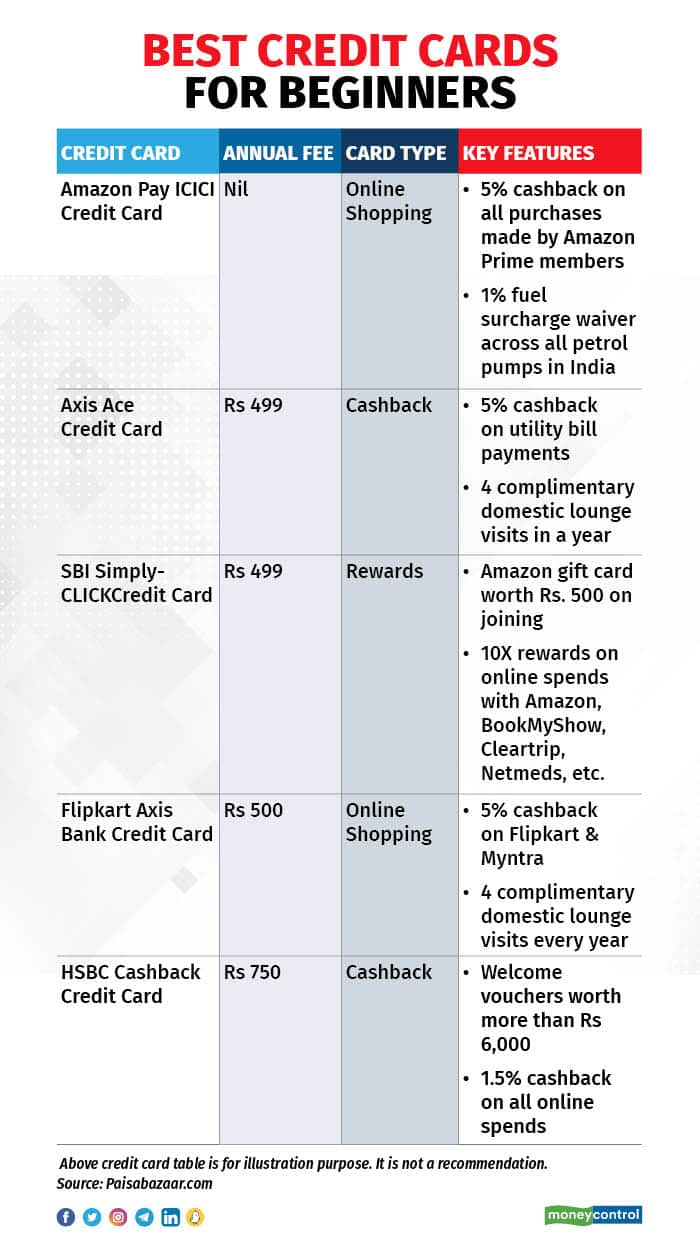

Cash may be king, but there’s no denying that digital transactions have seen a huge jump. And while everyone talks about the increasing usage of mobile wallets, credit cards still remain a popular mode of payment.

According to Reserve Bank of India (RBI) data, there were around 8.03 crore credit cards in circulation in the country as of July 2022. This number has increased 26.5 percent from the end of July 2021.

A credit card allows you to enjoy great discounts, cashback and other good deals. One can also use credit cards in emergency situations as they offer an interest-free period of up to 45 days, and are useful for hassle-free transactions online and offline. Moreover, it can help you to improve your credit score if you spend judiciously and make your full payment before the due date.

But with a plethora of cards catering to varied needs, it becomes difficult to choose the right card. Here we list some of the key things to keep in mind while deciding on a credit card.

There is no single “perfect credit card” that meets everyone's needs. The best way to find the right card will depend on your personal spending patterns and your interest in rewards. It is advisable that you take a step back and understand your reason to opt for a card—this will help you in your decision-making process.

Parijat Garg, a digital lending expert, says that it is important to not put all your eggs in one basket even while opting for cards, so multiple cards across different brands for different needs should be preferred over customisable ones. Keep these pointers in mind.

Travel, shopping, lifestyle… Which card do you need?How are you most likely to use your credit card? Your spending habits matter. For instance, do you travel a lot? In which case, a card that allows you lounge visits or an airline credit card that gets you airline miles on every rupee spent helps.

If you use your credit card a lot for shopping, like buying groceries, a card that gives you frequent cashbacks helps. If you like to dine out regularly, there are cards that help you get good meal offers.

“If your primary expenses are around shopping, you should consider cards that offer cash back, reward rates, benefits on expenses with preferred brands or merchants,” says Sachin Vasudev, director and head of cards at Paisabazaar.

Marketplaces like Paisabazaar, BankBazaar or independent card-evaluation websites can come handy in taking this decision.

Which bank should you opt for?Most commercial banks offer credit cards. To make it easy though, try searching for the right card with your own bank, that is, the bank where you have your savings bank account and have your primary relationship with. “Based on your finances, your own bank is likely to create a preapproved offer for you. Such offers help cut down processing time and paperwork.

You could typically apply for these offers via your bank’s portal or app, or seek them out on a platform,” says Adhil Shetty, CEO, BankBazaar.com.

Experts also say that a well-established bank with multiple cards typically should be among your first choices. “It is not advisable to go for a bank which has only one or two cards right now. The reason is that those banks either are experimenting with their card business or they may be shutting down the cabinets,” says Garg.

There is no publicly available record of the number of credit card products in the market. Rough estimates suggest that on average, a bank has about 20 products. This translates to around anywhere between 200 and 400 credit cards in the market. But there aren’t any estimates on how many of them are free for life and how many entail annual charges.

On the face of it, a lifetime-free card looks better. But that isn’t always the case.

High-end premium cards that come with annual fees can offer more benefits than lifetime-free cards. For instance, the HDFC Diners Club Black credit card offers annual membership to Club Marriott, Forbes, Amazon Prime, Zomato Pro, Times Prime, etc. The cardholder also has unlimited airport lounge access in India and worldwide. Similarly, a State Bank of India Aurum credit card comes with free membership to Amazon Prime, Zomato Pro, Lenskart Gold, Discover Plus, etc. Here too, the cardholder has unlimited international airport lounge access.

The good news is that some high-end, annual fee cards waive your annual fees if you spend a minimum amount a year. Some cards also ask you to tie up a utility bill payment to your card to be eligible for an annual fee waiver.

That said, it’s best for first-timers to stick to cards with no yearly fees.

That’s because most high-end cards have a higher eligibility requirement. In other words, you need to be in a particular income bracket or your application might be rejected. And this is not good for your credit profile.

Understand the chargesThe crucial aspect while comparing the cards across all categories with those of their competitors, apart from the rewards and benefits, are the charges that come along with owning a card. Issuance charges, interest rate charges and annual renewal fees make you weigh the costs and benefits clearly.

On starter cards for first-timers, issuance fees are typically zero. “However, we’re seeing a preference for premium cards which typically cost Rs 499 or upwards. Customers prefer them for the above-average benefits. The annual percentage rate on most cards is upwards of 40 percent. The more premium the card, the more its fees, which could run even into lakhs of rupees in some cases,” says Shetty.

The main thing about credit card usage is settling the dues. Beyond the interest charges and late fees, ballooning credit card debt could hurt your credit score. The more your dues, the greater its negative impact on your credit score.

Know your rewardsCustomers opting for credit cards usually start from here. But this should ideally be the last step of the pyramid.

A welcome voucher of, say, one or two airline tickets or a free one-night stay at a hotel should not be the reason to opt for a particular credit card if it doesn’t align with your spending preferences. Similarly, vouchers that come your way provided you spend a minimum threshold amount—this is typically in the range of Rs 2-5 lakh a year—shouldn’t tempt you to spend more than you can afford.

Compare all cards in your range and make an appropriate choice. It is also important to acquaint yourself with the reward point structure of the cards, which may differ for different cards and banks.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.