For non-resident Indians (NRIs), buying health insurance in India is less about overseas medical cover and more about maintaining financial security back home — be it protecting ageing parents, preparing for an eventual return, or optimising tax liability on income earned in India. Domestic health insurance policies serve multiple purposes, ranging from lower costs, easier claims in India and potential tax deductions, emerging as a financial planning tool for NRIs, not just a medical safeguard.

Health insurance for NRIs

Most NRIs purchase health insurance for their parents residing in India. In contrast, others purchase policies for themselves as part of future return plans, especially those working in Gulf nations, where permanent residency is not assured.

“One key reason is pricing and currency mismatch. Health policies purchased in India are denominated in rupees, while treatment and claims overseas are in local foreign currency, making them less viable,” said Siddharth Singhal, head of health insurance at Policybazaar, an insurance brokerage firm.

Most NRIs prefer to purchase local health insurance policies in the country where they live. Even though a few India-based health plans provide overseas treatment cover, they are generally not practical for NRIs.

“NRIs who spend most of the year overseas, the global plan is not suitable because the probability of needing treatment outside India is much higher and the product is not priced to reflect that risk,” said Singhal.

So, to make health plans more attractive for NRIs, insurers in India have started offering discounts on policies bought for themselves, their families or their parents while keeping the core offering similar to that of Indian residents, subject to policy terms, waiting periods and exclusions.

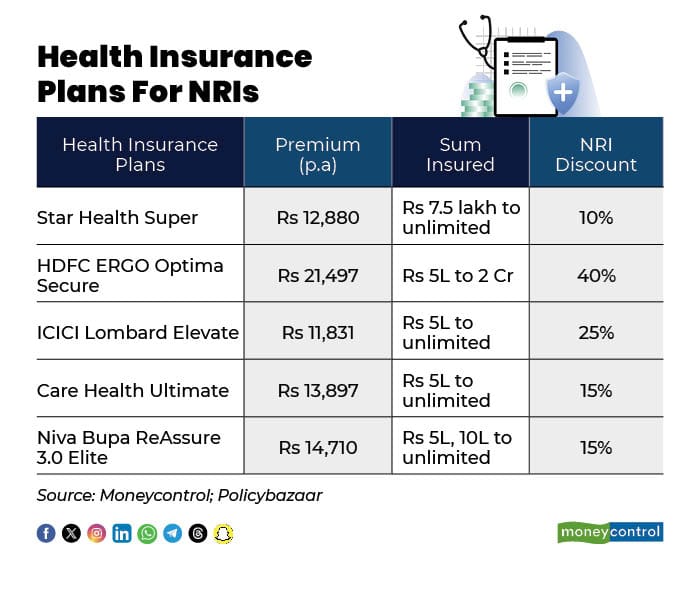

An analysis of five health insurance policies shows that insurers are offering NRI discounts ranging from 10 to 40 percent on select plans, including individual plans, family floater policies, and parent-only coverage.

According to Singhal, insurance companies offer incentives to NRIs because they recognise the distinct profile and behaviour of this customer segment, subject to meeting certain documentation requirements.

The exact eligibility criteria and process vary. Typically, customers must provide proof of NRI status and evidence that the premium is paid from an NRI or NRE account. Based on the insurer’s rules, these discounts may apply to both individual and family floater plans.

“One positive aspect of health insurance for NRIs is that fewer than 0.5 percent of cases require a mandatory medical check-up. Policies are issued based on the customer’s self-declaration or through a simple tele-underwriting call arranged by the insurer,” said Singhal.

Most health insurance plans for NRIs have a standard three-year waiting period, with specific illnesses covered after two years and pre-existing diseases after three years; however, this can be reduced to the 31st day by opting for a rider. Other benefits include two-hour hospitalisation cover, unlimited sum insured restoration, unlimited renewal bonus, day-care procedures, home hospitalisation, and ambulance expenses, to name a few.

If an NRI customer has a history of major hospitalisation and lacks supporting documents, insurers request additional information or medical tests. “Even then, insurers may consider exceptions on a case-by-case basis. Overall, the policy issuance process for NRIs is quite straightforward, especially when purchasing digitally, with minimal procedural requirements,” said Singhal

Deduction valid only against taxable Indian income

One key advantage of purchasing a health insurance policy in India is the availability of tax deductions on premiums paid. Although India’s tax law framework is being reorganised under the Income Tax Act, 2025, the underlying tax benefits for NRIs remain unchanged.

“The benefit currently available under Section 80D has been recodified as Section 126 within the personal tax incentives chapter, with the same policy intent and monetary thresholds continuing for individual, family floater, and parental cover,” said Vipin Upadhyay, Partner at a law firm, King Stubb and Kasiva.

Both residents and NRIs can claim tax deduction of up to Rs 25,000 for health insurance premiums bought for themselves or their family, and up to Rs 50,000 for policies purchased for senior citizens. There’s also an additional tax deduction of Rs 5,000 for preventive health check-ups in a financial year.

Upadhyay said the deduction applies only against income chargeable to tax in India. If a person has no taxable income in India, the deduction cannot be utilised even if the premium is paid, as it can be claimed only against income earned India, such as rent, interest from investments, capital gains, or business income.

Also, NRIs should make the premium payment through permitted banking channels, such as NRE, NRO, or FCNR accounts, or other recognised electronic modes.

Overall, the ITA 2025 framework is expected to create a more transparent, cross-verified ecosystem where tax deductions filed by NRIs are supported by digital evidence. “Insurer reporting, annual information statement (AIS) pre-fill, payment traceability, and PAN-linked disclosures will play a central role in substantiating claims, making documentation and regime selection critical for NRIs going forward,” said Upadhyay.

The analyst reminds NRIs to be mindful of the default new tax regime, under which such deductions are not available unless they specifically opt for the old regime when filing their returns.

Claiming health insurance tax deductions — on income from rent, interest, capital gains, or business income — is relevant for NRIs only if they choose the old tax regime. The new regime offers lower slab rates but most common deductions and exemptions, including Section 80D for health insurance, are generally not available.

“On the procedural side, NRIs will continue to file returns in ITR-2 or ITR-3, depending on the nature of their Indian income, and must retain premium receipts, policy documents, and proof of payment for verification,” Upadhyay said.

NRIs can use ITR-2 if they earn income from salary, rent, capital gains, or other sources but have no business or professional income. ITR-3 is applicable if they also earn income from a business or profession in India.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.