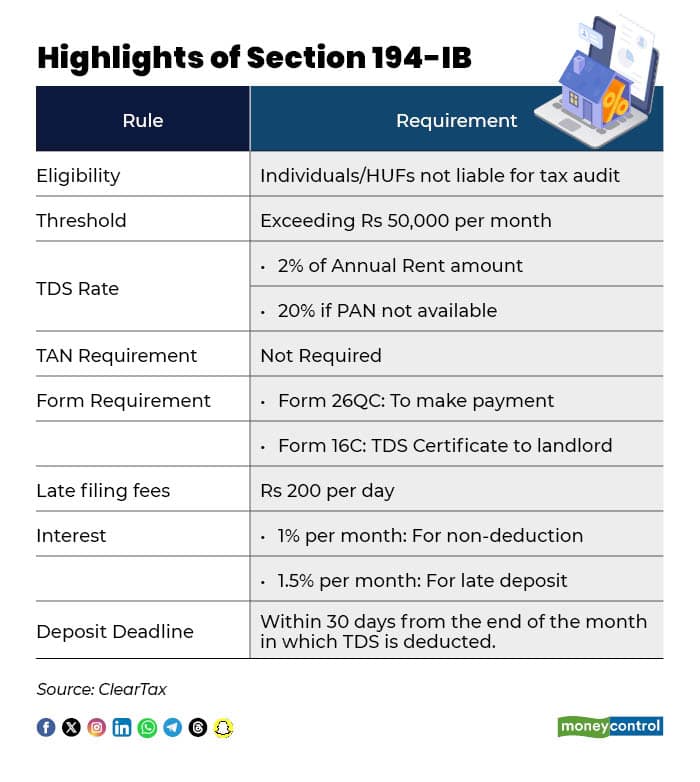

Most salaried tenants assume that TDS deduction is the responsibility of employers alone. However, if you pay rent exceeding Rs 50,000 per month, even for a single month during the financial year, you may also be required to deduct tax at source. Under Section 194-IB of the Income Tax Act, 1961, any individual or Hindu Undivided Family (HUF) paying rent above this threshold to a landlord must deduct TDS before making the payment.

“TDS is required to be deducted at the time of credit of rent for last month of the financial year, i.e., March or the last month of tenancy, if the property is vacated during the year. The deducted TDS must be deposited with the Government within 30 days from the end of the month in which deduction is made. Therefore, TDS deducted in March 2026 is to be deposited by 30th April 2026,” said Gopal Bohra, Partner -Tax, NA Shah Associates.

Understanding the TDS rule

The provision was introduced amid concerns that some individuals were claiming large HRA exemptions while landlords were not reporting the corresponding rental income. To address this mismatch and improve tax compliance, the government introduced Section 194-IB under the Income Tax Act, 1961, in 2017.

What is Section 194IB?

Section 194-IB deals with TDS on rent payments. Under this provision, individuals or Hindu Undivided Families (HUFs) who pay rent exceeding Rs 50,000 per month to a resident landlord are required to deduct tax at source. This requirement applies only to individuals or HUFs who are not subject to tax audit under Section 44AB.

The applicable TDS rate under Section 194-IB was previously 5 per cent if the landlord provided a valid PAN. If the landlord did not furnish a PAN, the TDS rate increased to 20 percent. However, the amount of TDS deducted cannot exceed the rent payable for the last month of the tenancy.

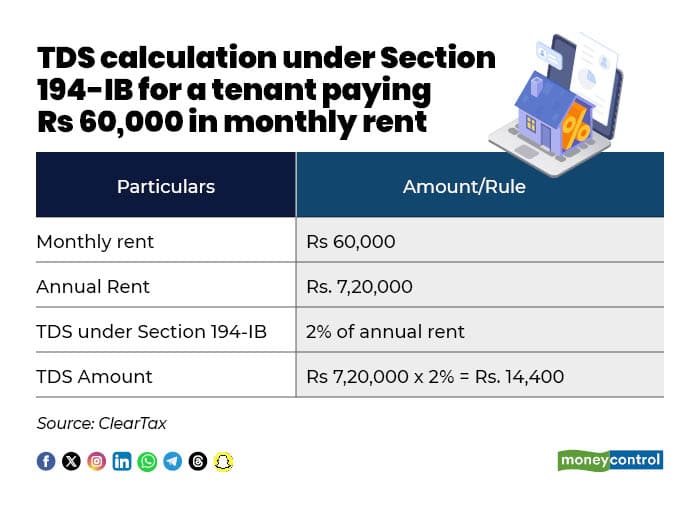

In the Union Budget 2024, the government reduced the TDS rate under Section 194-IB from 5 percent to 2 percent on house rent payments exceeding Rs 50,000 per month. As per the provision, any individual or HUF (other than those covered under the second proviso to Section 194-I) paying rent above this threshold to a resident must deduct tax at source. The revised TDS rate of 2 percent is effective from October 1, 2024.

Failure to comply with these requirements may lead to penalties and interest charges. The tenant may be treated as an ‘assessee in default’ and could face interest charges (1 per cent per month for non-deduction and 1.5 per cent for non-payment after deduction), a late filing fee of Rs 200 per day, and penalties up to Rs 1 lakh under Section 271H for not filing TDS returns. Additionally, the entire tax not deducted may be recovered from the tenant.

“For tenants paying over Rs 50,000 in monthly rent, the compliance process is straightforward. They can deposit the tax using Form 26QC without the need to register for a TAN. This structure encourages individuals to report their transactions accurately and improves transparency in the real estate sector, whilst keeping the paperwork manageable for regular taxpayers,” said Archit Gupta, Founder and CEO of ClearTax.

Process for TDS Payment Under Section 194IB

Once the payment is successfully submitted, save the payment acknowledgement number for your records. You can also download and print Form 26QC for documentation. After the payment, issue Form 16C to the landlord as proof of TDS deduction, which the landlord can use while filing their income tax return.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.