July 13, 2022 / 11:19 IST

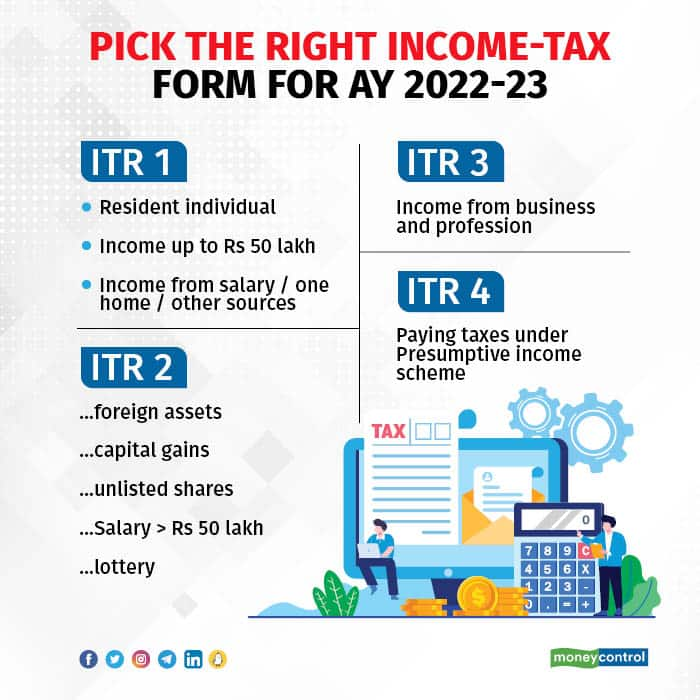

July 31, 2022, the last date for filing income tax return (ITR) for assessment year (AY) 2022-23 (financial year 2021-22), is fast approaching. It makes sense to file your return at the earliest to avoid last-minute mistakes. To start with, you need to select theITR forms based on the source of income, total taxable income, origin of income (domestic or foreign), assets and so on. “The ITR forms for AY 2022-23 have a few but significant changes one need to take note of,” said Aarti Raote, Partner, Deloitte India. Also Read:All about income tax return (ITR) forms for assessment year 2022-23 Here are the changes and the form that will suit you best. The right ITR formOut of the seven forms notified by theCentral Board of Direct Taxes (CBDT), ITR-1 to ITR-4 are the ones that are applicable to individual taxpayers. ITR-1: If you are a salaried individual and your total income for FY 2021-22 was up to Rs 50 lakh. The definition of salary here also includes income in the form of a pension. You can also file a return in ITR-1 if you earn income from other sources like interest from bank deposits and one-house property. Also, if you have agricultural income of up to Rs 5,000, you can use ITR-1. There are a few new disclosures to be made this year while using ITR-1 forms.“The ITR-1 form requires details regarding retirement benefit accounts maintained in notified countries under Section 89A, namely Canada, the United States of America, the United Kingdom of Great Britain and Northern Ireland. This amount needs to be included in the net salary. The form also requires information on income from retirement accounts maintained in other foreign countries,” said Deepak Jain, chief executive, TaxManager.in, a tax e-filing and compliance management portal. These disclosures should be made in ITR-2 forms, too. Also Read:Want a loan or credit card? File your income tax returns first ITR-2: You can use ITR-2 forms to file your return if you have income, including those qualifying for ITR-1 forms, and income from capital gains, income from more than one-house property, foreign income, foreign assets, or if you hold directorship in a company or unlisted equity shares. This year, “there has to be a separate disclosure of interest accrued on provident fund (PF) contribution to the extent taxable. This is because any interest on an employee's contribution to PF over Rs 2.50 lakh shall be taxed at the hands of the employee year after year,” said Yeeshu Sehgal, head of tax markets, AKM Global, a tax and consulting firm. The taxable component is the interest on the excess contribution and not the entire contribution. The excess contribution cannot be taxed twice as the contribution made by the employee is already taxed in the hands of the employee in the first place, added Sehgal.

ITR-3: You can file your return in ITR-3 form if you have income mentioned in ITR-2, and/or have income from a business or profession. You should also use ITR-3 if you are a partner in a firm.“There is now a new field that requires taxpayers to intimate the date of commencement of business. In case of non-residents, the form requires reporting on Significant Economic Presence (SEP) as well,” said Sehgal.Typically, non-residents are also taxed in the countries they live in. However, the SEP rule is meant to establish how deeply the NRI’s business is connected with India.To establish this, the tax department has prescribed revenue and user thresholds for non-residents last year. It says that if you are an NRI doing business from foreign shores, and earn revenues of at least Rs 20 million from sales to Indian persons or at least 3 lakh Indian customers (residing in India), SEP rules will apply. In simple words, you’ve got to pay your taxes here as well.ITR-4: Return on income can be filed in ITR-4 by resident individuals, HUFs and firms (other than LLPs), having a total income up to Rs 50 lakh and having income from business and profession, and if you have opted to file the return under the presumptive taxation scheme.In this year’s form, if you are a pensioner, you have to specify if you are a central or state pensioner. “The new ITR form also seeks some information with respect to concessional tax regime under Section 115BAC for AY 2021-22 and AY 2022-23. It seeks to know whether you have opted for the regime or not or whether you are opting in now, opting out, continuing or not opting,” said Sehgal. From FY2020-21, a taxpayer can choose to pay income-tax under a new optional tax regime. This regime is available for individuals and HUFs with lower tax rates and fewer deductions/exemptions,” he said. Selecting the wrong ITR form“If you select a wrong form, it can lead to non-disclosure of certain sources of income as each form has a purpose,” said Jain. The I-T authorities will consider the return so filed as defective and a notice will be sent to the assessee to file a revised return within 15 days. In case of failure to do so, the return will be treated as invalid, added Jain.”So, make sure you select the right ITR form.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!