The long-awaited initial public offering of SBI Cards and Payment Services, a subsidiary of the country's largest lender State Bank of India, is set to open for subscription.

It will open on March 2 for four days, and will close on March 5.

This will be the largest IPO after General Insurance Corporation of India which came out with the initial offering in October 2017.

The anchor book, a part of qualified institutional buyer (QIB) portion, will open for a day on Friday, February 28.

Kotak Mahindra Capital Company, Axis Capital, DSP Merrill Lynch, HSBC Securities and Capital Markets (India), Nomura Financial Advisory and Securities (India) and SBI Capital Markets will be book running lead managers to the issue.

Here are 10 key things to know before subscribing the issue:About the Public IssueIt comprises a fresh issue of Rs 500 crore and an offer for sale of up to 13,05,26,798 equity shares.

As a part of the offer for sale, parent company SBI will sell up to 3,72,93,371 shares and CA Rover Holdings, an affiliate of the Carlyle Group, will sell up to 9,32,33,427 shares.

The offer includes a reservation of up to 18,64,669 equity shares for subscription by eligible employees and reservation of up to 1,30,52,680 equity shares for SBI shareholders.

Eligible employees will get shares at a discount of Rs 75 per share on final issue price.

The price band for the issue has been fixed at Rs 750-755 per share. Bids can be made for a minimum of 19 equity shares and in multiples of 19 equity shares thereafter.

IPO SizeSBI Cards proposed to raise Rs 10,289 crore at the lower end of the price band (Rs 750 per share) and Rs 10,355 crore at the upper end (Rs 755 per share).

Objective of the IssueThe net proceeds of the fresh issue are proposed to be utilised for augmenting the capital base of the company to meet future capital requirements.

The objective of the offer for sale is to allow the selling shareholders (State Bank of India and CA Rover) to sell equity shares held by them. Hence, SBI Cards will not receive any proceeds from the offer for sale.

Company Profile and SBI PartnershipSBI Cards, which started operations in 1998, offers an extensive credit card portfolio to individual cardholders and corporate clients which includes lifestyle, rewards, travel and fuel, shopping, banking partnership cards and corporate cards covering all major cardholder segments in terms of income profiles and lifestyles.

The partnership with State Bank of India provides SBI Cards access to largest lender's extensive network of 21,961 branches across India, which enables the company to market its credit cards to bank's vast customer base of 44.55 crore (as of December 31, 2019).

In October 2017, SBI Cards launched Project Shikhar as a joint effort between the company and SBI to market its credit card products directly to SBI's customers. Since its implementation, Project Shikhar has significantly increased the proportion of new accounts sourced from SBI's existing customer base, from 35.2 percent of all new accounts in fiscal 2017, to 55.2 percent in fiscal 2019. The company also integrated digital customer acquisition platform with the SBI YONO interface.

Business ModelIts operating model is focused on catering to what it sees as cardholders' two main financial needs: transactional needs and short term credit. The revenue from credit card products consists primarily of interest on credit card receivables and non-interest income primarily comprising of fee-based income such as interchange fees, late fees, annual credit card membership fees and other fees.

Its revenue model generates both non-interest income, as well as interest income, on credit card receivables. The interest that it earns on revolving credit card balances and monthly instalment balances comprised 51 percent of total revenue from operations, and non-interest income comprised 49 percent of revenue from operations, in the nine months ended December 2019.

Growth in BusinessDuring FY17 to FY19, its total credit card spends grew at a rate of 54.2 percent and the number of credit cards outstanding at a 34.5 percent CAGR as compared to a 35.6 percent and 25.6 percent CAGR for the overall credit card industry respectively, according to the RBI.

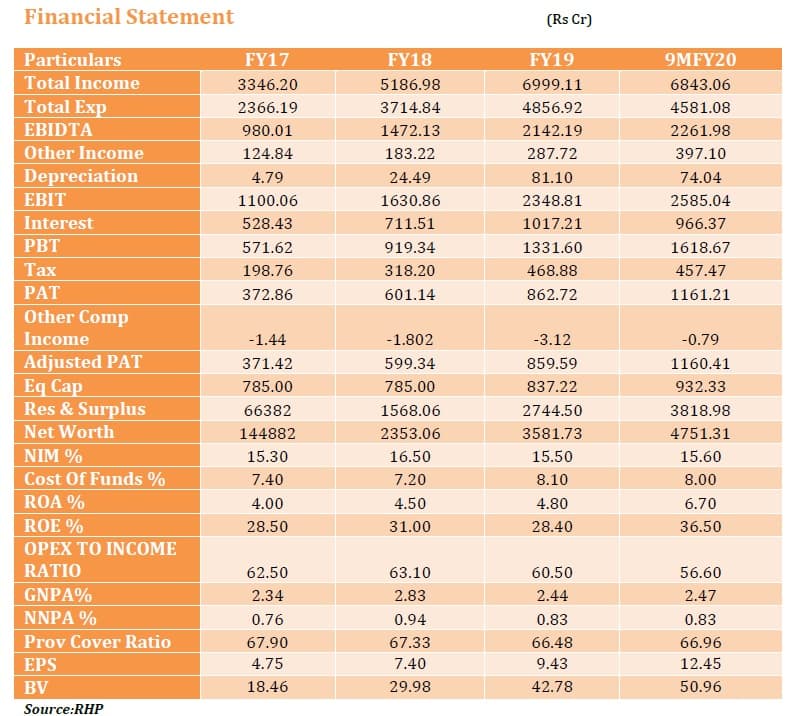

Its revenues from operations increased from Rs 3,346.2 crore in FY17 to Rs 6,999.11 crore in fiscal 2019 at 44.6 percent CAGR. Net profit increased from Rs 372.86 crore in FY17 to Rs 862.72 crore in FY19 at a CAGR of 52.1 percent.

Its return on average equity (ROAE) stood at 28.5 percent in FY17 and 28.4 percent in FY19, while return on average assets (ROAA) increased from 4 percent in FY17 to 4.8 percent in FY19.

There are 74 players offering credit cards in India, with the top three private banks (HDFC Bank, Axis Bank and ICICI Bank) and SBI Card, dominating the segment with a combined total of 72 percent market share by number of outstanding credit cards as of March 2019 and approximately 66 percent market share by credit card spends in FY19.

HDFC Bank is the market leader and has maintained its market share in the number of outstanding credit cards at 27 percent over the years, followed by SBI Card (18 percent), (ICICI Bank (14 percent) and Axis Bank (13 percent).

HDFC Bank is the market leader in total credit card spends, but has lost market share in total credit card spends from 30 percent in FY14 to 28 percent in fiscal 2019. SBI Card and Axis Bank, on the other hand, have gained market share in total credit card spends over the years from 11 percent and 6 percent in FY14 to 18 percent and 11 percent in FY19, respectively.

Credit card spends have registered robust growth, growing at a CAGR of 32 percent from FY15 to FY19 to reach Rs 6 lakh crore in FY19. It is expected to grow at a healthy rate to reach Rs 15 lakh crore in FY24, according to CRISIL Research.

The number of credit cards issued stood at 4.7 crore in FY19, growing at a CAGR of 20 percent over the last five years, and is expected to grow by 25 percent from FY19 to FY20, according to CRISIL Research.

In absolute terms, per-capita Private Final Consumption Expenditure (PFCE) was approximately Rs 85,000 in FY19, of which only Rs 4,500 comprises spending through credit cards. Credit card spending accounted for approximately 5.4 percent of PFCE in FY19, compared to approximately 2.3 percent in FY14.

Going forward, CRISIL Research expects credit cards spend to grow at a much faster pace than PFCE, and per capital credit card spend as a percentage of per capita PFCE is expected to reach 7.6 percent by FY24.

Competitive Strengths> It is the second-largest credit card issuer in India with deep industry expertise and has demonstrated track record of growth and profitability.

> It has a diversified customer acquisition network that allows it to engage prospective customers across multiple platforms, which it believes is a key strength and competitive advantage.

> It is supported by a strong brand and pre-eminent promoter.

> It has a comprehensive and diverse portfolio of credit card products.

> Its advanced risk management infrastructure is robust and data-intensive, both in terms of frequency and volume of review, and is guided by its data analytics capabilities.

> It has a scalable, modern and sophisticated technology infrastructure capable of servicing the entire credit card life cycle.

> It has a professional and experienced management team with a deep level of expertise in the credit card industry and the overall financial services industry. Managing Director and Chief Executive Officer, Hardayal Prasad, has over 36 years of experience in the financial services industry.

Strategies> It intends to grow cardholder base by continuing to expand customer acquisition capabilities.

> It intends to tap into new cardholder segments by continuing to expand the portfolio of credit card products.

> The company seeks to increase the number of credit card transactions conducted by its cardholders in order to increase revenues.

> It intends to continue to optimize risk management processes.

> It is focused on continuing to invest in digital and mobile capabilities to enhance cardholder experience.

> The company operates in a highly competitive, ever-evolving industry where it must continuously improve technology platform in order to compete effectively and reduce operating costs.

Shareholding and ManagementCurrently, State Bank of India owns 74 percent stake in the company and the rest 26 percent is held by CA Rover Holdings, an affiliate of the Carlyle Group.

Carlyle Group is a global investment firm with deep industry expertise with over $224 billion of assets under management (AUM) as of December 31, 2019.

After the issue, SBI's shareholding will be reduced to 69.51 percent and CA Rover's to 22.40 percent.

Rajnish Kumar is the non-executive chairman, Hardayal Prasad is the Managing Director and Chief Executive Officer, and Dinesh Kumar Khara and Shree Prakash Singh are non-executives. All are nominees of SBI.

Sunil Kaul, the nominee of CA Rover, is the non-executive director, while Tejendra Mohan Bhasin, Nilesh Shivji Vikamsey, Rajendra Kumar Saraf, Dinesh Kumar Mehrotra and Anuradha Shripad Nadkarni are Independent Directors.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.