Rate sensitive stocks tend to rejoice on easing of monetary policy, and with the US Fed announcing a jumbo rate cut of 50 basis points, it is a no brainer that banking stocks may also attract huge investor interest. However, this time, it is different.

While hopes for RBI to follow steps of the Fed have increased, market experts expect the underperformance of banking stocks to continue in the near-term on account of a combination of factors including trailing margins, sluggish deposit growth, and widening credit-to-deposit (CDR) ratio.

Chokkalingam G, founder of Equinomics Research, cautioned that even if the RBI cuts interest rates, banking stocks are unlikely to see relief in the near term. He highlighted factors such as increased liquidity requirements, higher provisions for credit losses, slow deposit growth, and the widening CDR ratio as ongoing challenges that will keep banking stocks under pressure.

So far this year, the Bank Nifty index has risen 9 percent, significantly underperforming benchmark Nifty 50's 16 percent gains.

Dnyananda Vaidya, research analyst tracking BFSI sector at Axis Securities concurred to this view, saying that a rate cut by RBI would dent lenders margins in the near-term with higher share of repo-linked loans.

Repo-linked loans adjust with changes in the repo rate, potentially narrowing the gap between deposit and loan rates, thereby, squeezing bank margins.

However, the Street is split on whether a rate cut by the RBI will happen this year. While some experts anticipate a small rate cut in the October meeting, most are betting on a delayed cut, likely in December or even next year.

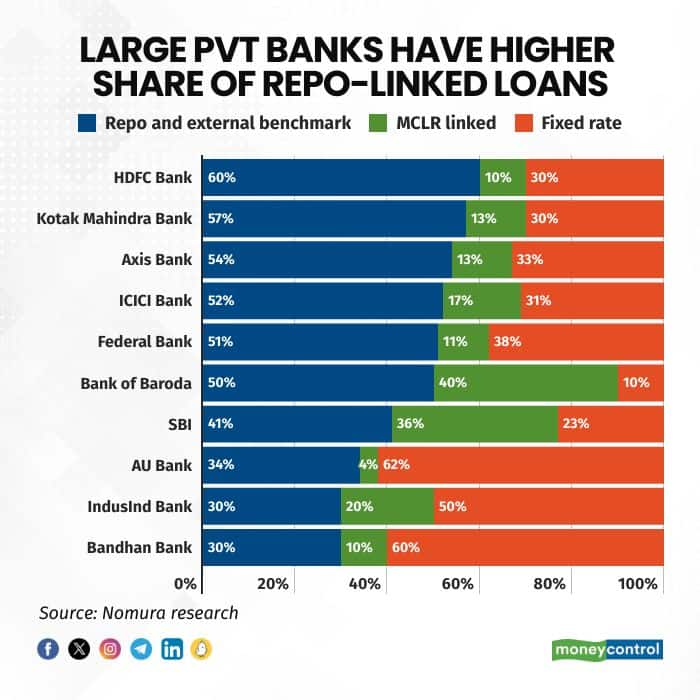

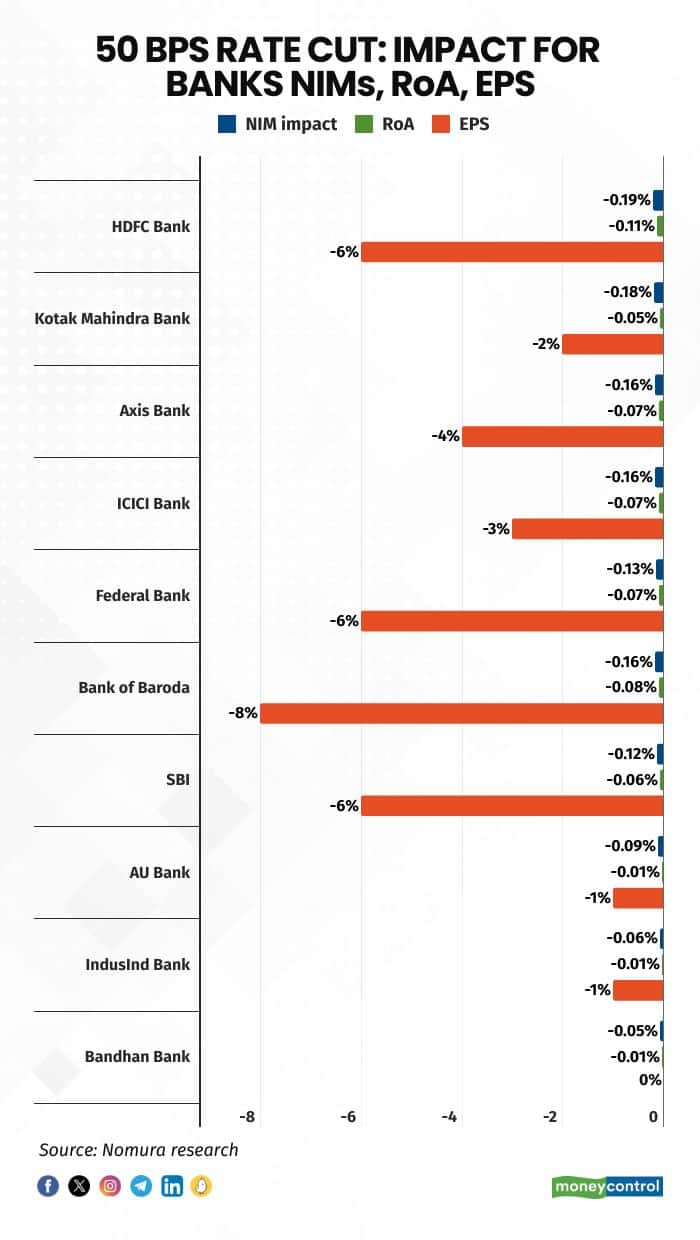

Which lender will feel the most margin pressure?If the RBI mirrors the Fed's 50 bps rate cut, large private banks like HDFC Bank, Kotak Mahindra Bank, Axis Bank, and ICICI Bank are expected to see a margin impact of 15-20 bps, according to Nomura analysts. This is because 50-60 percent of their loan books are directly linked to the repo rate or external benchmarks.

Smaller private banks such as IndusInd Bank, AU Bank, and Bandhan Bank, which have a higher share of fixed-rate loans, will be less affected. Similarly, PSU banks like SBI, which has more MCLR-linked loans, will also experience less impact.

Before FY20, banks didn't use repo rates or external benchmarks for floating rate loans; instead, they based lending rates on their internal benchmarks like the MCLR. In October 2019, the RBI mandated that new floating rate loans for retail and MSME sectors be linked to the repo rate or another external benchmark, making lending rates more sensitive to changes in external interest rates.

Despite the margin pressures, the overall impact on banks' return on assets (RoA) is expected to be limited, thanks to potential mark-to-market (MTM) gains from their treasury books, said Nomura.

Treasury gains occur when bond prices rise after a rate cut, benefiting banks with large government bond portfolios. Large private lenders like HDFC Bank, Kotak Mahindra Bank, Axis Bank, and ICICI Bank are likely to see a 5-10 bps RoA impact, while IndusInd Bank, Bandhan Bank, and AU Bank will experience minimal RoA pressure.

Will deposit, CASA ratio improve with a rate cut?Historically, the CASA ratio of the banking system has improved during rate cut cycles. For example, between FY15 and FY17, the CASA ratio rose by around 600 bps, and it improved by 260 bps between FY19 and FY21. However, the RBI's aggressive monetary tightening over the past two years caused the CASA ratio to drop by about 450 bps by March 2024.

A future rate cut could help the CASA ratio recover from these low levels, as each 1 percentage point increase in the CASA ratio typically boosts banks' net interest margin (NIM) by 4-5 bps, according to Nomura analysts.

Deposit growth could also improve if the RBI shifts to a more accommodative policy. Nomura projects system deposit growth to rise to 13 percent year-on-year for FY25, up from around 11% as of August 9, 2024.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.