Highlights: - Manufacturer of aluminium fluoride, a critical raw material for aluminium - Aluminium fluoride prices have been rising due to stricter environment norms in China - The company benefits from a production process that is not dependent on China - 60 percent capacity expansion next fiscal to aid volume growth - Stock trading at attractive valuation multiples -------------------------------------------------

Alufluoride is a small cap manufacturer of a critical raw material, aluminium fluoride, required for aluminium production. Its strategic advantages in its production process, raw material sourcing and a favourable demand-supply balance that helps its pricing make it an interesting investment.

Production process not dependent on China The unique proposition of the company is its production route for aluminium fluoride. There are two ways of producing aluminium fluoride. The first method, which accounts for 80 percent of the world’s production, requires processing natural raw material resources such as fluorspar and sulphur. Fluorspar is mostly sourced from China, where, due to stricter compliance with environmental norms, supply has reduced. The upshot: it’s reported that fluorspar prices have increased by 40 percent year-on-year.

In the other method, which is followed by Alufluoride, aluminium fluoride is sourced from a byproduct of phosphoric fertiliser plants. So this process is not dependent on the China factor and the adverse supply demand dynamics that have led to the rise in fluorspar prices. That’s a big advantage.

New contract cycle is the key trigger Globally there is a supply constraint for aluminium fluoride, not only because of lower fluorspar availability but also due to the ongoing supply side reform’s impact on the entire aluminium fluoride value chain in China. That is why aluminium fluoride prices are going up. That gives aluminium fluoride producers an opportunity.

The management is sanguine about the new contract cycle which is on the verge getting closed. Current pricing levels suggest new contracts can be agreed at about a 15 percent higher price.

Capacity expansion on track The company is on track with its capacity expansion plan of 4,500 tonne (vs. current capacity of 7,500 tonne) expected to be ready by the second quarter of FY20.

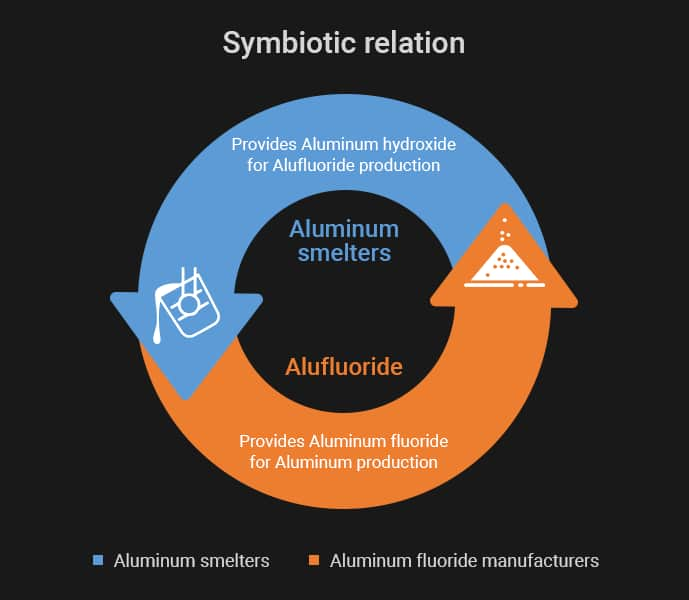

New linkages for key raw material underway The company depends on two key raw materials: alumina hydroxide and hydrofluosilicic acid. The former has been a key drag on the recent Q3 operating performance.

Aluminium hydroxide is produced by aluminium smelters and is in turn further used in the value chain of aluminium production. Interestingly, this means that higher demand for aluminium leads to lower availability of residual aluminium hydroxide for aluminium fluoride manufacturers.

Source: Moneycontrol Research

To mitigate this, the company is developing linkages with aluminium smelters such as Emirates Global Aluminium to ensure the supply of aluminium hydroxide. Venkat Akkineni, Alufluoride’s Managing Director, briefed us on a teleconference call that these linkages would be formalised by the middle of the next fiscal year, ensuring availability and reasonable pricing of aluminium hydroxide.

Sourcing of other raw materials is intact For the other key raw material, hydrofluosilicic acid, the company is well placed. Last year the company had signed a 20 year agreement for the supply of raw materials from Coromandel (4000 tonne) and IFFCO (7000 tonne).

Since Coromandel’s new capacity for phosphoric acid production would also be available by mid FY20, there doesn’t seem to be any concerns on the supply of hydrofluosilicic acid for the new plant.

Other takeaways from the Q3 result The company’s sales run rate was broadly on track and the sequential decline was mainly due to a maintenance shutdown. There was also a sharp sequential rise in fuel cost and other expenses, impacted by non-recurring charges and we expect expenses to moderate with the slump in crude oil prices.

Result snapshot

Outlook: Margin expansion to help re-rating We remain positive about FY19 sales guidance of 8,600 tonne. In FY20 too, sales volume could remain in a similar range due to expected plant shutdowns for the commissioning (1-2 months) of a new plant. While keeping a conservative capacity utilisation of 35 percent in FY21, we expect the compound annual growth rate (CAGR) in sales to be 14 percent for the next two years.

We are also positive on company’s foray in to middle-east aluminium fluoride market. Company has recently signed a MoU with the Jordan company – Jordan Phosphate Mining Company (JPMC) - for the manufacturing of aluminium fluoride.

As the company is likely to benefit from the new contract cycle in FY20, that should also offset raw material pricing pressures. We expect decisive improvement in operating margin from the second half of FY20 onwards. The management expects about five percent of operational cost savings with the commissioning of the new plant along with a new solar power plant. We expect a 290 bps EBITDA margin expansion by FY21 compared to normalised margins seen in the second quarter of FY19.

Importantly, the capacity expansion, which is going to result in a lot of efficiency gains, is being done without adding leverage to the company’s balance sheet, thereby largely insulating the financials from any cyclical downturn in the industry. Further, the current valuation keep us positive as the stock is trading at 3.7 times estimated earnings for FY21 (EV/EBITDA of 3.2 times for FY21), which is at a discount to the non-ferrous sector.

Follow @anubhavsaysDisclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed hereDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.