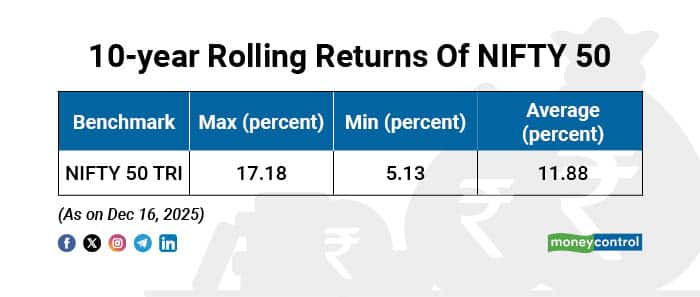

Equities have delivered strong long-term returns. For example, 10-year rolling returns of the NIFTY 50 TRI show:

10-year Rolling Returns

10-year Rolling Returns

While long-term averages are useful, actual portfolios rarely remain fully invested in equities throughout the investment period. As goals approach, asset allocation typically becomes more conservative.

As a result, assuming 11-12 percent returns is often more practical than planning around peak historical averages.

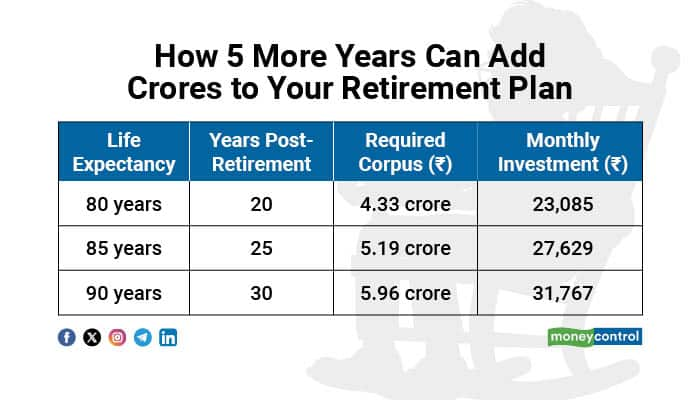

3. Life Expectancy: Duration Risk

Life expectancy directly affects the duration over which retirement savings must last. Every extra year after retirement is another year your money has to last, without a salary backing it.

Here’s what that looks like for someone retiring at 60, with current expenses of Rs50,000 per month.

How 5 more years can add crores to your retirement plan

How 5 more years can add crores to your retirement plan

Assumptions:

Since lifespan cannot be predicted accurately, planning for a slightly longer retirement period reduces the risk of shortfall.

4. Growth in Income: The Least Predictable Variable

Income growth influences savings capacity, but it is rarely linear.

Career changes, industry conditions, and personal choices all affect how income evolves over time.

Most plans assume income grows at 10percent annually. It’s not perfect, but it’s workable.

To arrive at a realistic number:

Being slightly conservative here is better than building a plan that depends on perfect execution.

The Bottom Line

Getting assumptions wrong is normal, but refusing to revisit them is the real risk.

Financial planning isn’t a one-time exercise. It needs to evolve as markets, income, goals, and life change.

Keep in mind, wrong assumptions are riskier than bad markets.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.