The last date to file your income–tax return for income earned in the financial year 2021-22 (assessment year 2022-23) has passed. But you can still file your tax return in some cases.

For instance, if you have already filed your income tax return, but discovered any mistake or missed reporting any income, you can file a revised return.

If you have not yet filed an income tax return for FY 2021-22, you can file a belated return.

If you want to update your older return you can do that too. But there are penalties and limitations associated with it, so let's read more.

Also read: All you need to know about filing income tax returns

Revised return

If you have already filed your return, but later realised that you made an error, omission or any wrong statement, you should revise the return by filing a revised return within the prescribed time limit.

“This return can be filed three months before the end of the relevant assessment year or before the completion of the assessment, whichever is earlier,” said Deepak Jain, chief executive, TaxManager.in, a tax e-Filing and compliance management portal. This means that for the AY 2022-23 you can file revised returns by December 31, 2022.

There is no limit on the number of times you can revise a return, but remember if the original return has been filed in paper format or manually, then technically it cannot be revised by online mode or electronically.

There is no limit on the number of times you can revise a return, but remember if the original return has been filed in paper format or manually, then technically it cannot be revised by online mode or electronically.

If need be, you can also change the ITR form while revising the tax return. “No penalty can be levied by the department for revising bonafide mistakes. Interest under sections 234B and 234C will be recalculated under every revised return. Before filing the revised return, a taxpayer must ensure that the original return has been verified,” said Yeeshu Sehgal, Head of Tax Markets, AKM Global, a tax and consulting firm.

There is no limit on the number of times you can revise returns, but remember that if the original return had been filed in paper format or manually, then technically it cannot be revised online or electronically.

Also listen: Why you must file your tax returns before July 31

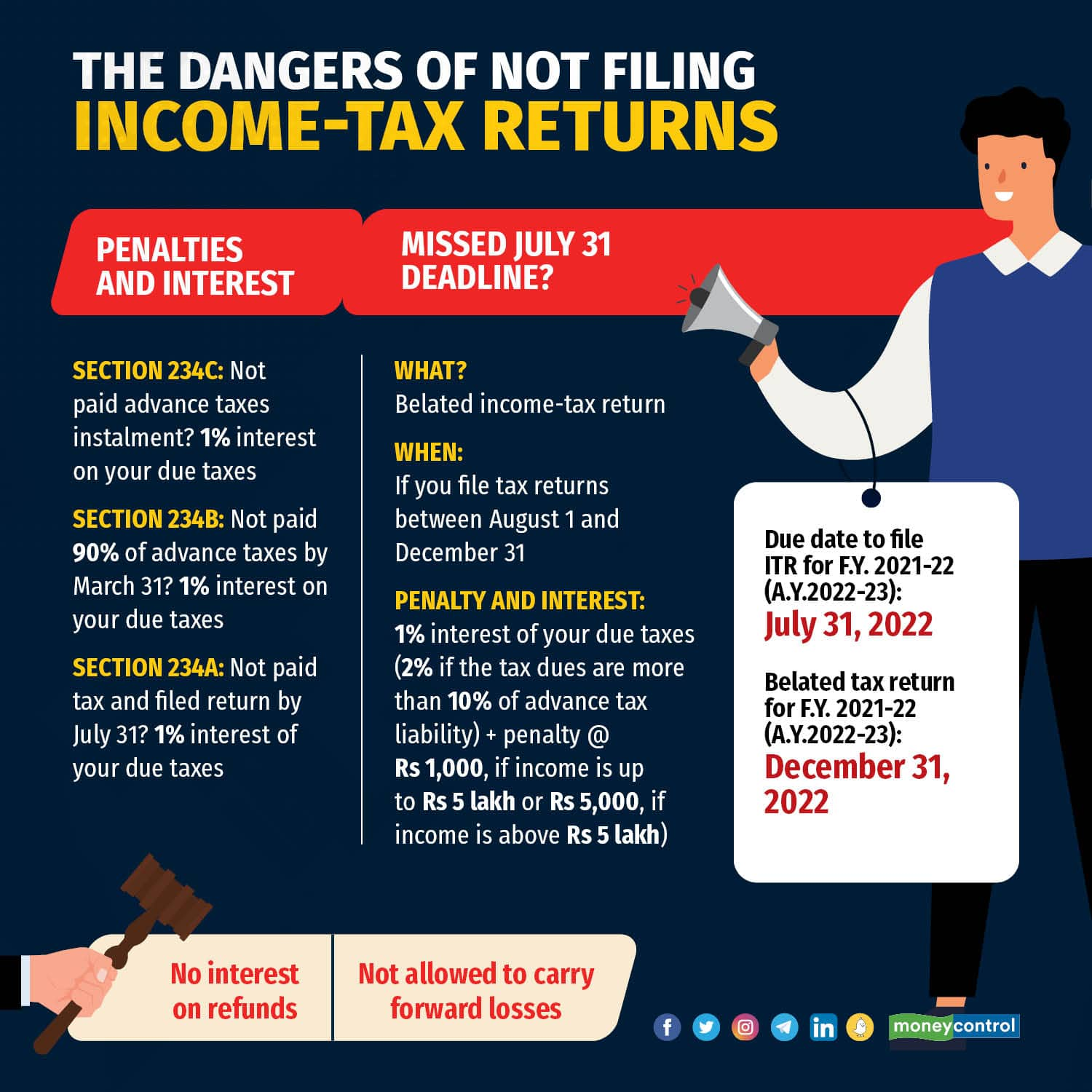

Belated return

A valid return filed within the due dates is called an original return under section 139(1) of the Income-tax Act, 1961. For AY 2022-23 the due date to file your return was July 31, 2022.

“An assessee who does not file his return within the timelines prescribed in the Act but files the return after the due date is referred to as a belated return under section 139(4) of the Act,” said Sehgal.

A belated return can be filed till three months before the end of the relevant assessment year. So, any return filed after July 31, 2022 but before December 31, 2022 for AY 2022-23 will be considered a belated return.

To file a belated return you may need to pay a penalty. As per section 234F, late filing fees of Rs 5,000 need to be paid if a return is furnished after the due date. However, the amount of late filing fees to be paid shall be Rs1,000 if the total income of the person does not exceed Rs 5 lakh.

There will be no late filing fee, even after the due date, in case you are filing a return voluntarily and not required to file an ITR mandatorily. For instance; if your income is below the basic exemption limit i.e. Rs 2.5 lakh for individuals below the age of 60 years, Rs 3 lakh for people between the age of 60 years and 80 years and Rs 5 lakh for those above 80 years, you are not mandatorily required to file an ITR.

In such cases, if you still file a return, even after the due date, you need not to pay any penalty.

Also read: Tax-payers now have 30 days to verify their returns

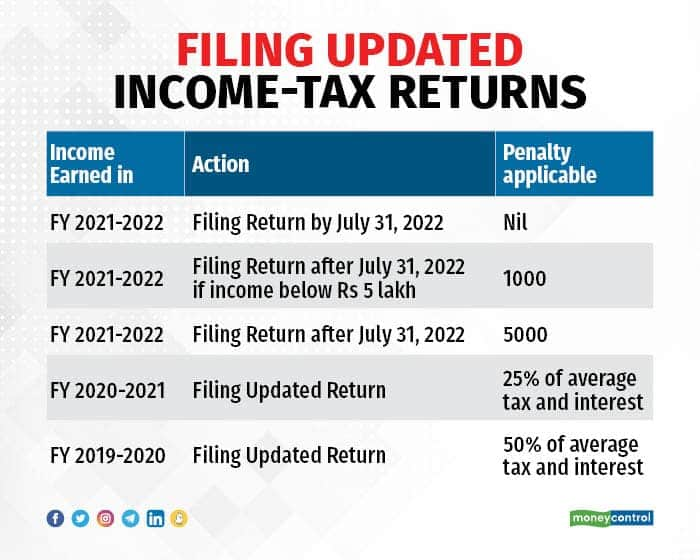

Updated return

The Finance Act 2022, has inserted subsection (8A) in section 139 to enable the filing of an updated return.

The section provides that an updated return can be filed by any person irrespective of the fact whether such a person has already filed the original, belated or revised return for the relevant assessment year or not (subject to certain conditions).

For the purpose of filing updated returns, “The government has introduced a new income tax return-filing facility known as ‘Updated Return’ for the taxpayers who are looking to file the same for FY 2019-20,” said Sehgal.

To file a belated return you may need to pay a penalty. As per section 234F, late filing fees of Rs 5,000 need to be paid if a return is furnished after the due date. However, the amount of late filing fees to be paid shall be Rs1,000 if the total income of the person does not exceed Rs 5 lakh.

To file a belated return you may need to pay a penalty. As per section 234F, late filing fees of Rs 5,000 need to be paid if a return is furnished after the due date. However, the amount of late filing fees to be paid shall be Rs1,000 if the total income of the person does not exceed Rs 5 lakh.

However, to file an updated return, you may need to pay a hefty penalty. “You need to pay the due tax and interest along with an additional 50 percent amount of such tax and interest. For those looking to file for FY 2020-21, the additional amount will be 25 percent of the due tax and interest,” said Sehgal.

Also, remember that an updated return is not allowed to be filed if it is intended to show a lower income or a loss, which you’d like to set off against any gains you may have made in the past, Sehgal explains.

There is a separate ITR form—ITR Form U—for filing an updated income tax return.

You also have to mention the reason behind filing an updated return. Whether you hadn’t filed an income-tax return before, if you wish to report an income that was not reported correctly earlier, if you chose wrong heads of income in the original return that you had filed earlier, whether you’d like to reduce carried-forward losses or unabsorbed depreciation, or you want to reduce the tax credit, or filed the return based on a wrong tax rate, or any others.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.