A Rs 1-crore health insurance cover might seem excessive today but financial experts argue that the real risk is being underinsured. As medical costs soar, the focus shifts from immediate hospital bills to expenses that may arise years later.

"When I suggest a Rs 1-crore health insurance cover to clients, I often get the same look, a mix of surprise and mild disbelief. 'That seems like a lot,' they say. And honestly, 10 years ago, I might have agreed. But we are no longer living in that decade, and more importantly, we will not be living in this one either when it matters most," said Arijit Sen, qualified personal finance professional practitioner.

Health insurance isn't just about the current cost of hospital stays. It's about what it will cost when you truly need it.

India's medical inflation has consistently run at 12–15 percent a year, roughly two to three times the general consumer price inflation. This means healthcare costs are doubling approximately every five to six years.

"A procedure that costs Rs 5 lakh today will likely cost Rs 10 lakh by 2030 and close to Rs 20 lakh by 2035. This is not a theoretical projection, it is already playing out in hospitals around us. Rising costs of technology, specialist fees, diagnostics, imported drugs, and post-surgical care are all compounding. Your Rs 5 lakh cover from 2016 is not the same Rs 5 lakh cover in 2026," Sen said.

A critical illness or a complicated surgery at a top private hospital runs into the tens of lakhs. A prolonged ICU stay, cancer treatment, organ transplant or advanced cardiac procedure can push the bill well beyond Rs 10 lakh. Medical inflation has consistently stayed in double digits, and treatment costs in large cities have surged even faster.

Priya Deshmukh, head, health products, operations and services, ICICI Lombard, said, "In metros, a prolonged cardiac event or severe infection requiring ICU/ventilator support can also exhaust lower covers quickly, while a Rs 1 crore floater safeguards against concurrent claims across family members. Such coverage lets customers focus on the right treatment and hospital, without compromising care due to coverage limits.”

For several households, a Rs 1-crore health cover is no longer about an expensive demand; it is about protecting long-term savings from a single medical emergency.

Sarita Joshi, Head of Health and Life Insurance at Probus, said, "For anyone questioning whether a Rs 1 crore cover is too much, a glance at the bills from private hospitals in metro cities today can be quite revealing. A decade ago, Rs 5 lakh was the gold standard; now a single complex surgery or a week in the ICU can wipe that out before you even process the diagnosis."

Joshi said with medical inflation in India the highest in Asia, buying insurance is future-proofing for a major ailment 10 years down the line.

"What I love about these high-sum insured plans is the 'value for money' aspect. Moving from a Rs 10 lakh cover to a Rs 1 crore cover doesn’t cost 10x the premium; in fact, it usually only costs about 20-30 percent more," she said.

Insurance Brokers Association of India (IBAI) president Narendra Bharindwal said a Rs 1-crore policy makes sense , particularly for urban families, but the decision should be based on individual risk profile rather than a headline number. For families living in large cities or those seeking treatment at top private hospitals, higher coverage provides an important financial safety net, he said.

How to buy such a big cover?

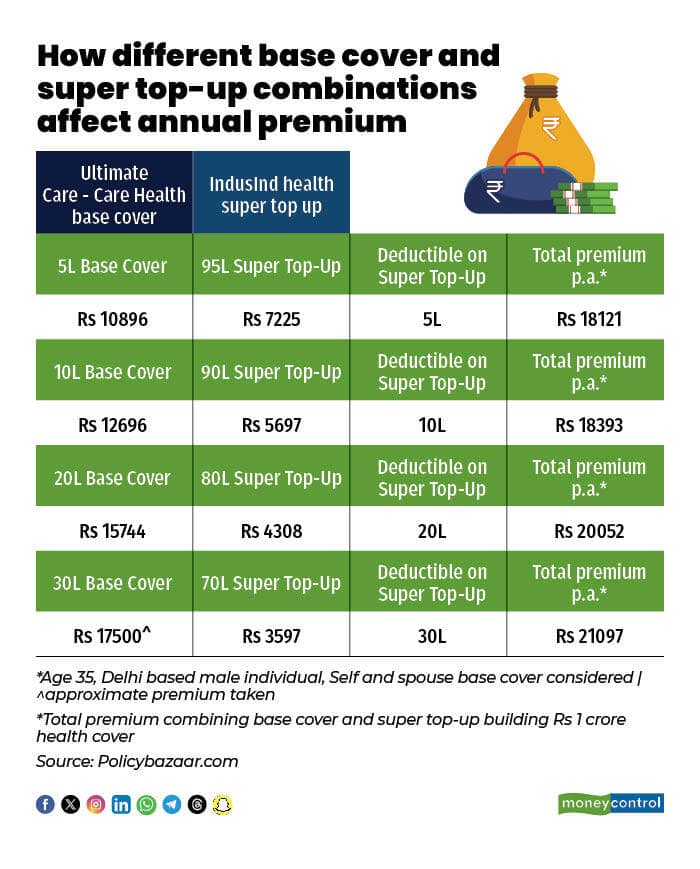

It is important to buy such a high-value policy intelligently. One practical approach is to combine a reasonable base cover, say Rs 10 lakh or Rs 20 lakh, with a large super top-up plan that activates once the base cover is exhausted.

"The affordability and sustainability of premiums are equally important. Instead of directly opting for a Rs 1 crore base cover, you may consider a balanced structure, such as a base policy of Rs 10 to 25 lakh supplemented by a super top-up cover. This approach provides high protection at a reasonable cost while ensuring long-term coverage continuity. Ultimately, adequate coverage should align with lifestyle, location, age, and family medical history," said Bharindwal.

This structure allows policyholders to build a Rs 1 crore protection shield at a lower premium, while ensuring that a catastrophic medical bill does not wipe out years of savings. Premiums are affordable with such a combination.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.