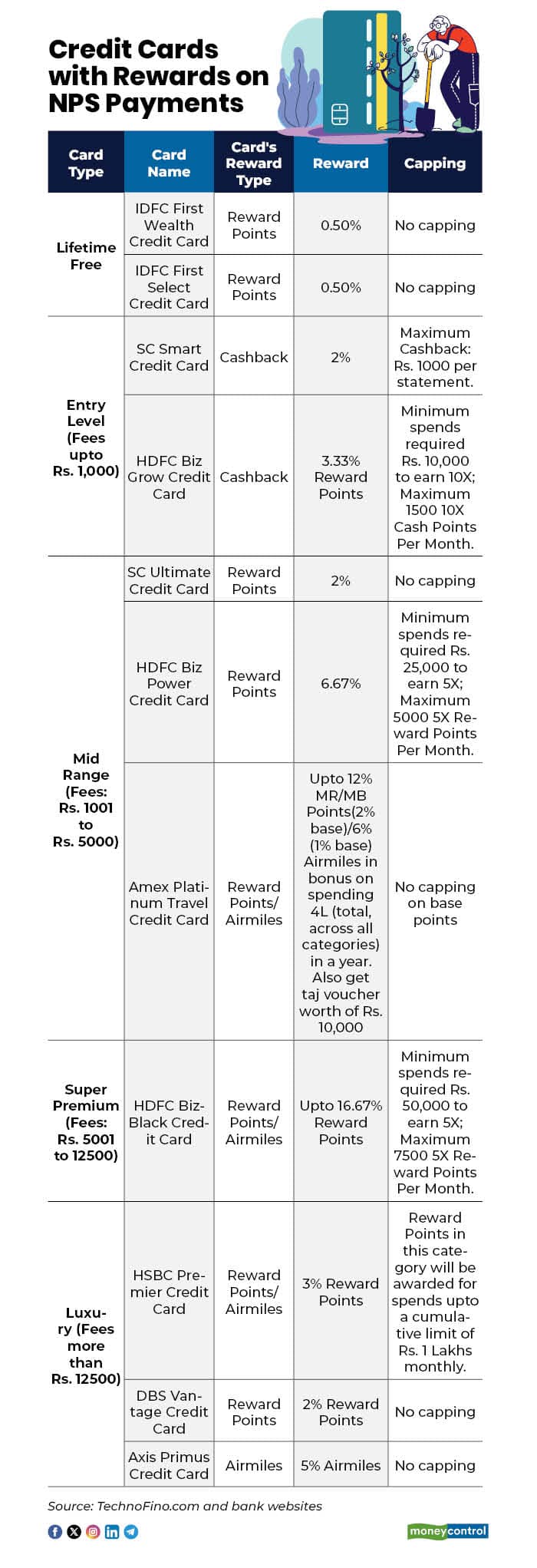

Using a credit card has become second nature for a lot us — swipe, earn reward points and may be unlock a milestone benefit along the way. It is therefore worth examining the option to invest in the National Pension System (NPS) using a credit card. While insurance policies allow premium payments through credit cards but only a few investment products offer this facility.

For many investors, NPS contributions can be substantial, whether through regular monthly investments or large year-end lump sums for tax planning. Routing this spending through a credit card can appear efficient, particularly if it helps earn rewards or meet spending milestones on premium cards.

This growing interest is largely driven by credit cards that offer milestone-based benefits such as bonus points, vouchers or travel rewards once annual spending crosses specific thresholds. For cardholders already optimising their spends, paying for NPS through a credit card may seem like a way to combine long-term retirement investing with short-term rewards.

Whether this works in an investor’s favour depends on costs, card-specific terms and how the card is managed.

Here is what works in favour of using a credit card for NPS

Using a credit card to make NPS contributions can offer some practical conveniences, depending on how the card is used and managed.

While the rewards look attractive at first glance, there are the costs you have to factor in.

Costs investors need to account for

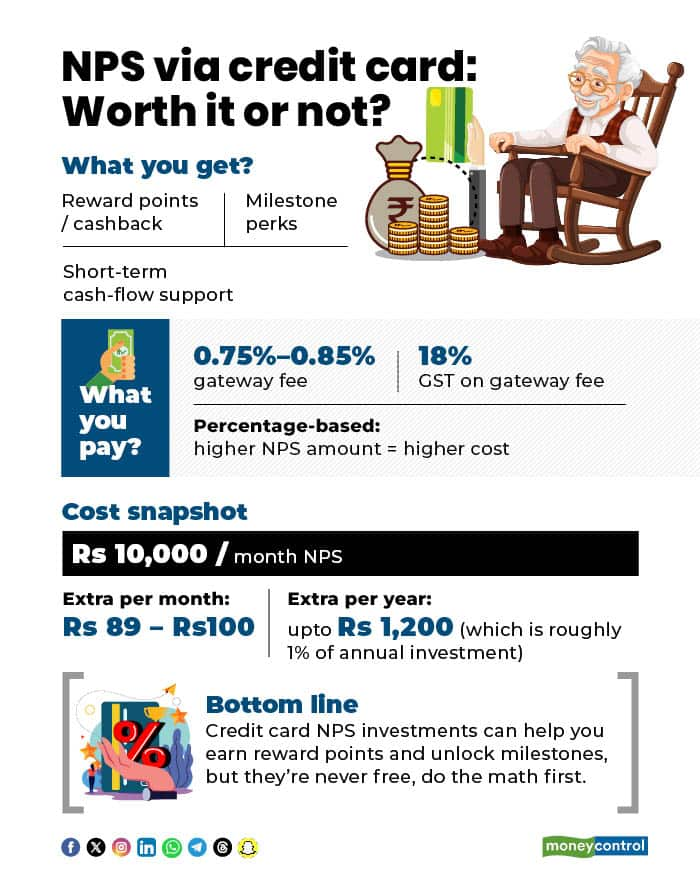

Unlike UPI or net banking, credit card payments for NPS attract payment gateway (PG) charges, which are collected upfront.

Most platforms charge:

Since this is a percentage-based fee, the cost rises with the contribution amount, a detail often overlooked when focusing only on reward points.

Let’s understand with an example of an investor who puts Rs 10,000 a month to NPS (Rs 1.2 lakh a year) using a credit card.

Costs: gateway fee + GST + CRA charge per month: Rs 89 -Rs 100. So instead of Rs 10,000 through credit card you will pay Rs 10,089.

It will lead to an extra annual transaction cost of Rs 1,068-Rs 1,200. That’s roughly 1 percent of the annual contribution, paid purely for using a credit card.

"If your card reliably gives 1.25 percent cashback and there’s no cap/exclusion, cashback on Rs 120,000 works out to Rs 1,500. Against fees of Rs 1,100–1,200, you might barely win (Rs 1,500 − Rs 1,104 = Rs 396 net)," said Vijay Maheshwari, founder of Stocktick Capital.

But that’s optimistic. It assumes issuer credits full reward on these transactions and you can realise full value on redemption. In practice, many users will see lower reward value or no rewards for such transactions, Maheshwari said. Converting points to cash/vouchers often gives Rs 0.20–Rs 0.50 per point or lower effective cashback, that reduces effective benefit.

When does using a credit card for NPS make sense? If your effective reward rate (after converting points to real value) exceeds the total payment gateway fee + GST + per-transaction fee. Example: if your card truly gives >1.2 percent effective back for the spend and the PG fee is 0.75 percent + GST (0.92 percent total), you could net a small positive.

Investors sometimes argue that paying NPS contributions through a credit card creates a short-term “float” benefit, as the money can remain in a savings account until the card bill is due. For example, even if Rs 10,000 is kept in a savings account for 45 days at an interest rate of 2.5 percent per annum and repaid thereafter, the interest earned works out to barely Rs 31.

Where credit cards can fall short

While using your credit card for NPS can get you rewards points, milestone benefits but there are certain downsides to this too.

Is using a credit card for NPS worth considering?

The answer isn’t a straightforward yes or no. Using a credit card for NPS contributions can make sense in certain situations. In limited cases, such as meeting a milestone on a card that clearly rewards NPS payments, it may make tactical sense.

For most investors, however, the payment gateway charges, uncertainty around rewards and the risk of changing card terms reduce the appeal. For those investors, options like UPI, debit card or net banking might work better.

Credit cards can work as an occasional tool but they are not a default or superior way to fund NPS contributions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.