If you have to file your income tax returns (ITR), it is better to do it in advance rather than wait till the last day.

Last-minute mistakes and e-filing website malfunctions are very common. On June 2, the income-tax department issued an advisory through the official Twitter handle, alerting tax-filers about delays on the income-tax portal. If such delays persist, you could miss the deadline. You could file your tax returns after the due date, but then penalties and interest kick in. Interest kicks in as soon as the financial year (for which you pay taxes) gets done. Also read:

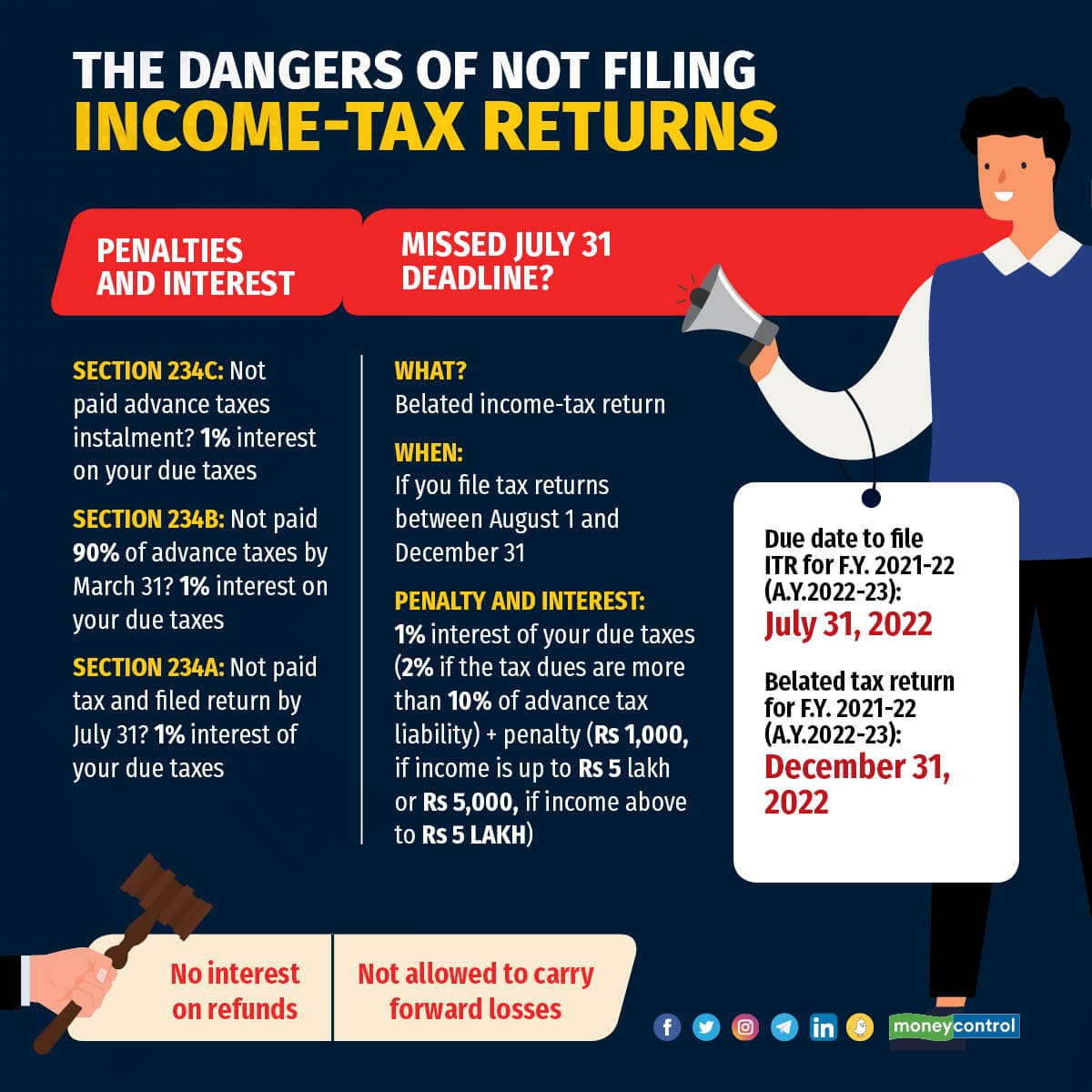

How to select the right ITR formJuly 31, the due date According to Section 139 of the Income-Tax Act, 1961, the due date for filing of tax returns is July 31 of the relevant assessment year for all assesses other than a company, a person whose accounts are required to be audited, and a few others specified in the section. So, for most individuals who had income from salaries, small businesses and professionals, the due date to file ITRs for financial year 2021-22 is July 31, 2022.

1% interest of your due taxes (2% if the tax dues are more than 10% of advance tax liability) + penalty (Rs1,000, if income is up to Rs 5 lakh or Rs5,000, if income above Rs 5 lakh)

1% interest of your due taxes (2% if the tax dues are more than 10% of advance tax liability) + penalty (Rs1,000, if income is up to Rs 5 lakh or Rs5,000, if income above Rs 5 lakh)Belated returns Although the deadline for filing ITRs is July 31, one can still file returns till December 31 of the assessment year (2022-23 at present). But this is called a

belated return. And there are penalties to be paid, in addition to interest. Belated returns can be filed at any time up to three months before the end of the assessment year or before completion of assessment, whichever is earlier. A belated return for 2021-22 can be filed till December 31, 2022, i.e., three months before the assessment year 2022-23 ends on March 31, 2023.

Penalties for belated return However, filing a regular return and filing a belated return are not the same. A penalty of Rs 5,000 will be charged for the delay in filing returns if the total income to be reported exceeds Rs 5 lakh. If the total income of the person is less than Rs 5 lakh, then the fee payable is up to Rs 1,000. After December 31 of the assessment year, one cannot voluntarily file ITRs. After that, if and when the income-tax department picks up your income and tax details available for scrutiny, it’ll tell you what you need to do. Also read:

Getting started with filing I-T returns Verify your Form 26AS and AIS first Penal interest on taxes due Not only does the delay in filing your tax returns attract a penalty, you also have to pay penal interest if income taxes are due from your end. Section 234 of the

Income-Tax Act deals with penal interest that are levied for delays in paying taxes on time. Your interest penalty clock starts to tick from the first instalment of advance tax. Advance taxes based on annual income projections are supposed to be paid in four instalments: June 15, September 15, December 15 and March 15. According to Section 234C, if you fail to pay your

advance taxes in time, you will need to pay a 1 percent penalty every month or part thereof on income-taxes due till you pay out or till the end of the financial year. Once the financial year (in which you earn your income; 2021-22 at present) gets over, you need to start preparing your income-tax returns to be paid by July 31 (the usual deadline date for filing your tax return). The year in which you file your tax returns is called the assessment year. Further, if you have not paid 90 percent of the advance tax due by March 31 of the financial year, the penal interest clock starts ticking under section 234b from April 1 onwards. That is why tax experts say it’s always better to file your return as soon as the assessment year begins (April 1) and not wait till the last minute (July 31).

Depending on when you file your tax returns between April 1 and July 31 of the assessment year, you need to pay 1 percent interest on your tax dues per month or part thereof, as per Section 234b. If you fail to file your return and pay the due taxes by the deadline date (July 31), then you have a chance to file a belated tax return by December 31 of the assessment year.

“Interest (under Section 234A) at 1 percent per month or part thereof (full month’s interest will be charged even if you pay your taxes mid-month) will be charged on the unpaid tax amount. The calculation of interest will start from the date falling immediately after the due date, i.e., July 31, 2022, for AY 2022-23,” said Yeeshu Sehgal, head of tax markets at AKM Global, a tax and consulting firm.

That means from the day after the due date, interest rate implication on due taxes increases.

Story continues below Advertisement

“Interest under Section 234a is in addition to the 1 percent interest (under Section 234b) per month and part thereof if you haven’t been able to file your return within the due date,” said Vikash Mittal, a partner at AGSM Advisory.

So, from August onwards, a total of 2 percent interest (under Sections 234b and 234a) will be charged on due taxes every month and part thereof till you pay the tax and file the return, explained Mittal.

Other disadvantagesBesides penalty and interest, there are other disadvantages of filing a belated return.

In case of filing a belated return, “if the assessee is eligible for a refund, then no interest is given on the refundable amount,” said Deepak Jain, chief executive of TaxManager.in, a tax e-filing and compliance management portal. In other words, there is a price to pay for a belated return, even if eligible for a refund.

Sehgal explains that when one files a belated return, losses cannot be carried forward. This effectively means that no loss under the head ‘capital gain’ or ‘business and profession’ can be carried forward or set off from succeeding years if you do not file returns on time.

Further, “in case an assessee fails to file the belated return, then a taxpayer can receive a notice of inquiry,” said Jain.

Story continues below Advertisement

Given so many disadvantages of missing the due date, it is better to file the return in time.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!