In a lifespan, you may borrow from Banks, a Non-Banking Financial Company (NBFCs) or Fintech companies for various reasons which includes while buying a home or car, for higher studies (education), to set-up or expand a business, loan against property or gold, personal loans for various reasons, etc.

These loan products are offered on fixed interest rate and floating interest rates by both the banks i.e. private and public sector banks. Due to this given interest rates option from lenders, often borrowers are in a dilemma whether to apply for a loan that has a fixed interest rate or floating interest rate. Let’s understand both the interest rates and which one suits you in through examples and theory.

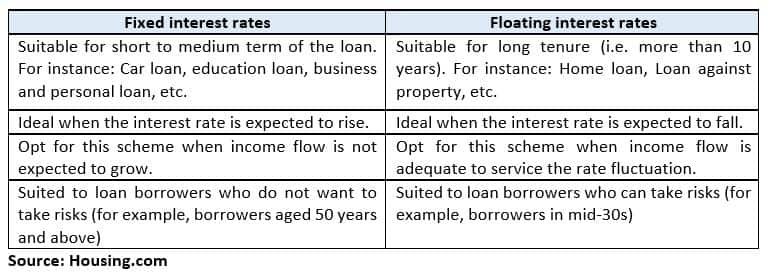

What is a fixed interest rate? In fixed interest rates, you will repay loans at a fixed percentage in equal instalments over the entire tenure of the loan.

Mumbai-based tax and investment professional Balwant Jain said, “Opting for fixed interest rate loan gives you a shield against interest rate fluctuations.”

For instance, if the interest rate cycle is expected to rise for the next few years, it’s recommended to lock a fixed interest rate on your loan.

However, it’s important to read the terms and conditions while applying for a fixed interest loan because some of the banks have a reset clause to decide on interest rates after servicing a loan for few years or convert fixed interest rate loan to floating interest rate loan scheme.

For instance, a bank is offering a 2-year fixed rate home loan at 8.5-8.55% for up to Rs 30 lakh. You took a loan in October 2018 for Rs 25 lakh. It has a reset clause of interest rate every 2 years in your agreement.

So, in October 2020 your loan linked to the marginal cost of funds-based lending rate (MCLR) will get reset or might get converted to floating interest rate depending on the clause.

Pros Interest rate remains constant throughout the tenure of the loan so you can precisely budget outflow for a loan from annual income.

Drawback

The major drawback is in case the interest rate cycle goes down during the tenure of the loan, you will not get the benefit of reduced interest rates as banks will not change the fixed interest rate you servicing on loan.

What is a floating interest rate? In floating interest rate loan, the interest rate varies with the market / economic scenarios. The floating rate loan is tied to a marginal cost of funds-based lending rate at present. So, if the MCLR changes, the floating rate also fluctuates.

Pros

The main benefit of floating rate loans are that they are slightly cheaper (approximately 1-2%) than fixed interest rates.

Amit Prakash Singh, Principal Partner-Mortgages of real estate advisory services, Square Yards said, “Even if the floating rate exceeds the fixed rate, it will be for some period of the loan and not for the entire tenure. The interest rates will surely fall over a long period and thus floating interest rates bring a lot of savings.”

Drawback

The major drawback of a floating interest rate is uneven nature of monthly instalments throughout the loan tenure which makes financial planning difficult.

Floating interest rates to change for all retail loans From April 2019, interest rates on all retail loans, including home loans and auto loans will be linked to external benchmarks, and not the MCLR.

The new framework from Reserve Bank of India will make loan pricing more transparent but this may also mean more volatility in borrower's equated monthly instalments (EMI). The final guidelines are expected soon from the central bank.

Bottom line

To conclude, picking the type of interest rate is a personal choice considering the risks and advantages. It differs for individuals considering what suits them.

Navin Chandani, Chief Business Development Officer, BankBazaar.com suggested, “If you prefer to plan well ahead when it comes to your finances and not leave anything to external factors, a fixed rate would be better suited to your needs. This, however, comes with a higher price.”

So, before you make a decision, you must compare loan schemes with fixed and floating interest rates from different financial institutions. Understand the terms and conditions of the scheme then choose which suits best.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.