Nitin Agrawal Moneycontrol Research

Highlights: - FIEM Industries posted a strong topline growth in Q3FY19 - Raw material prices have softened sequentially but remain a key challenge - Wider adoption of LEDs is the key growth driver for the company - Stock trades at a reasonable valuation --------------------------------------------------

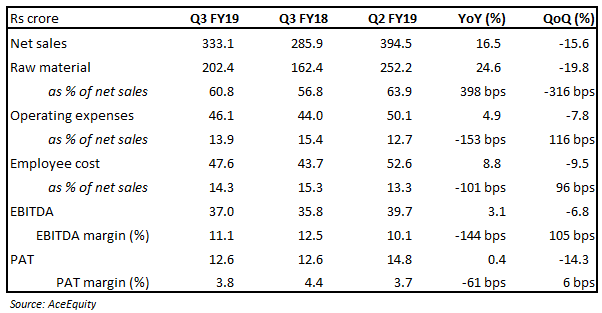

FIEM Industries (FIEM) continued to do well despite the weakness in the two-wheeler market. The company posted strong topline growth year-on-year (YoY) although operating profitability was marred by a rise in raw material (RM) prices.

Its dominant position, marquee clients, focus on developing technologically-advanced products and adoption of LED-based products provide improved earnings visibility and attractive valuations, keeping us confident about the company.

Quarter in a snapshot Despite weak demand, FIEM posted 16.5 percent YoY growth in two-wheeler sales driven by increasing business from existing clients and adoption of LEDs. Interestingly, LED luminaries business clocked revenue of Rs 10 crore and grew 3.78 times compared to the same quarter last year.

RM prices, however, continued to mount weighing down the operating profitability. The earnings before interest, tax, depreciation and amortisation (EBITDA) margin contracted 144 basis points (bps) YoY. This got partially offset by the operating leverage and cost reduction efforts undertaken by the company. Notably, RM prices have come off significantly on a sequential basis leading to EBITDA margin expansion of 105 bps.

Industry outlook – sluggish in near-term FIEM is a lighting solutions provider to automobiles catering to two-wheeler (2W) segment (95 percent revenue contribution) and hence, its fortune is linked to the growth in the 2W segment. The segment is, however, going through a rough patch, thanks to multiple challenges such as an increase in the total cost of ownership due to mandatory long-term insurance and implementation of safety regulations and higher cost of retail finance. This has made the inventory levels to reach alarming levels. It is as high as 80-90 days versus normal inventory of 20 days.

The slowdown is cyclical and the long-term demand scenario in India will no doubt remain intact on the back of relatively strong growth and government’s focus towards rural areas.

LED – a game changer What could help in strengthening the company’s financial performance is the wider adoption of LEDs as LEDs require technical expertise and the company’s in-house R&D supports it.

LED products are expensive compared to conventional products and earn a better margin for the company. The wider adoption of LEDs unlocks huge potential for the company both in terms of sales growth and margin expansion. The management said, despite higher prices, OEMs are willing to shift to these products as they are more efficient and improve the styling and appearance of vehicles.

The government’s decision to make ‘Automatic Headlamp On (AHO)’ in two-wheelers from 2017 has led to increasing adoption of LED-based DRLs (Day Running Lights) which are more energy efficient. Consequently, they have been adopted by a few models. Increasing adoption of LED DRLs in other models would unlock huge potential for the company.

BSVI and EV adoption – upcoming opportunities Bharat Stage (BS) VI norms are to be implemented by 2020 and would require the vehicles to be more energy efficient, which is expected to lead to faster adoption of LEDs. The management expects huge growth from this in the coming year.

Additionally, the company’s products are unaffected by the upcoming electric vehicle (EV) disruption. In fact, EV adoption would lead to increased adoption of LED products as EVs require products to be energy efficient.

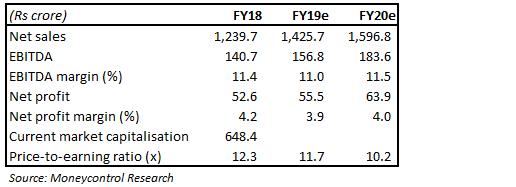

Valuation – at attractive levels The stock has corrected over 50 percent since the start of last year likely due to overall weakness in midcaps and the near term demand concerns cited above. However, long term drivers remain intact, in our opinion; therefore, current levels provide an interesting entry opportunity. FIEM is currently trading at valuations of 15.9 times FY20 projected earnings. We advise investors to consider these businesses with an eye on the long term.

For more research articles, visit our Moneycontrol Research page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.