The Income Tax Act, 2025, is scheduled to be implemented from April 1, 2026, onwards, and there’s already a growing curiosity among taxpayers on how flexibly the provisions will apply once the new rules replace the Income Tax Act, 1961.

This is because the government has renumbered most sections under the Income Tax Act (ITA), 2025, without materially changing the core philosophy of the current Income Tax Act, 1961.

The Central Board of Direct Taxes also published a draft of the Income Tax Rules, 2026, on February 7, reorganising sections under 333 rules and 190 forms while laying out the blueprint for implementing the ITA 2025.

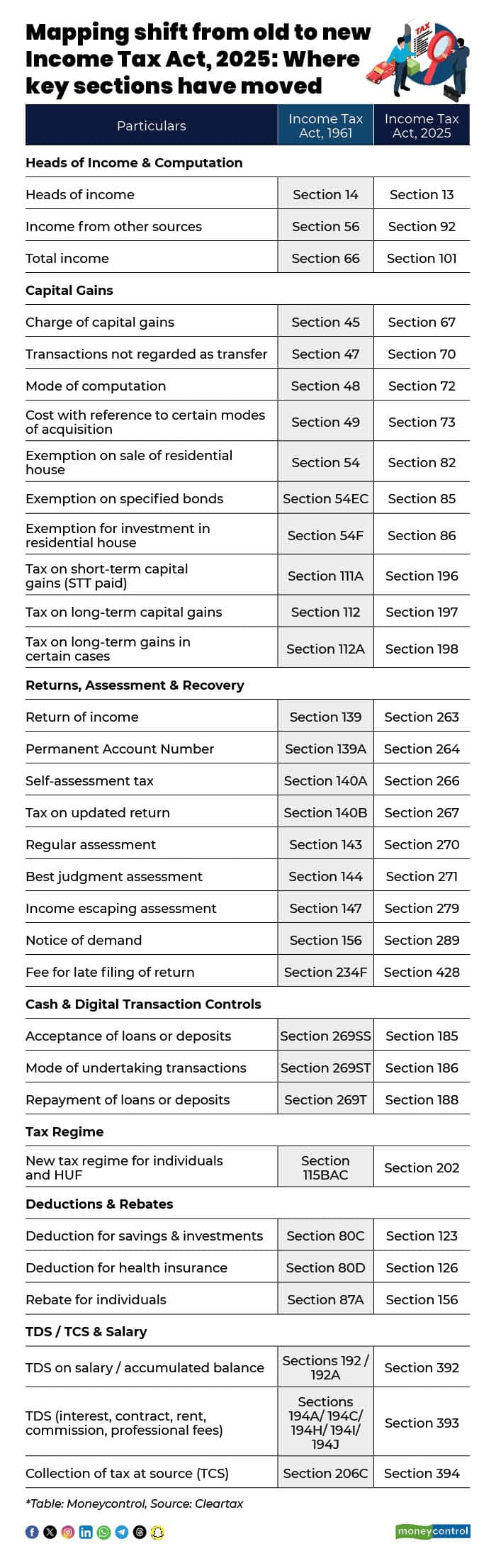

Transition of sections from the Income Tax Act, 1961, to the Income-tax Act, 2025

The new rules will replace the 511 rules and 399 forms of the Income-tax Rules, 1962. The draft rules have also suggested a framework for ITR (Income Tax Returns) forms under the new rules.

"The Income Tax Act 2025 has reduced the number of sections in the act, simplified the provisions, and ensured a better flow of the sections as compared to the existing Income Tax Act 1961, " said CA Chandni Anandan, Tax Expert at ClearTax.

Here’s how key personal finance sections for taxpayers transition from the existing law to the new framework under the Income-tax Act, 2025.

ITA 2025: Rental income rules for landlords and second-home owners

Further analysis of the chart shows that changes in numbering apply to most sections simultaneously. The ‘Income from House Property’ that applied to Sections 22, 23, and 24 of ITA 1961 will be dealt with under Sections 20, 21, and 22 of ITA 2025.

“The core framework governing income from house property, currently under Sections 22 to 24 of the Income-tax Act, 1961, has been substantively carried forward in the corresponding chapter of the proposed Income-tax Bill, 2026,” said Aditya Bhattacharya, Partner at King Stubb & Kasiva Advocates and Attorneys.

Likewise, ‘Determination of the annual value of the property’ that applies to ITA 1961 Section 23 will be dealt with under ITA 2025 Section 21. Similarly, numbering has changed from Section 24 to Section 22 for deductions on income from house property.

Thereafter, ‘Return on Income’ from such property per se, which will apply under Section 263 of the ITA 2025 (replacing Sections 139 and 285BA of the ITA 1961), will be subject to enhanced reporting, data integration, and provisions relating to tax return filing and information reporting.

“Overall, rental income is expected to be under closer scrutiny. The proposed law marks a clear shift towards stricter taxation and higher scrutiny of rental income, while retaining familiar classification principles. Rental income is no longer viewed as a passive stream but as a regular, traceable source of income, backed by improved data matching,” said Bhattacharya.

This would essentially require landlords and second-home owners to reassess property use, financing and disclosures to remain compliant.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to consult certified experts before making any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.