The draft Income-tax Rules, 2026 propose a significant increase in the transaction limits that require mandatory quoting of the Permanent Account Number (PAN). The revised limits would apply to several financial activities, including cash deposits and withdrawals, purchase of motor vehicles and property, as well as payments made for hotel stays and event-related services. The draft, issued for public consultation, is aligned with the upcoming Income Tax Act, 2025, scheduled to come into force next year.

Key PAN related changes proposed under the draft Income-tax Rules, 2026:

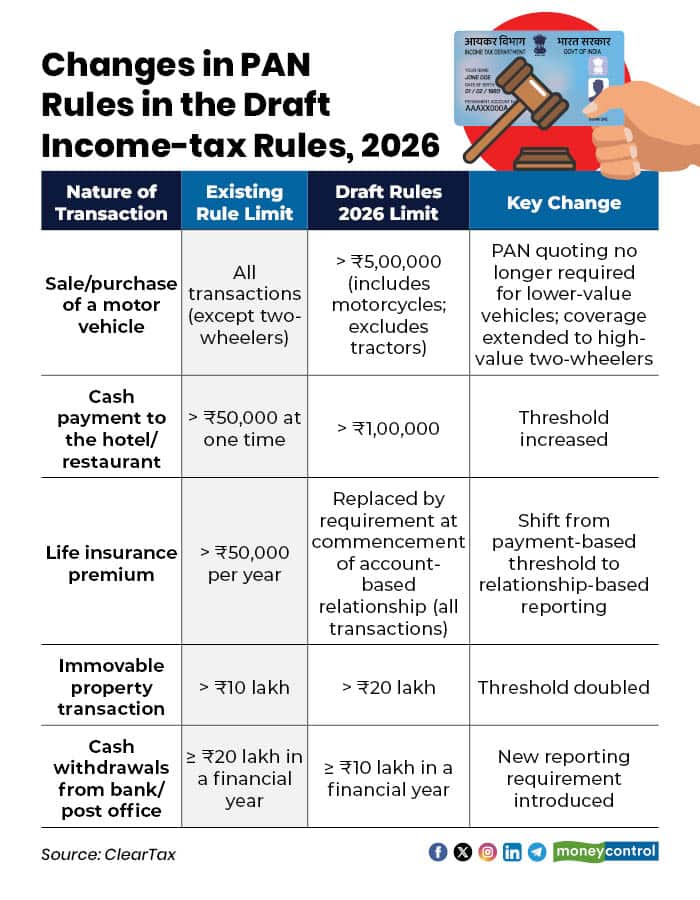

Motor Vehicle Transactions: Under the existing rules, PAN is required for all motor vehicle transactions except two-wheelers. The Draft Income-tax Rules, 2026 propose that PAN will be mandatory only for transactions exceeding Rs 5 lakh, and this will now include high-value motorcycles while excluding tractors. This change reduces compliance for lower-value vehicle purchases and strengthens monitoring of high-value transactions, including premium two-wheelers.

Cash Payments to Hotels/Restaurants: Currently, PAN is required for cash payments exceeding Rs 50,000 at one time. The draft rules increase this threshold to Rs 1 lakh. The move narrows compliance requirements to higher-value spending, ensuring scrutiny is focused on substantial cash transactions rather than routine expenses.

Life Insurance Premium Payments: Earlier, PAN was required if the life insurance premium exceeded Rs 50,000 per year. The draft rules replace this payment-based threshold with a requirement to quote PAN at the commencement of an account-based relationship, covering all related transactions. This marks a shift toward stronger customer identification at the onboarding stage and expands reporting coverage.

Immovable Property Transactions: The current rule mandates PAN quoting for property transactions above Rs 10 lakh. The draft rules double this limit to Rs 20 lakh. This reduces the compliance burden for smaller property deals while maintaining oversight of significant real estate transactions.

Cash Withdrawals from Banks/Post Offices: At present, reporting is required for cash withdrawals of Rs 20 lakh or more in a financial year. The draft rules lower this threshold to Rs 10 lakh annually, introducing a stricter reporting requirement. This measure aims to curb potential tax evasion through large cash withdrawals and strengthen financial transparency.

These major changes may be intended to reduce compliance burden, enable the capture of only relevant information and leverage technology to a great extent.

“Under the Draft Income-tax Rules, 2026, the monetary limits for PAN quoting requirements have been revised across various transactions, including immovable property, vehicles, and cash withdrawals. The revised thresholds indicate a legislative shift toward tighter monitoring of significant and high-risk transactions, alongside a relaxation of compliance obligations for lower-risk activities,” said Chandni Anandan, Tax expert at ClearTax.

However, a few tax experts say that as a cash-based society and low tax base, upward revision of thresholds and leniency will cause more harm than the favour to the exchequer. “For instance, the Income-tax department has unearthed crores of rupees in unreported property transactions by Sub-Registrar offices across Bengaluru during last two-three years alone. To discourage these practices and clamp the revenue loss, hopefully, the final rule will retain most of the current threshold limits,” said Prabhakar K S, Founder & CEO, Shree Tax Chambers, Bangalore.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.